The Four Pillars of Equity Market Risk in 2025: Valuation, Earnings, Policy, and Liquidity

The equity bull market of 2025 is perched on a knife's edge, buoyed by robust earnings growth but shadowed by a quartet of risks: valuation overhang, earnings momentum deceleration, policy uncertainty, and liquidity tightening. These factors, while not mutually exclusive, collectively amplify the fragility of current market optimism.

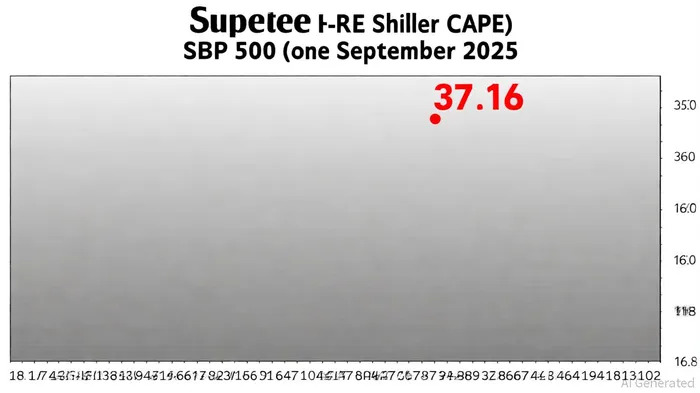

Valuation Overhang: A House of Cards?

The S&P 500's Shiller P/E ratio (CAPE) of 37.16 as of September 2025, according to a Shiller P/E guide, is a stark reminder of the market's detachment from historical norms. For context, the long-term average CAPE ratio hovers around 16.8, with readings above 25 typically signaling overvaluation, per global CAPE data. The global stock market's CAPE ratio of 25.84, noted in an Advisor Perspectives analysis, further underscores the synchronized optimism across geographies, particularly in the U.S., where Technology and Financials dominate. While earnings growth has historically justified elevated valuations, the current disconnect raises concerns about mean reversion. As noted by financial commentator David Shiller in a Markets article, "When valuations stretch beyond the bounds of earnings, the market becomes a waiting room for corrections."

Earnings Momentum: Broadening but Fraying

The S&P 500's 15% projected earnings growth for 2025, according to FactSet's Earnings Insight,-well above the 10-year average of 8%-has been a lifeline for equity bulls. This growth is broadening, with non-Magnificent 7 companies in the index expected to contribute 13% growth compared to 4% in 2024, as S&P Global observed. However, the narrative is fraying at the edges. Earnings estimates for 2025 have fallen from 14.8% to 11.5% year-over-year due to geopolitical tensions and trade policy risks, according to a Nasdaq review. Meanwhile, sector divergence is emerging: Communication Services and Financials lead the charge, while Energy lags, as shown in a Q2 earnings report. LPL Research commentary warns that achieving double-digit growth in 2025 will require "a perfect storm of AI adoption and tariff moderation," a scenario that feels increasingly fragile.

Policy Uncertainty: The Invisible Tax on Growth

Policy uncertainty, both economic and trade-related, has become a silent killer of market stability. The U.S. Economic Policy Uncertainty (EPU) index has surged since 2019, with the Federal Reserve noting that a one‑standard‑deviation increase in EPU correlates with a 0.5–1% drop in industrial production, as detailed in a Federal Reserve note. Trade Policy Uncertainty (TPU) is even more volatile, with investment declines peaking at 1% within three months of shocks, according to the ECB review. The European Central Bank has flagged U.S. tariff hikes as a potential catalyst for a trade war, which could ripple through global supply chains and inflation expectations; J.P. Morgan's mid‑year outlook cautions that "policy uncertainty is the new baseline for equity risk premiums," a point also reported by Reuters, forcing investors to price in a margin of error for regulatory and geopolitical shocks.

Liquidity Tightening: The Fed's Double-Edged Sword

The Federal Reserve's quantitative tightening (QT) program has drained liquidity from financial markets, with U.S. bank reserves falling below $3 trillion-the lowest in over two years-according to an MFS analysis. This liquidity squeeze has amplified equity volatility, particularly for long-duration assets like growth and technology stocks, as highlighted in a Visual Capitalist piece. Historically, QT periods (e.g., 2017–2019) have been marked by sharp price swings as market depth erodes, a dynamic noted in the St. Joseph Partners outlook. The current environment is no different: bond yields have risen sharply, creating a widening gap with equity valuations that historically precedes corrections, according to a Cambridge Associates insight. While the Fed's Standing Repo Facility aims to mitigate liquidity stress, the cumulative impact of QT remains a headwind for risk assets, as a Morningstar discussion explains.

Conclusion: A Delicate Balancing Act

The 2025 equity market is a paradox: overvalued yet earnings-driven, optimistic yet policy-risk-laden. For bulls, the hope rests on AI-driven productivity gains and a soft landing narrative. For bears, the risks of a valuation-driven selloff loom large, exacerbated by liquidity fragility and policy shocks. Investors must navigate this duality with caution, hedging against scenarios where earnings growth falters or liquidity conditions tighten further. As the year progresses, the interplay of these four pillars will determine whether the bull market endures-or implodes.

Comentarios

Aún no hay comentarios