Post-October 2025 Market Dynamics: Navigating Macroeconomic Recalibration and Investor Sentiment Shifts

The post-October 2025 global market landscape is defined by a fragile equilibrium between macroeconomic recalibration and shifting investor sentiment. Central banks, investors, and policymakers are navigating a complex interplay of divergent monetary policies, trade tensions, and technological optimism. This analysis dissects the key drivers shaping near-term dynamics and their implications for asset allocation and risk management.

Macroeconomic Recalibration: Divergence and Constraints

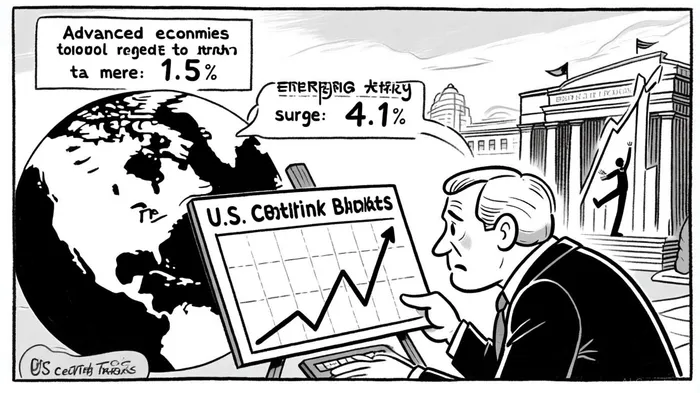

Global growth remains subdued, with the IMF projecting 3.2% expansion for 2025, down from 3.3% in 2024, as advanced economies grapple with structural headwinds[1]. The U.S. Federal Reserve's cautious approach to rate cuts-initiating a 25-basis-point reduction in October 2025-reflects persistent inflationary pressures in services sectors and the drag from Trump-era tariffs[2]. In contrast, the European Central Bank (ECB) has accelerated easing, cutting rates to 2.15% by mid-2025, while China's central bank has injected liquidity to stabilize domestic growth amid property market fragility[3].

This policy divergence has amplified currency volatility and trade imbalances. The U.S. dollar's strength, fueled by higher-for-longer rates, has constrained emerging markets, where growth remains resilient at 4.1% but faces headwinds from protectionist policies[4]. Meanwhile, global inflation, though declining to 5.43% in 2025, remains above central bank targets in key economies, with the U.S. CPI at 3.5% and China's deflationary pressures underscoring regional disparities[5].

Investor Sentiment: Optimism Amid Paranoia

Investor sentiment in October 2025 reveals a duality of optimism and caution. A global survey by Ontario Teachers' Pension Plan (OTPP) found 70% of investors view the 2025 environment as favorable, driven by AI-driven equity gains and emerging markets' resilience[6]. However, 44% cited geopolitical tensions-particularly U.S.-China trade frictions-as a top risk, while 49% expressed concerns over macroeconomic volatility[7].

Behavioral biases are amplifying market volatility. Panic selling during tariff-related selloffs in early 2025, as noted by a Canadian investor who liquidated 80% of their portfolio, highlights the psychological toll of uncertainty[8]. Conversely, AI-related FOMO (fear of missing out) has inflated valuations for tech infrastructure, with leading AI firms already priced for perfection[9]. This tension between speculative fervor and risk aversion underscores the fragility of current market psychology.

Asset Allocation: Defensive Tilts and Alternative Appetite

Portfolio strategies have shifted toward defensive positioning and diversification. Gold, for instance, surged to $3,800 per ounce in October 2025, as central banks in emerging markets increasingly view it as a hedge against U.S. debt risks and policy instability[10]. Fixed income has also gained traction, with the Bloomberg U.S. Aggregate Bond Index rising 2.9% year-to-date, supported by a 4.17% Treasury yield reflecting evolving Fed expectations[11].

Equity markets, meanwhile, have seen a rotation from megacap dominance to mid- and small-cap stocks, which offer more attractive valuations amid a weaker dollar[12]. International equities have benefited from this shift, with the S&P 500's forward P/E ratio resetting to 20.2x from 26.7x in early 2025[13]. Private markets and real assets, including infrastructure and real estate, are also gaining favor, with J.P. Morgan projecting 8.1% returns for U.S. core real estate over the next decade[14].

Conclusion: Preparing for a Divergent Future

The post-October 2025 market environment demands a nuanced approach to risk management. While central banks continue to navigate the delicate balance between inflation control and growth support, investors must remain vigilant to geopolitical and policy-driven shocks. Diversification into alternatives, disciplined re-entry strategies during selloffs, and a focus on structural trends like AI infrastructure will be critical. As the OECD warns, "Uncertainty remains the new normal," and adaptability will define success in this recalibrated landscape[15].

Comentarios

Aún no hay comentarios