The Persson Family's H&M Stake Surge: A Prelude to Privatization?

The Persson family, founders of H&M, has embarked on an unprecedented share-buying campaign since 2023, transforming their stake in the company from 35.5% to over 64% by mid-2025. This aggressive accumulation of shares raises critical questions: Is this a strategic move to secure control, or a prelude to a full-scale take-private transaction by 2030? Let's dissect the data, motivations, and market dynamics to assess the implications for investors.

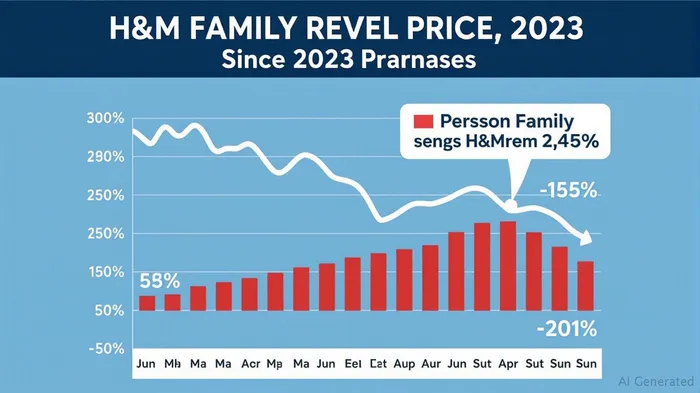

The Share Purchase Surge: A Timeline of Accumulation

The Persson family's buying spree has followed a clear trajectory:

- 2023: Purchased 55.65 million shares, pushing their stake to 42%.

- 2024: Added another 56.85 million shares, reaching 53%.

- 2025: Accelerated purchases to 42.75 million shares by June alone, surpassing the previous two years' totals.

By mid-2025, their combined holdings with affiliates exceed 64%, a near-majority stake. This rapid ascent—fueled by reinvested dividends and strategic purchases—suggests a long game. The family has invested over $6.6 billion since 2016 to reach this milestone, signaling both financial commitment and strategic intent.

Strategic Implications: Why Now?

Analysts point to several motives behind the accelerated buying:

1. Control Over Strategy: With H&M's sales declining (a 1% drop in early 2025) and profits plummeting (27.8% year-on-year), the family may seek to steer the company toward a turnaround without public market pressures.

2. Privatization Feasibility: A stock price decline of nearly 9% in early 2025 has reduced the cost of a potential buyout. At a $23.3 billion market cap, a full take-private would require $8.4 billion to acquire the remaining 36%—a daunting sum, but achievable with financing or partnerships.

3. Market Conditions: Retailers face headwinds like tariffs, inflation, and shifting consumer preferences. Privatization could insulate H&M from volatile equity markets while allowing flexibility in restructuring.

Deutsche Bank's Adam Cochrane notes, “The family's dividend reinvestment creates a self-funding mechanism. By 2030, they could own 80% or more, making a full buyout viable.” However, H&M has remained silent on privatization, redirecting inquiries to Ramsbury Invest, which also declines to comment.

Market Valuation Dynamics: A Bargain or a Trap?

H&M's current valuation presents a paradox:

- Low Stock Price: The recent dip to $23.3 billion creates a “fire sale” opportunity for the Perssons.

- Debt Risks: A take-private would require significant debt or equity partners. H&M's $2.2 billion in debt (as of Q1 2025) adds complexity.

- Public Market Sentiment: Investors may already be pricing in a “privatization discount,” but a formal announcement could trigger a short-term rally as shares are bought out at a premium.

Feasibility of a Take-Private by 2030

While plausible, execution hinges on several factors:

1. Ownership Threshold: The Persson family needs to secure at least 90% of shares to delist under Swedish law, requiring another $15 billion in purchases.

2. External Financing: A $23 billion valuation demands partnerships with private equity firms or strategic buyers—a high-risk proposition in a volatile retail sector.

3. Regulatory Scrutiny: Any buyout must navigate antitrust and shareholder approval hurdles.

Investment Implications: To Buy or to Bail?

For investors, the Persson family's moves present a nuanced opportunity:

- Short-Term Play: If rumors of privatization intensify, shares could rise as buyers anticipate a premium. Monitor for any formal announcements or accelerated purchases.

- Long-Term Caution: Without a turnaround in H&M's fundamentals (slowing store growth, weak online sales), the stock remains risky.

- Dividend Reinvestment Angle: The family's strategy hints at confidence in H&M's long-term value, but public shareholders may face diluted returns if a buyout reduces liquidity.

Conclusion: A Glimmer of Privatization, but Risks Remain

The Persson family's stake-building is a clear signal of intent, but a full take-private by 2030 is far from certain. Investors should weigh the potential upside of a buyout premium against the risks of H&M's stagnant performance and the capital-intensive path to privatization. For now, the stock's valuation offers a speculative entry point—but stay prepared for volatility. As the saying goes, “founders know best,” and the Perssons are clearly doubling down.

Final thought: If history is a guide, family-led buyouts often follow when public markets undervalue legacy brands. H&M's next chapter could hinge on whether the Perssons see this as their last stand—or their best move yet.

Comentarios

Aún no hay comentarios