PepGen Inc.'s Breakthrough in Myotonic Dystrophy Type 1 Treatment: A New Dawn for Rare Disease Therapeutics

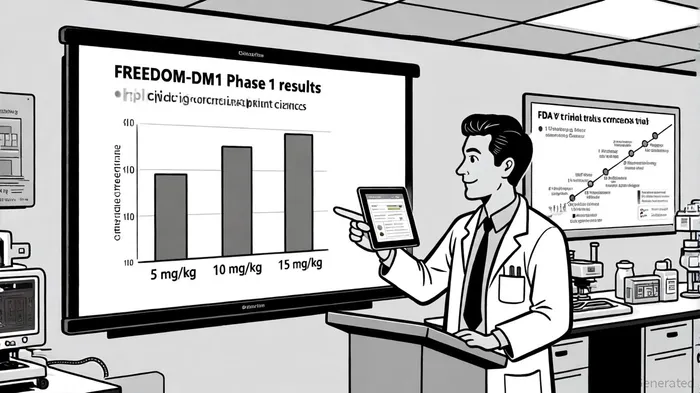

In the annals of biotech innovation, few developments have captured the imagination of investors and clinicians alike as swiftly as PepGenPEPG-- Inc.'s FREEDOM-DM1 Phase 1 trial. The results, announced in late September 2025, represent not just a scientific leap but a recalibration of expectations for rare disease therapeutics. According to a report by Business Wire, a single 15 mg/kg dose of PGN-EDODM1 achieved a mean splicing correction of 53.7% in patients with myotonic dystrophy type 1 (DM1), a figure that dwarfs prior outcomes at lower doses (12.3% at 5 mg/kg and 29.1% at 10 mg/kg) and underscores the therapy's potential to address the root cause of this debilitating genetic disorder [2]. For investors, this is more than a data point—it is a signal of a company poised to redefine the therapeutic landscape for a condition that has long eluded effective treatment.

The implications of these findings extend beyond the clinical realm. PepGen's Enhanced Delivery Oligonucleotide (EDO) platform, which underpins PGN-EDODM1, has demonstrated a capacity to achieve unprecedented splicing correction while maintaining a favorable safety profile. Notably, the therapy was well-tolerated, with only mild or moderate treatment-related adverse events reported—none of which required intervention [2]. This dual achievement of efficacy and safety is rare in early-stage gene-targeted therapies and positions PepGen to advance swiftly to the next phase of trials. The company's upcoming FREEDOM2-DM1 multiple ascending dose (MAD) study, with results from the 5 mg/kg cohort expected in early 2026, will be a critical inflection point for both scientific validation and investor sentiment.

Financially, PepGen operates in a precarious but navigable space. As of Q2 2025, the company reported $98 million in cash and marketable securities, a balance that, while under pressure from a trailing twelve-month cash burn of $91 million , provides a runway to advance its DM1 program without immediate dilution. This financial buffer is a boon for investors wary of the capital-intensive nature of biotech development. However, the company's decision to pivot focus from its Duchenne muscular dystrophy (DMD) program, PGN-EDO51, to DM1 signals a strategic recalibration—one that prioritizes near-term clinical milestones in a market with fewer competitors and higher unmet need [1]. Analysts at Guggenheim have reiterated a “buy” rating for PepGen, citing the company's differentiated platform and the growing demand for curative therapies in rare diseases [3].

The competitive landscape for DM1 treatments, though still nascent, is intensifying. Key players such as Biogen, Ionis Pharmaceuticals, and Sarepta Therapeutics are advancing antisense oligonucleotides and gene therapies, but PepGen's EDO platform offers a unique edge: its ability to achieve high splicing correction with a single dose. As noted in a market analysis by DataInsightsMarket, North America and Europe dominate the DM1 therapeutics market, driven by robust regulatory frameworks and a concentration of clinical expertise [2]. For PepGen, this means a clear path to regulatory engagement and potential partnerships, particularly as gene therapy emerges as the dominant modality for genetic disorders.

Yet, the road ahead is not without risks. The high cash burn rate raises questions about long-term sustainability, and the absence of a marketed product means PepGen remains a speculative bet. Moreover, the rarity of DM1 (estimated to affect 1 in 8,000 individuals globally) limits the immediate commercial potential, even if PGN-EDODM1 secures approval. Investors must weigh these factors against the broader trend of biotech innovation, where breakthroughs in RNA-targeted therapies are increasingly translating into blockbuster markets. PepGen's success in DM1 could serve as a springboard for its EDO platform in other neuromuscular diseases, including DMD and spinal muscular atrophy, thereby expanding its addressable market.

In conclusion, PepGen's FREEDOM-DM1 trial represents a pivotal moment in the quest for curative therapies for rare diseases. The data, while preliminary, suggest a therapy that could transform the lives of DM1 patients and validate the EDO platform as a next-generation tool for genetic medicine. For investors, the challenge lies in balancing the promise of these results with the inherent uncertainties of clinical development. Yet, in an era where biotech innovation is increasingly defined by precision and durability, PepGen's progress offers a compelling case for optimism—and a reminder that the most significant breakthroughs often emerge from the most unexpected places.

Comentarios

Aún no hay comentarios