Personal Loan Market Dynamics and Investor Opportunities: Evaluating Non-Interest Risk Factors in Loan Portfolios

The personal loan market has emerged as a critical segment of consumer finance, driven by evolving borrower behavior and macroeconomic pressures. However, as outstanding balances surge and economic uncertainty persists, investors must navigate a complex landscape of non-interest risk factors. These include borrower financial stress, cyclical borrowing patterns, and systemic risks from private credit expansion. This analysis explores how these dynamics shape investor opportunities and outlines actionable strategies to mitigate risks while capitalizing on growth.

Rising Debt and Behavioral Risks: A Double-Edged Sword

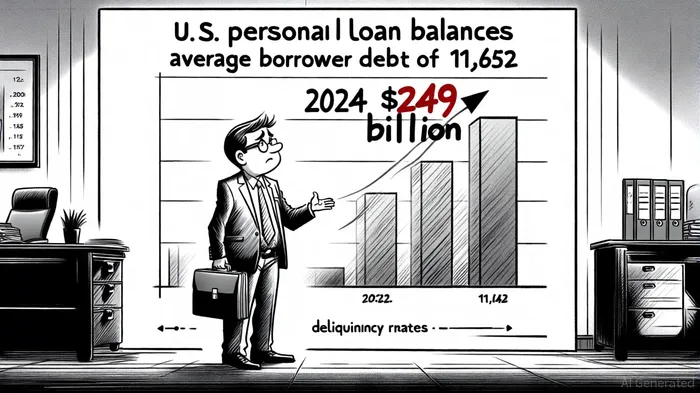

According to a report by the Bureau of Industry and Commerce (Bai.org), U.S. personal loan balances reached $249 billion in 2024, with an average debt per borrower of $11,652-a 35% increase since 2022 [1]. This growth is fueled by high living costs and trade tensions, which have pushed consumers to rely on financial institutions for guidance. Yet, behavioral patterns reveal a troubling cycle: a TransUnionTRU-- survey found that 42% of borrowers who consolidate credit card debt into personal loans revert to similar spending habits within 12 months, exacerbating long-term financial instability [4].

Such trends underscore the importance of transparency in lending practices. Financial institutions must prioritize borrower education and responsible credit solutions to avoid contributing to a debt spiral. For investors, this highlights the need for rigorous underwriting standards and continuous monitoring of borrower behavior to preempt defaults.

Strategic Diversification and Data-Driven Risk Management

Investor strategies for managing non-interest risks increasingly emphasize diversification and advanced analytics. Diversifying across borrower profiles, industries, and geographies reduces concentration risk, as sector-specific downturns have less impact on a broad portfolio [3]. For example, Redwood Community Bank's 2025 case study demonstrated how Probability of Default (PD) and Loss Given Default (LGD) models, combined with historical data, enabled the institution to refine risk-adjusted pricing and align with CECL compliance requirements [1]. The analysis revealed unsecured consumer loans carried an average PD of 3.60% and LGD of 110%, prompting targeted adjustments to loan terms and collateral requirements.

Data-driven tools such as credit scoring models and automation further enhance risk assessment. By integrating real-time borrower data, lenders can identify early warning signs of financial stress, such as sudden delinquency spikes or shifts in spending patterns [4]. These insights allow for proactive interventions, including loan restructuring or temporary relief programs, which mitigate non-performing loan (NPL) risks while preserving net interest income [2].

Structured Notes and Alternative Investments: Hedging Against Uncertainty

Structured notes have gained traction as a tool to hedge non-interest risks in personal loan portfolios. These instruments, which combine fixed-income features with derivative components, offer downside protection while allowing market participation. For instance, a 54-week structured note tied to the S&P 500 with a 15% buffer would have preserved principal in 93% of historical scenarios over the past two decades [3]. This makes them particularly appealing for investors seeking to offset potential losses from volatile borrower behavior or economic downturns.

Alternative investments, such as private credit and infrastructure, also provide diversification benefits. These assets generate stable cash flows and higher yields compared to public market equivalents, offering resilience during periods of market volatility [3]. For example, private credit funds have grown to $1.2 trillion in assets under management by 2025, with banks increasingly providing credit lines to these funds. While this expansion introduces indirect risks-such as heightened exposure to credit defaults-it also creates opportunities for investors to access non-traditional markets with disciplined risk management frameworks [2].

Regulatory and Systemic Considerations

Regulatory scrutiny remains a key factor in managing non-interest risks. The Federal Reserve and banking regulators have intensified stress testing requirements, particularly for commercial real estate and consumer lending portfolios [3]. Institutions must align with these standards by incorporating scenario analysis and liquidity stress tests into their risk management protocols. For investors, this means prioritizing lenders with robust compliance frameworks and transparent risk disclosures.

Systemic risks, such as the interplay between private credit growth and bank balance sheets, also demand attention. As banks extend credit lines to private credit funds, they face potential liquidity strains if these funds underperform. Investors should evaluate the creditworthiness of both the fund managers and the underlying collateral to ensure alignment with their risk tolerance [2].

Future Outlook and Actionable Opportunities

The personal loan market is poised for continued growth, but success will hinge on managing non-interest risks through innovation and adaptability. Fintech partnerships, for instance, enable banks to scale lending while maintaining responsible credit solutions through AI-driven underwriting and borrower analytics [1]. Similarly, structured notes and alternative investments offer scalable tools to hedge against macroeconomic shocks.

For investors, the path forward involves a balanced approach: leveraging data analytics to refine risk assessments, diversifying portfolios to mitigate sector-specific vulnerabilities, and adopting structured products to protect against downside scenarios. As the market evolves, those who integrate these strategies will be best positioned to capitalize on opportunities while safeguarding long-term profitability.

Comentarios

Aún no hay comentarios