PG&E's $500M Term Loan: Strategic Funding or Warning Signal?

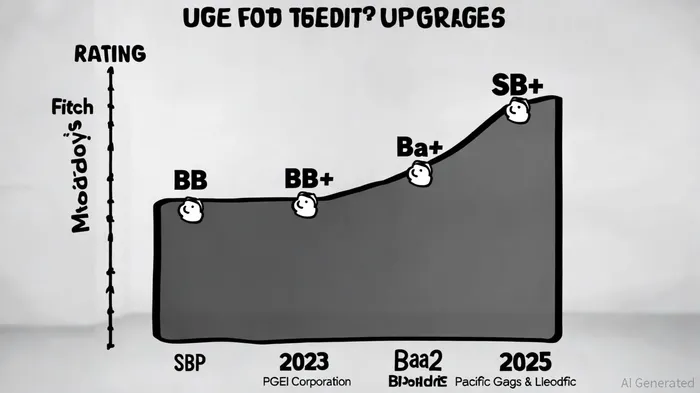

Pacific Gas & Electric (PG&E) has long navigated the dual challenges of regulatory scrutiny and wildfire liabilities. Yet, recent developments suggest a shift in its financial trajectory. As of June 30, 2025, PG&E Corporation's credit ratings reflect optimism: S&P and Fitch upgraded its issuer rating to BB with a positive outlook, while Moody's elevated its senior secured debt to Ba2 from Ba3 [1]. For Pacific Gas & Electric, Moody's upgraded its senior secured first mortgage bonds to Baa1 from Baa2 [2]. These upgrades underscore progress in mitigating wildfire risks—$20 billion invested since 2020—and legislative support via California's AB1054, which caps liabilities and provides access to a state wildfire insurance fund [3].

However, the utility's $500 million term loan maturing in 2025 raises critical questions about its capital allocation strategy. Is this a calculated move to fund infrastructure modernization, or does it signal lingering financial stress?

Strategic Funding: Aligning with Long-Term Goals

PG&E's capital strategy appears anchored in balancing debt management with infrastructure investment. The $500 million loan, part of a broader $5.5 billion Debtor-in-Possession (DIP) financing package from 2019, was initially designed to fund operations during bankruptcy proceedings [4]. While specific terms for the 2025 maturity remain opaque, the company has demonstrated a pattern of refinancing high-cost debt. For instance, in November 2023, PG&E issued $1.5 billion in convertible senior secured notes to repay portions of its $2.75 billion secured term loan, which carried a floating interest rate of ~8.44% [5]. This suggests a deliberate effort to reduce refinancing risks and stabilize liquidity.

The utility's 2027–2030 General Rate Case (GRC) further aligns with strategic priorities. By proposing modest rate increases, PG&E aims to fund grid modernization, wildfire mitigation, and clean energy projects while maintaining customer affordability [6]. A $15 billion federal loan guarantee from the U.S. Department of Energy (DOE) under the Energy Infrastructure Reinvestment (EIR) program—offering lower interest rates than traditional markets—bolsters this strategy [7]. Analysts note that such low-cost financing could save customers up to $1 billion over the loan's lifespan [8].

Credit Risk and Liquidity Concerns

Despite these positives, PG&E's liquidity metrics reveal vulnerabilities. As of June 2025, its current ratio stood at 0.94, down from 1.05 in December 2024 [9]. This tightening liquidity position, coupled with a debt-to-equity ratio of 1.81 as of 2023 [10], raises concerns about its ability to service debt amid rising interest rates. The $500 million term loan, if refinanced at higher rates, could exacerbate this strain.

Moreover, the DOE's $15 billion loan guarantee remains conditional, subject to technical and regulatory approvals [11]. PG&E has acknowledged “substantial uncertainty” about the loan's implementation under potential policy shifts, prompting requests for higher return rates to offset risks [12]. This uncertainty introduces volatility into its capital structure, complicating long-term planning.

Capital Allocation: Prioritizing Resilience Over Short-Term Gains

PG&E's capital allocation strategy emphasizes resilience. Its five-year capital plan, expanded to $63 billion from 2024 to 2028, prioritizes wildfire mitigation, battery storage, and grid upgrades [13]. The $500 million term loan, while part of a larger refinancing effort, appears to support these priorities. For example, the utility has already secured junior subordinated notes to fund its capital plan and reaffirmed $3 billion in equity issuance guidance for 2025–2028 [14].

However, the absence of explicit terms for the 2025 loan—such as interest rates, covenants, and repayment schedules—introduces ambiguity. Without transparency, investors struggle to assess whether the loan aligns with PG&E's credit risk profile. For context, similar term loans in the energy sector often carry SOFR-based rates with potential reductions tied to operational milestones [15]. If PG&E's terms are less favorable, the loan could strain its balance sheet.

Conclusion: A Calculated Bet with Caveats

PG&E's $500 million term loan represents a strategic bet on long-term resilience, supported by regulatory tailwinds and access to low-cost federal financing. The recent credit rating upgrades and expanded credit facilities—such as a $5.4 billion revolving credit line extended to 2030 [16]—signal improved financial flexibility. Yet, liquidity constraints and conditional federal loans introduce risks that could undermine its capital allocation goals.

For investors, the key lies in monitoring PG&E's ability to execute its GRC, secure favorable refinancing terms, and navigate regulatory uncertainties. While the loan appears to align with strategic priorities, its ultimate impact will depend on PG&E's operational efficiency and the stability of its external funding environment.

Comentarios

Aún no hay comentarios