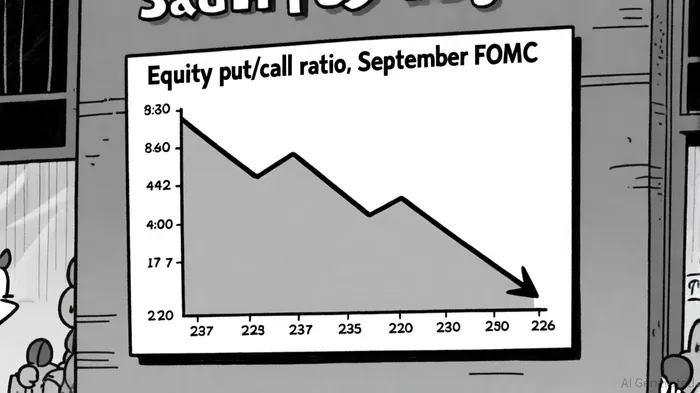

Post-FOMC Options Imbalance and Its Implications for Equity Market Direction

The Federal Open Market Committee (FOMC) meeting in September 2025 has ignited a surge in bullish positioning across U.S. equity options markets, with call buying outpacing put buying at an unprecedented rate. According to a report by the CBOE, single stock option volume hit a record high of 54 million contracts post-FOMC, driven almost entirely by call options[1]. This has pushed the equity put/call ratio to a 3-month low, signaling extreme optimism among investors. Meanwhile, the Russell 2000 index (IWM) saw call volumes reach an all-time high of 2.85 million contracts, dwarfing put volumes by a margin of over five to one[1]. Such imbalances are not merely statistical anomalies—they are windows into investor psychology and potential harbingers of market direction.

The Mechanics of Post-FOMC Call Buying

The recent options activity reflects a broader shift in risk appetite. For instance, stock "X" experienced a 202.53% spike in open interest, with a call-to-put ratio of 4.47, while ERJ and ADSK also saw gains of 35.01% and 25.34%, respectively[1]. These figures underscore a preference for leveraged exposure to equities, particularly in sectors perceived as beneficiaries of lower interest rates. The surge in call buying is further amplified by inverted call skew, where out-of-the-money (OTM) calls trade at a premium to at-the-money (ATM) calls—a phenomenon that jumped from 3% to 12% of stocks in the past week[1]. This suggests investors are not only betting on upward moves but also hedging against tail risks with expensive, far-out OTM calls, a strategy often seen ahead of anticipated volatility.

Historically, such imbalances have had mixed implications. A low put/call ratio—where call buying dominates—is often interpreted as a contrarian signal. As noted by Investopedia, ratios below 0.5 (indicating more than twice as many calls traded relative to puts) have historically preceded market tops[2]. While the current ratio is not yet at extreme levels, its rapid decline raises questions about overcrowded positions. Studies also highlight that abnormal order imbalances in VIX futures and call options tend to predict short-lived informational advantages during FOMC embargoes, suggesting potential information leakage or rapid digestion of policy signals[3].

Historical Correlations and Market Outcomes

The interplay between FOMC decisions and equity performance is well-documented. Research from 1994 to 2016 reveals that equity premiums are disproportionately earned during "even weeks" following FOMC meetings, with average excess returns of 0.33% to 0.60% compared to negative returns during "odd weeks"[4]. More recently, the S&P 500 has historically delivered 13% of its cumulative returns during FOMC meeting days between 1960 and 2000, despite these events representing just 4.42% of trading days[5]. A simple strategy of investing in the S&P 500 during FOMC weeks and holding cash otherwise would have generated a Sharpe ratio double that of a year-round strategy[4].

The September 2025 FOMC meeting, which included a 25-basis-point rate cut, aligns with this historical pattern. Post-meeting, the S&P 500 closed at a record high, while the Nasdaq surged 0.94%[6]. Small-cap and value stocks, in particular, outperformed, with the Morningstar US Small Cap Index rising 4.58% in August 2025[3]. This rally was fueled by Fed Chair Jerome Powell's dovish signals at Jackson Hole, which hinted at a "shifting balance of risks" in the labor market and a willingness to ease policy further[7].

Implications and Risks

While the current call buying frenzy suggests a bullish consensus, it also introduces risks. A low put/call ratio often precedes market corrections, as excessive bullishness can lead to overcrowded trades. For example, during the 2008 financial crisis and the 2015 global economic slowdown, the put/call ratio spiked to extreme levels before reversing course[2]. Similarly, the current inverted call skew—where OTM calls are priced higher than ATM calls—indicates a market pricing in a sharp upward move with limited downside protection. If the Fed's dovish pivot fails to materialize or inflationary pressures resurge, this positioning could lead to rapid unwinding.

Moreover, the Fed's rate cut has already been partially priced into asset classes. The 10-year Treasury yield fell to 4.26% post-meeting[7], and gold and cryptocurrencies like EthereumETH-- saw heightened volatility[7]. However, the benefits for consumers—such as lower mortgage and credit card rates—remain muted in the short term[8]. Savers, meanwhile, face declining returns as CD rates adjust downward[8].

Conclusion

The post-FOMC options imbalance in 2025 reflects a market primed for growth but vulnerable to overextension. While historical correlations suggest that the current bullish positioning could support further gains, particularly in small-cap and value stocks, investors must remain cautious. The Fed's dual mandate—balancing employment and inflation—introduces uncertainty, especially with global competitors like China's DeepSeek AI challenging U.S. tech dominance[9]. A diversified approach, hedging against potential volatility with sector rotation and tactical use of options, may be prudent. As always, the market's next move will depend not just on Fed policy but on the broader economic narrative it seeks to manage.

Comentarios

Aún no hay comentarios