Philippine Real Estate Debt Investment: Navigating Credit Quality and Market Stability in 2025

The Philippine real estate debt market in 2025 presents a nuanced investment landscape, characterized by a blend of resilience and caution. While macroeconomic tailwinds and structural reforms bolster long-term optimism, sector-specific credit risks and operational challenges demand careful scrutiny. This analysis evaluates the interplay between credit quality and market stability, drawing on recent data to outline strategic considerations for investors.

Credit Quality: A Mixed Bag of Risks and Resilience

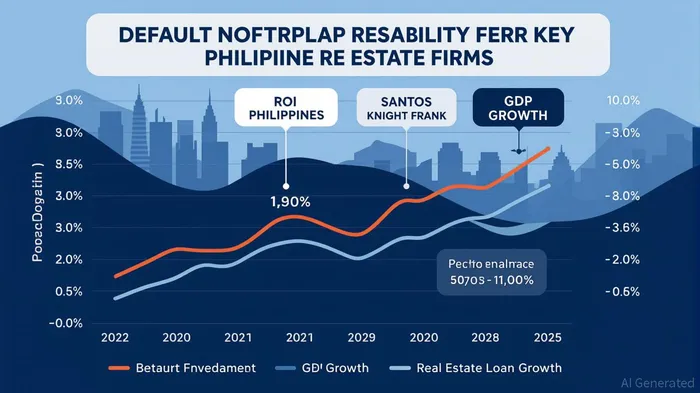

The creditworthiness of Philippine real estate debtors has shown divergent trends. Megaworld Philippine Properties, a bellwether developer, exemplifies the sector's fragility. Its Martini Letter Rating fell from B1 to B2 between May 2022 and June 2025, reflecting financial strain from large-scale redevelopment projects like the P2.5 billion Eastwood City renovation[2]. Concurrently, its default probability surged to 1.993 in April 2025 before stabilizing at 1.619 by June 2025[2]. Such volatility underscores the vulnerability of firms reliant on capital-intensive projects amid rising interest rates and inflationary pressures.

However, broader credit metrics remain reassuring. Japan-based R&I affirmed the Philippines' investment-grade rating at “A-” with a stable outlook in August 2025[3], citing manageable non-performing loan (NPL) ratios and robust economic growth. Real estate loans grew by 7.3% year-on-year to P3.39 trillion in Q2 2025, with NPLs easing to 3.78%[1]. This suggests that while individual firms face stress, systemic risks remain contained.

Market Stability: Structural Strength Amid Sectoral Shifts

The Philippine economy's 5.5% Q2 2025 growth[4] has underpinned demand for commercial real estate, particularly in prime office markets like Makati and Bonifacio Global City (BGC). Office rents in these areas rose by 0.5%, with vacancy rates at 10.5%, outperforming fringe markets grappling with oversupply[4]. This bifurcation highlights the importance of location and asset quality in mitigating risks.

Hybrid work models and sustainability mandates are further reshaping demand dynamics. Developers prioritizing green-certified properties are attracting tenants seeking cost efficiency and regulatory compliance[4]. Meanwhile, regional hubs like Cebu and Davao are emerging as growth corridors, driven by decentralization and infrastructure investments[4]. These trends suggest that adaptability—both in asset management and geographic diversification—will be critical for long-term stability.

Investment Considerations: Balancing Risk and Reward

For investors, the key lies in differentiating between high-quality and speculative opportunities. Realty Options Inc. (ROI) Philippines, with a 0.378% default probability and B3 rating[1], represents a moderate-risk proposition. Its 4.5% credit spread (91st percentile in the bond universe) reflects elevated perceived risk but also potential for outperformance if economic conditions stabilize[1]. Conversely, Santos Knight Frank's recovery from a peak default probability of 0.678 in 2022 to 0.227 by November 2024[2] illustrates the sector's capacity to rebound amid improved macroeconomic conditions.

Banks' real estate exposure, now at 19.61% of total loans[1], remains a double-edged sword. While this level is within manageable thresholds, a sharp rise in past-due loans (up 10.3% to P155.82 billion in Q2 2025[1]) signals the need for rigorous due diligence. Investors should prioritize firms with strong liquidity buffers and transparent governance, particularly those leveraging government-backed infrastructure programs.

Conclusion: A Prudent Path Forward

The Philippine real estate debt market in 2025 is a study in contrasts: macroeconomic strength coexists with sectoral fragility, and innovation offsets traditional risks. For investors, the path forward requires a balanced approach—capitalizing on growth in prime commercial assets and sustainable developments while hedging against overexposure to high-leverage developers. With the country's credit rating affirmed and economic fundamentals intact, the sector offers compelling long-term potential, provided risks are meticulously managed.

Comentarios

Aún no hay comentarios