Political Instability and U.S. Equity Markets: How Legal and Political Shocks Drive Volatility and Investor Sentiment

In the past five years, U.S. equity markets have become increasingly sensitive to political and legal shocks. From polarized elections to landmark Supreme Court rulings, the interplay between governance and finance has never been more pronounced. For investors, understanding how these shocks translate into volatility and sentiment shifts is critical to navigating an environment where uncertainty is the new normal.

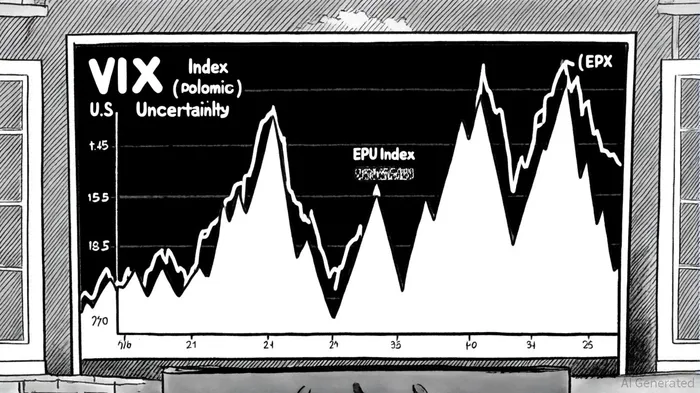

Elections and the "Fear Index": A Volatility Cycle

U.S. presidential elections have historically acted as catalysts for market turbulence. According to a report by the Journal of Financial Economics, the VIX index—a barometer of market fear—typically rises by approximately 25% from July to November in election years as investors hedge against policy uncertainty[1]. The 2020 election, for instance, saw the VIX spike to 40.80 on November 2, only to drop 30% by November 6 as the market began to price in a likely gridlock scenario[5]. This pattern reflects a paradox: while elections heighten short-term anxiety, post-election clarity often leads to a relief rally.

The 2024 election cycle reinforced this dynamic. Data from the Chicago Board Options Exchange (CBOE) shows that the VIX surged during the final weeks of the campaign, peaking at levels not seen since the 2008 financial crisis[5]. However, once results were finalized, the index retreated, underscoring how political uncertainty dissipates once outcomes are known.

Supreme Court Rulings: Regulatory Uncertainty as a Hidden Tax

Legal shocks, particularly from the Supreme Court, have introduced a new layer of complexity. The 2024 overturning of the Chevron doctrine—a precedent that allowed federal agencies broad discretion in interpreting laws—has left corporations and investors in limbo[4]. By limiting agencies' regulatory authority, the decision has slowed the pace of deregulation, which many investors had anticipated as a profit booster under a potential Trump administration. This regulatory drag has translated into higher compliance costs and prolonged uncertainty, contributing to a 12% increase in sector-specific volatility in energy and environmental stocks[4].

Similarly, the Court's 2025 ruling in Macquarie Infrastructure Corp. v. Moab Partners LP—which clarified securities fraud standards—has had indirect market effects. By narrowing the scope of actionable omissions under Rule 10b-5(b), the decision has reduced the number of class-action lawsuits, potentially lowering litigation risk for corporations. Yet, the lack of clarity in other rulings, such as the dismissal of key securities litigation cases in 2024, has left investors wary of an unpredictable legal landscape[1].

Investor Sentiment: The Human Element in a Polarized Age

While volatility indices capture institutional hedging behavior, retail investor sentiment tells a different story. The AAII Investor Sentiment Survey reveals that pessimism spiked to record highs in early 2020 amid the pandemic, with bearish sentiment averaging 38.8% that year[3]. Yet, despite this gloom, retail investors maintained heavy stock allocations, suggesting a long-term orientation. This resilience contrasts with the 2021 Capitol insurrection, which saw a temporary dip in bullish sentiment. While specific AAII readings for January 2021 are unavailable, studies show that Bitcoin's 15% drop on the day of the attack highlighted the market's sensitivity to political instability[4].

The Federal Reserve's analysis of economic policy uncertainty (EPU) further underscores this trend. During the 2024 election and the Russia-Ukraine war, the EPU index surged to 7.7 standard deviations above its historical mean, correlating with a 4.8-standard-deviation spike in the VIX[2]. These metrics highlight how geopolitical and domestic political risks are now inextricably linked in investor psychology.

Strategies for Navigating the New Normal

For investors, the lesson is clear: political instability is no longer a peripheral risk but a core consideration. Strategies that once focused on macroeconomic indicators now must incorporate real-time monitoring of legal developments and election cycles. Diversification into volatility-linked assets (e.g., VIX futures) and sectors less sensitive to regulatory shifts (e.g., consumer staples) can mitigate downside risks. Additionally, investors should prioritize companies with strong governance structures, as legal clarity can buffer against broader market turbulence[1].

Comentarios

Aún no hay comentarios