Petrus Resources' (TSE:PRQ) Dividend Sustainability: Navigating Risk and Resilience in the Gold Sector

The gold sector, long a refuge for income-focused investors, faces a critical juncture in 2025 as macroeconomic volatility and rising interest rates test the resilience of dividend-paying companies. Petrus Resources (TSE:PRQ), a Canadian gold producer with a 6.90% yield, has drawn attention for its aggressive payout policy. However, the sustainability of its dividend hinges on a delicate balance between operational efficiency, debt management, and market conditions. This analysis evaluates Petrus Resources' dividend sustainability through the lens of its financial metrics, operational costs, and capital allocation strategy.

Operating Cash Flow and Cost Efficiency: A Mixed Picture

Petrus Resources reported operating cash flow of C$4.28 million in Q2 2025, according to TipRanks, a modest figure for a company with a market capitalization of over CAD 1 billion. While this represents a slight improvement from Q1 2025, the company's operating expenses averaged $6.10 per boe (barrel of oil equivalent) in Q2, down 10% from $6.76/boe in the prior quarter, as noted in a MarketBeat alert. This reduction, driven by lower field-related expenditures and a 30% decline in well design costs, is also reflected on MarketBeat's dividend page, and suggests operational discipline. However, the company's generated funds flow-$12.3 million in Q2-was only marginally higher than its dividend payout of $3.8 million, the MarketBeat alert noted, indicating thin margins.

Debt Load and Financial Leverage: A Double-Edged Sword

Petrus Resources' debt-to-equity ratio of 19.79 is alarmingly high, per MarketBeat's dividend page, signaling significant financial leverage. This metric, combined with the absence of explicit all-in sustaining costs (AISC) data, raises concerns about the company's ability to service debt while maintaining dividend payments. High debt levels amplify vulnerability to interest rate hikes and gold price fluctuations, both of which could strain cash flow. For context, the gold sector's average debt-to-equity ratio in 2025 is approximately 2.5, making Petrus Resources' leverage an outlier, according to a GlobeNewswire release.

Dividend Payout Ratios: Contradictions and Context

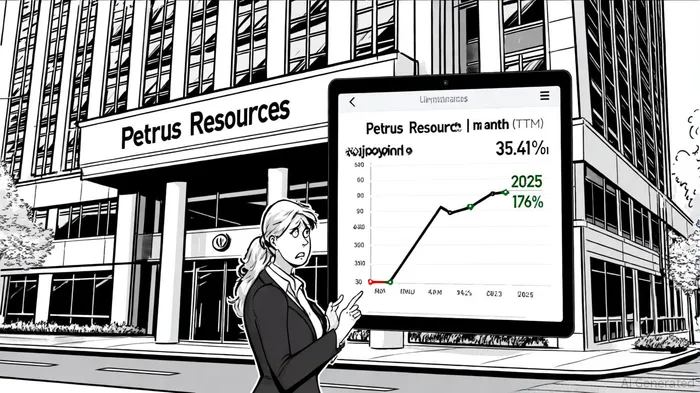

The most contentious issue is Petrus Resources' dividend payout ratio. According to trailing twelve-month (TTM) earnings, the ratio stands at 35.41%, per MarketBeat's dividend page, a level typically deemed sustainable. However, projections based on 2025 earnings estimates suggest a staggering 176% payout ratio, a figure cited in the MarketBeat alert, implying the company is paying out more in dividends than it earns. This discrepancy likely stems from differing methodologies: the 35.41% figure is based on net income, while the 176% figure appears to use cash flow or earnings before interest and taxes (EBIT).

Data from Yahoo further complicates the picture, reporting a cash flow-based payout ratio of 235.77%, which underscores the risk of over-reliance on short-term cash flow rather than earnings. For income investors, this inconsistency is a red flag. A sustainable payout ratio generally falls below 60%, as higher ratios often precede dividend cuts - a point echoed in Petrus' own 2025 budget guidance.

Capital Allocation and Future Outlook

Petrus Resources' 2025 budget guidance allocates $40–50 million toward capital expenditures, with 70% directed to high-impact drilling in its Ferrier and North Ferrier regions. While this investment could boost production and cash flow in the long term, it also diverts funds from debt reduction-a critical priority given the company's leverage. The remaining capital will fund infrastructure projects, such as pipeline expansions, which may enhance operational efficiency but do not directly address liquidity risks.

Conclusion: A High-Yield Gamble in a Volatile Sector

Petrus Resources' 6.90% yield is enticing, but its dividend sustainability remains precarious. The company's high debt-to-equity ratio, conflicting payout ratios, and thin operating margins create a volatile risk profile. While cost reductions and capital investments offer hope for future growth, these measures may not offset the immediate pressures of debt servicing and gold price volatility.

For income investors, the key takeaway is caution. Petrus Resources' dividend appears resilient in the short term but carries significant downside risk. Diversification and close monitoring of gold prices, interest rates, and the company's debt trajectory are essential. In a sector where resilience is paramount, Petrus Resources' dividend sustainability will ultimately depend on its ability to align its aggressive payout with a more conservative financial strategy.

Comentarios

Aún no hay comentarios