Pfizer's Dividend Reliability: A High-Yield Haven Amid Big Pharma's Uncertain Pipeline

For income-focused investors navigating a low-yield market, PfizerPFE-- (PFE) has emerged as a tantalizing option. With a dividend yield of 6.87% as of July 2025—nearly triple the pharmaceutical sector average of 1.89%—the stock offers a compelling income stream[2]. However, this high yield comes with caveats. While Pfizer's payout ratio of 90.5% raises concerns about long-term sustainability[2], its dividend history—marked by a 2022 increase and a recent $0.43 per share payout—suggests short-term reliability[6]. This article argues that income investors should prioritize Pfizer's yield and capital stability over its speculative drug bets, which face significant headwinds from patent expirations and pipeline uncertainties.

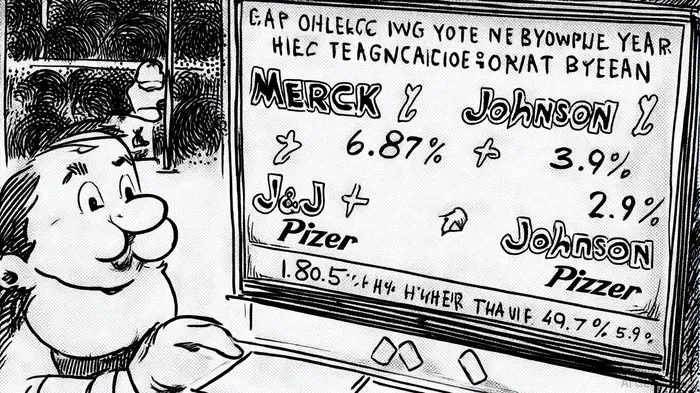

The Allure of Yield in a Low-Growth Sector

Pfizer's dividend yield dwarfs those of its peers. Merck (MRK) and Johnson & Johnson (JNJ) offer 3.9% and 2.9% yields, respectively, while maintaining more conservative payout ratios of 49.7% and 53.9%[1][3]. These companies also boast stronger financial metrics: J&J's debt-to-equity ratio of 0.65 and interest coverage ratio of 33.48 signal robust solvency[3], while Merck's $8.007 billion in cash reserves provide a buffer against volatility[4]. By contrast, Pfizer's 90.5% payout ratio leaves little room for error, particularly as its debt-to-equity ratio stands at 0.70—a slight improvement from June 2025's 1.32 but still higher than its peers[2][4].

Patent Cliffs and Pipeline Risks Undermine Growth Hopes

Pfizer's long-term dividend sustainability hinges on its ability to offset revenue declines from expiring patents on key drugs like Ibrance and Eliquis. Analysts predict earnings contraction through 2029[1], a trend exacerbated by reduced demand for its COVID-19 vaccine and antiviral. While the $43 billion acquisition of Seagen aims to bolster its oncology portfolio, the pharmaceutical industry's notoriously low success rates—less than 30% for drugs advancing from Phase II to III—make speculative bets risky[5]. Merck and J&J, by contrast, have diversified their R&D strategies: Merck spent $17.94 billion on R&D in 2024 (28% of revenue), while J&J invested $13.53 billion (24% of revenue), focusing on high-potential areas like AI-driven drug discovery[4].

Capital Stability Trumps Speculative Growth for Income Investors

While Pfizer's dividend appears secure in the near term—its next payment of $0.43 per share is scheduled for September 2, 2025[6]—long-term investors must weigh the risks of its high payout ratio against the uncertain returns of its pipeline. Merck's 42.86% EBITDA margin and $5.569 billion in free cash flow[4], combined with J&J's disciplined R&D focus, offer more predictable income streams. For investors prioritizing yield over growth, Pfizer's 6.87% return is tempting, but its reliance on a shrinking revenue base and volatile pipeline makes it a less reliable long-term bet than its peers.

Conclusion: A High-Yield Trade-Off

Pfizer's dividend is a double-edged sword: it offers an attractive yield but comes with elevated risks tied to its payout ratio and patent cliffs. Income investors seeking stability may find better value in Merck or J&J, whose lower yields are supported by stronger financial metrics and diversified pipelines. However, for those willing to accept short-term uncertainty in exchange for a high yield, Pfizer remains a viable option—provided they monitor its earnings trajectory and patent expiration schedule closely. In an era where speculative drug bets often fail to deliver, capital preservation and consistent income may prove the more prudent path.

Comentarios

Aún no hay comentarios