"Is PDD Holdings Inc. (PDD) the Most Undervalued Large Cap Stock to Buy Now?"

Generado por agente de IAMarcus Lee

domingo, 9 de marzo de 2025, 5:04 pm ET2 min de lectura

PDD--

In the ever-evolving landscape of e-commerce, PDD HoldingsPDD-- Inc. (PDD) has emerged as a formidable player, yet its stock remains relatively undervalued compared to its peers. With a market capitalization of $26.906 billion, PDD's performance metrics paint a picture of a company on the rise, but is it the most undervalued large-cap stock to buy now? Let's dive in.

The Bull Case for PDD

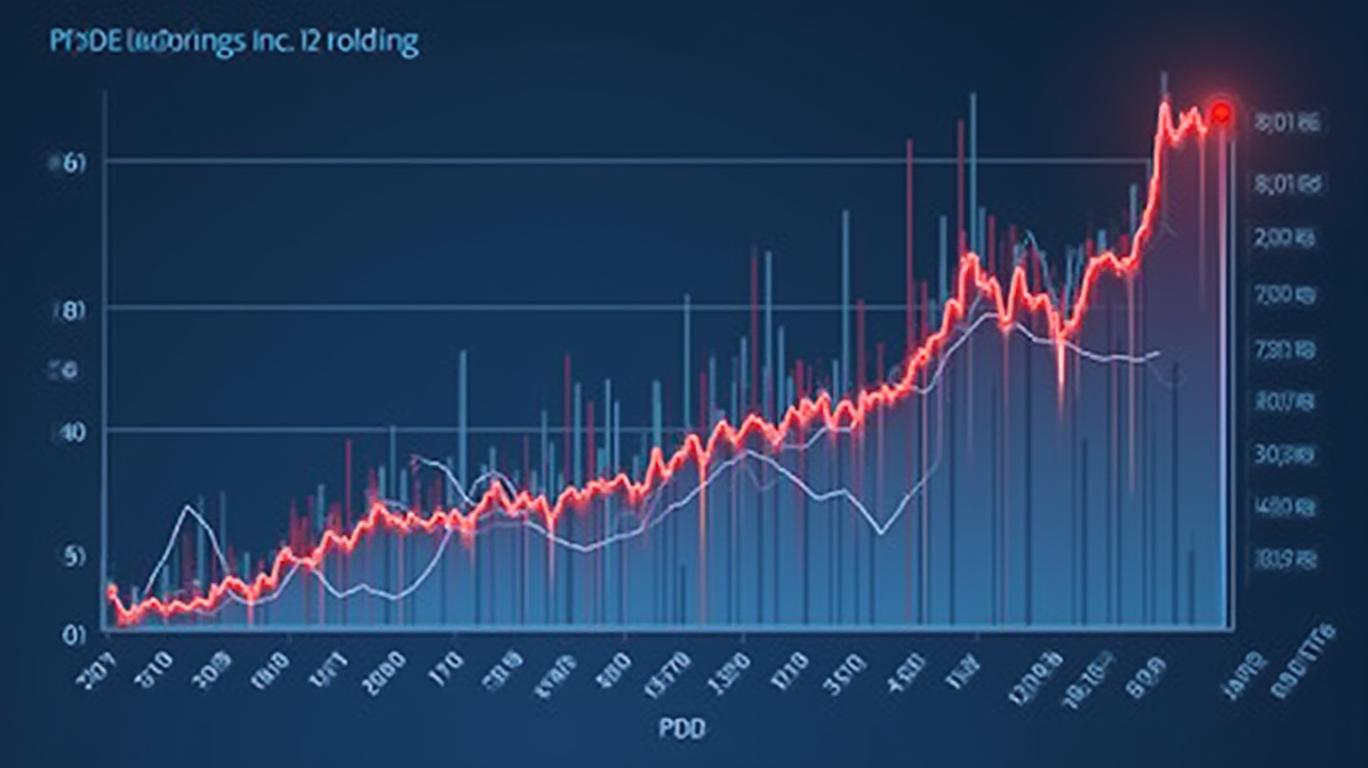

PDD Holdings has shown remarkable growth over the past year, with a total return of 88.93% compared to the S&P 500's 27.85%. This performance is not just a flash in the pan; over the past five years, PDD's total return stands at an impressive 496.92%, dwarfing the S&P 500's 107.63%. This kind of growth is typically associated with smaller, more volatile stocks, not a large-cap company like PDDPDD--.

The company's revenue growth is equally impressive. With a revenue CAGR (Compound Annual Growth Rate) of 105.14% over the trailing twelve months, 58.03% over the past three years, and 78.60% over the past five years, PDD is growing at a pace that outstrips many of its competitors. For instance, Amazon.com (AMZN), a behemoth in the e-commerce sector, has a total return CAGR of 31.09% over the past year, significantly lower than PDD's 88.93%.

Profitability and Free Cash Flow

PDD's profitability metrics are also noteworthy. The company's profit margin of 26.93% is in the top 25% of its industry and is higher than its 3-year average of 15.65% and 5-year average of -1.74%. This indicates that PDD is not only growing its top line but also improving its bottom line.

The free cash flow CAGR for PDD is 92.97% over the TTM, 65.61% over the past three years, and 82.57% over the past five years. This strong free cash flow growth suggests that the company has ample liquidity to invest in growth opportunities and return value to shareholders.

