Pfizer's Undervaluation Paradox: Market Sentiment vs. Fundamentals

The stock market has long been a theater of contradictions, and PfizerPFE-- (NYSE: PFE) exemplifies this paradox in 2025. Despite posting robust financial performance and reaffirming revenue guidance, the company's shares trade at a valuation discount that seems disconnected from its fundamentals. This disconnect raises a critical question: Is Pfizer's undervaluation a mispricing born of short-term market sentiment, or does it reflect deeper structural risks?

Fundamentals: A Story of Resilience

Pfizer's financials tell a tale of adaptation. In 2023, the company faced a 42% operational revenue decline due to waning demand for its pandemic-era products, yet non-COVID revenue grew 7% year-over-year, driven by Eliquis, Xtandi, and new launches, according to a Valuesense analysis. By 2024, full-year revenues rebounded to $63.6 billion, a 7% increase, with non-COVID growth accelerating to 12%, per a Biospace release. Profitability metrics also normalized: Net profit margins improved from 3.56% in 2023 to 12.62% in 2024, reflecting cost discipline and portfolio optimization, according to the Valuesense analysis.

Looking ahead, Pfizer has reaffirmed 2025 guidance of $61–64 billion in revenue, a range that implies continued growth despite headwinds like U.S. Medicare price controls, as noted in the Biospace release. These fundamentals suggest a company in transition, leveraging its R&D pipeline and operational efficiency to offset post-pandemic challenges.

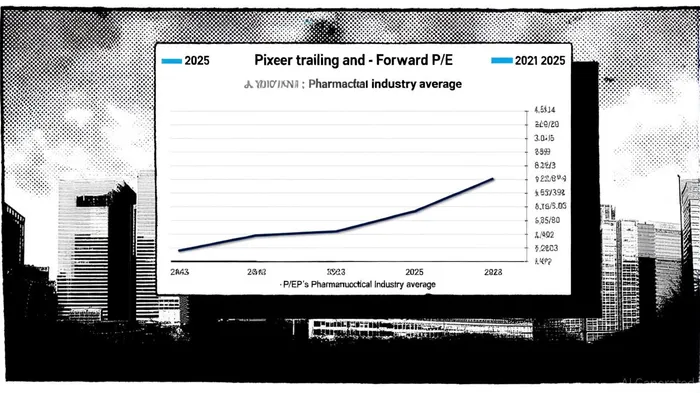

Valuation: A Discount That Defies Logic

Pfizer's valuation metrics underscore its undervaluation. As of late 2025, the stock trades at a trailing P/E of 13 and a forward P/E of 8.5, far below the pharmaceutical industry average of 25.34, according to the Valuesense analysis. Its price-to-book ratio of 1.55 further highlights the gap between market perception and asset value, per CompaniesMarketCap. Analysts argue this discount is irrational, given Pfizer's strong cash flow, 7% dividend yield, and a manageable payout ratio, as described in the Biospace release.

The disconnect is even more pronounced when considering valuation models. A narrative-based analysis estimates a fair value of $30.62 per share, while discounted cash flow (DCF) models suggest similar upside, according to the Valuesense analysis. At a recent closing price of $23.60, the stock offers a 25% potential return based on these estimates, assuming fundamentals hold.

Market Sentiment: Overreacting to Short-Term Risks

The market's skepticism stems from several factors. Legal challenges, including antitrust settlements and patent disputes over its COVID-19 vaccine, have clouded investor sentiment, as noted in the Valuesense analysis. Additionally, the obesity drug market—where Pfizer recently acquired Metsera—introduces competitive risks as rivals like Novo Nordisk dominate, a point raised in the Biospace release.

However, these concerns may be overblown. Pfizer's R&D pipeline, including Phase 3 trial data for a next-generation vaccine, hints at long-term growth potential, according to the Valuesense analysis. The company's strategic pivot in oncology partnerships and cost-cutting initiatives also position it to navigate patent expirations and regulatory shifts, as discussed in the Biospace release.

Investment Thesis: Balancing Risks and Rewards

Pfizer's undervaluation presents a compelling case for value investors. The stock's low P/E ratio and high dividend yield make it attractive for income-focused portfolios, while its R&D-driven growth story offers capital appreciation potential. However, risks remain: Patent expirations for key drugs like Eliquis could pressure margins, and the obesity market's competitive dynamics are uncertain, as highlighted in the Biospace release.

Analysts project a mixed outlook, with a consensus “Hold” rating and a 12-month price target of $29–$30, according to the Valuesense analysis. Algorithmic models suggest a broader range of $23.20–$38, reflecting divergent views on the company's ability to execute its strategic priorities, per CompaniesMarketCap.

Conclusion

Pfizer's undervaluation is a classic case of market sentiment overshadowing fundamentals. While short-term risks like legal challenges and patent cliffs are valid, they appear to be overweighted in current valuations. For investors with a medium-term horizon, the stock offers an attractive risk-reward profile, provided the company can capitalize on its R&D pipeline and operational strengths.

Comentarios

Aún no hay comentarios