PLXS Stock Up 32% in 3 Months: Is There Further Upside Left?

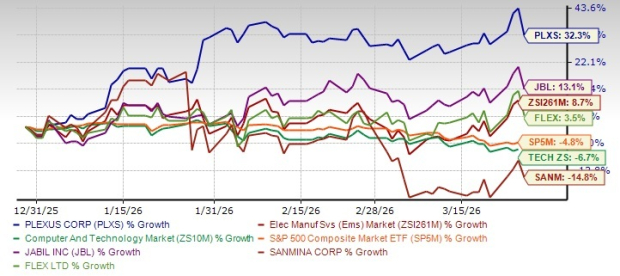

Plexus Corporation PLXS has emerged as a compelling performer in the electronics manufacturing services (EMS) space, with the stock price appreciating 32.3% over the past three months, outperforming the Electronic Manufacturing Industry’s growth of 8.7%. The S&P 500 composite and the broader Computer Technology Sector have declined 4.8% and 6.7%, respectively.

Price Performance

Image Source: Zacks Investment Research

Other players in the electronics manufacturing services space, like Jabil JBL and Flex Ltd. FLEX, have gained 13.1% and 3.5%, respectively, while Sanmina Corporation SANM is down 14.8%.

Given this backdrop, the question for investors is straightforward: after this rally, does PLXSPLXS-- still offer compelling long-term upside?

Let us take a closer look at PLXS fundamentals, growth drivers, competitive advantages and potential risks and assess whether it is still a buy?

Multiple Tailwinds Offer Runway for Long-Term Growth

A healthy number of program ramps are expected to drive the top-line performance for PlexusPLXS--. The company is focusing its efforts on sectors with robust demand, such as healthcare and life sciences, aerospace and defense, and industrial markets, especially semicap and energy management subsectors.

In the first quarter of fiscal 2026, Plexus announced 22 manufacturing program wins, which are estimated to contribute $283 million in annualized revenues once fully ramped into production. For fiscal 2025, Plexus had 141 manufacturing wins totaling $941 million in annualized revenues.

Notably, the Aerospace and Defense sector delivered record $220 million in the fiscal first quarter wins and Healthcare/Life Sciences had $40 million. Management highlighted that program wins, share gains and strengthening market demand position it for meeting/exceeding the high end of 9% to 12% total revenue growth target for fiscal 2026. The funnel of qualified manufacturing opportunities is $3.6 billion, indicating a strong pipeline for growth. The company had a record funnel for its Aerospace and Defense end market segment.

For both Aerospace and Healthcare/Life Sciences segments, PLXS expects to exceed the 9-12% range.

Further, strong cash flow generation bodes well. Plexus is driving free cash flow generation through a combination of operational/capex discipline and inventory reduction. While fiscal first-quarter free cash flow was negative due to investments, Plexus reaffirmed its fiscal 2026 free cash flow target of $100 million, underscoring working capital efficiency. Strong cash flow generation positions Plexus to maximize shareholder value via buybacks and reduce debt. It repaid $100 million of debt in fiscal 2025.

Plexus Corp. Price, Consensus and EPS Surprise

Plexus Corp. price-consensus-eps-surprise-chart | Plexus Corp. Quote

On the last earnings call, management emphasized that all excess cash will be used to create shareholder value. The company repurchased $22.4 million worth of shares at an average price of $146.36 per share under its repurchase program. Out of the $100 million authorization, $62.6 million remains available. For fiscal 2025, it repurchases $65 million worth of shares. The robust cash generation ensures that Plexus has a healthy financial foundation to support growth and investment in the business.

The company’s business strategy, focusing on earning a return on invested capital (“ROIC”) that exceeds its weighted average cost of capital (“WACC”), bodes well. For the first quarter of fiscal 2026, the company’s after-tax ROIC reached 13.2%, 420 bps above the WACC of 8.9%.

However, no investment case is without risks. The challenges in the Industrial sector in the near term remain concerning. Fiscal first-quarter revenues declined 8% sequentially. Growth recovery is heavily dependent on semicap demand rebound and program ramps in the industrial equipment subsector, while other industrial subsectors continue to face softness. If the semicap cycle stalls or weakens again, the Industrial segment could remain a drag on consolidated growth. Management expects fiscal 2026 revenues for this sector to approach the 9% to 12% target range.

Macro uncertainty owing to shifting trade policy and stiff competition in the EMS space from FLEXFLEX--, JabilJBL-- and SanminaSANM-- are additional concerns.

Image Source: Zacks Investment Research

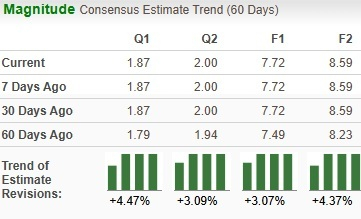

Given all these factors, analysts have revised PLXS’ estimates up for the current quarter and year.

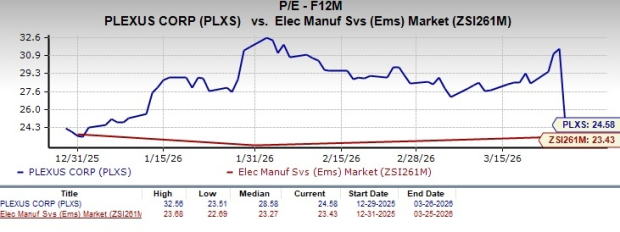

PLXS Valuation

In terms of the forward 12-month price/earnings ratio, PLXS is trading at 24.58, slightly above the sector’s multiple of 23.43.

Image Source: Zacks Investment Research

In comparison, FLEX, Jabil and Sanmina trade at a forward 12-month P/E of 18.2X, 20.57X and 11.84X, respectively.

How to Play PLXS Stock?

Plexus’ robust pipeline of program wins, expanding exposure to end markets like aerospace, defense and healthcare, and a solid $3.6 billion opportunity funnel provide improved visibility into sustained revenue growth. Coupled with healthy cash generation supporting buybacks, PLXS remains well-positioned for further upside despite near-term industry headwinds.

PLXS currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Plexus Corp. (PLXS): Free Stock Analysis Report

Jabil, Inc. (JBL): Free Stock Analysis Report

Flex Ltd. (FLEX): Free Stock Analysis Report

Sanmina Corporation (SANM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios