PermRock Royalty Trust: Assessing Dividend Sustainability in a Volatile Energy Sector

For income-focused investors, royalty trusts like PermRock Royalty TrustPRT-- (PRT) have long been a staple of high-yield portfolios. Yet, as the energy sector grapples with macroeconomic headwinds and shifting commodity dynamics in 2025, the sustainability of PRT's dividend remains a critical question. This analysis examines PRT's financial health, operational performance, and exposure to sector-wide risks to evaluate whether its 11.42% annualized yield[3] is a compelling opportunity or a precarious gamble.

Dividend Payouts and Revenue Trends: A Tale of Two Cycles

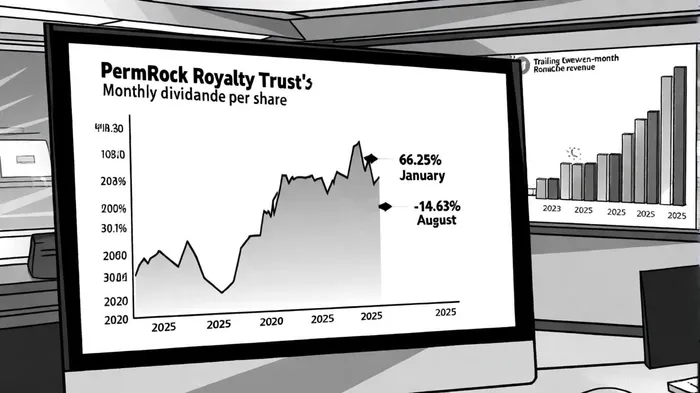

PermRock's dividend history reveals a pattern of volatility rather than consistency. While the trust surged to a peak of $0.0503 per share in January 2025—a 66.25% increase from December 2024—subsequent months saw sharp declines, including a -14.63% drop to $0.0277 per share in August 2025[3]. This erratic trajectory is mirrored in its revenue, which fell from $7.18 million in 2023 to $6.01 million in 2024, with trailing twelve-month (TTM) revenue at $6.31 million as of September 2025[4].

The disconnect between production volumes and pricing further complicates the picture. For instance, Q3 2025 saw oil cash receipts rise to $1.38 million in July 2025, driven by higher prices and sales volumes[1], yet natural gas receipts stagnated at $0.06 million due to offsetting volume and price shifts[2]. This duality underscores the trust's reliance on commodity price swings, which remain a double-edged sword for income stability.

Payout Ratios and Financial Leverage: A High-Stakes Balance

PRT's dividend payout ratio of 75.65%[3] suggests a heavy reliance on current earnings to fund distributions, leaving little room for operational shocks. While this ratio is not uncommon for royalty trusts, it becomes concerning when paired with declining revenue and a dividend growth potential score of 0%[4]. The trust's low dividend sustainability score of 50%[4] further signals that investors should approach its yield with caution.

Financially, PRTPRT-- operates without traditional debt but faces structural challenges. Its liabilities include distribution payables (e.g., $539,693 as of June 2025[1]) and cash reserves of $1.0 million[5], which are modest relative to its $70.22 million net profits interest[5]. However, the amortization of its Net Profits Interest—down to $70.22 million from $72.38 million in 2024[5]—highlights the finite nature of its underlying assets. For royalty trusts, this depletion is inevitable, but the pace at which it occurs directly impacts long-term dividend viability.

Macroeconomic Headwinds: Policy, Prices, and Portfolio Diversification

The energy sector in 2025 is shaped by two opposing forces: the push for clean energy and the persistence of fossil fuel demand. PRT's focus on the Permian Basin—a hub for oil production—positions it to benefit from near-term oil price resilience. For example, July 2025 oil prices averaged $67.55 per barrel[1], supporting higher cash receipts. Yet, the trust's exposure to natural gas—a commodity prone to price volatility—introduces risk, as seen in the 11.1% decline in natural gas volumes during February 2025[1].

Geopolitical tensions and U.S. trade policies also loom large. The Trump administration's proposed withdrawal from the Paris Agreement and potential tariffs could disrupt global energy demand, creating uncertainty for royalty trusts reliant on commodity prices[6]. Meanwhile, the IEA's World Energy Investment 2025 report notes a growing divergence between clean energy and fossil fuel investments, with the latter facing stricter regulatory scrutiny[7]. While PRT's structure is tied to finite hydrocarbon assets, its lack of diversification into renewables—a trend gaining traction among peers[8]—limits its adaptability to long-term sector shifts.

Conclusion: A High-Yield Proposition with Caveats

PermRock Royalty Trust's 11.42% yield[3] is undeniably attractive in a low-interest-rate environment, particularly for investors seeking immediate income. However, its declining revenue, volatile dividend history, and structural depletion of assets suggest that this yield is not a given. The trust's operational efficiency—evidenced by reduced operating expenses in Q3 2025[1]—is a positive, but it may not offset broader sector headwinds.

Historical backtesting of PRT's earnings release events from 2022 to 2025 reveals critical insights for buy-and-hold strategies. Over 14 analyzed events, cumulative returns were negative (-4.6%) over 30 days post-announcement, with a win rate below 35% after the second week[9]. These findings underscore that earnings-driven strategies for PRT have historically lacked reliability, with market reactions flattening within days of announcements. Investors must weigh these patterns against the trust's current yield, recognizing that past performance does not guarantee future results.

For income stability, investors must weigh PRT's current yield against its long-term sustainability. While the trust's recent performance demonstrates resilience in a challenging market, the finite nature of its assets and macroeconomic uncertainties warrant a cautious approach. Those willing to accept short-term volatility for high yields may find PRT compelling, but they should monitor production trends, commodity prices, and regulatory developments closely.

Comentarios

Aún no hay comentarios