Analyst Sentiment

Analysts seem to agree that PDD has room for growth. The average price target for PDD Holdings is $141.50, representing an 18.00% upside from the last price of $119.92. The highest price target is $158.00, suggesting that some analysts see significant upside potential in the stock.

The Bear Case for PDD

Despite these impressive metrics, PDD is not without its risks. The company operates in a highly competitive e-commerce market, both domestically in China and internationally. In China, it competes with major players like Alibaba Group (BABA) through its Taobao and Tmall platforms, JD.com (JD), and Dada Nexus (DADA) in local retail and delivery. Globally, through its Temu platform, it competes with Amazon (AMZN), Shopify (SHOP), Coupang (CPNG), and Shein (a private company). This intense competition could pressure PDD's market share and profitability.

Regulatory risks are another concern. As an e-commerce company operating in multiple jurisdictions, PDD Holdings is subject to various regulatory environments. Changes in regulations, such as those related to data privacy, e-commerce practices, and cross-border trade, could impact its operations and financial performance.

Economic downturns can also significantly affect consumer spending, which is a critical driver of e-commerce sales. A slowdown in economic growth could lead to reduced consumer discretionary spending, impacting PDD's revenue and profitability.

Conclusion

In conclusion, PDD Holdings Inc. (PDD) presents a compelling case as an undervalued large-cap stock. Its strong performance metrics, rapid revenue growth, high profitability, and positive analyst sentiment all suggest that it has significant potential for future growth. However, investors should be aware of the risks and challenges that the company faces, including intense competition, regulatory risks, and economic downturns.

For those willing to take on these risks, PDD Holdings could be a valuable addition to their portfolio. But as with any investment, it's essential to do your own research and consider your risk tolerance before making a decision.

In the ever-evolving landscape of e-commerce, PDD HoldingsPDD-- Inc. (PDD) has emerged as a formidable player, yet its stock remains relatively undervalued compared to its peers. With a market capitalization of $26.906 billion, PDD's performance metrics paint a picture of a company on the rise, but is it the most undervalued large-cap stock to buy now? Let's dive in.

The Bull Case for PDD

PDD Holdings has shown remarkable growth over the past year, with a total return of 88.93% compared to the S&P 500's 27.85%. This performance is not just a flash in the pan; over the past five years, PDD's total return stands at an impressive 496.92%, dwarfing the S&P 500's 107.63%. This kind of growth is typically associated with smaller, more volatile stocks, not a large-cap company like PDDPDD--.

The company's revenue growth is equally impressive. With a revenue CAGR (Compound Annual Growth Rate) of 105.14% over the trailing twelve months, 58.03% over the past three years, and 78.60% over the past five years, PDD is growing at a pace that outstrips many of its competitors. For instance, Amazon.com (AMZN), a behemoth in the e-commerce sector, has a total return CAGR of 31.09% over the past year, significantly lower than PDD's 88.93%.

Profitability and Free Cash Flow

PDD's profitability metrics are also noteworthy. The company's profit margin of 26.93% is in the top 25% of its industry and is higher than its 3-year average of 15.65% and 5-year average of -1.74%. This indicates that PDD is not only growing its top line but also improving its bottom line.

The free cash flow CAGR for PDD is 92.97% over the TTM, 65.61% over the past three years, and 82.57% over the past five years. This strong free cash flow growth suggests that the company has ample liquidity to invest in growth opportunities and return value to shareholders.

Analyst Sentiment

Analysts seem to agree that PDD has room for growth. The average price target for PDD Holdings is $141.50, representing an 18.00% upside from the last price of $119.92. The highest price target is $158.00, suggesting that some analysts see significant upside potential in the stock.

The Bear Case for PDD

Despite these impressive metrics, PDD is not without its risks. The company operates in a highly competitive e-commerce market, both domestically in China and internationally. In China, it competes with major players like Alibaba Group (BABA) through its Taobao and Tmall platforms, JD.com (JD), and Dada Nexus (DADA) in local retail and delivery. Globally, through its Temu platform, it competes with Amazon (AMZN), Shopify (SHOP), Coupang (CPNG), and Shein (a private company). This intense competition could pressure PDD's market share and profitability.

Regulatory risks are another concern. As an e-commerce company operating in multiple jurisdictions, PDD Holdings is subject to various regulatory environments. Changes in regulations, such as those related to data privacy, e-commerce practices, and cross-border trade, could impact its operations and financial performance.

Economic downturns can also significantly affect consumer spending, which is a critical driver of e-commerce sales. A slowdown in economic growth could lead to reduced consumer discretionary spending, impacting PDD's revenue and profitability.

Conclusion

In conclusion, PDD Holdings Inc. (PDD) presents a compelling case as an undervalued large-cap stock. Its strong performance metrics, rapid revenue growth, high profitability, and positive analyst sentiment all suggest that it has significant potential for future growth. However, investors should be aware of the risks and challenges that the company faces, including intense competition, regulatory risks, and economic downturns.

For those willing to take on these risks, PDD Holdings could be a valuable addition to their portfolio. But as with any investment, it's essential to do your own research and consider your risk tolerance before making a decision.

Divulgación editorial y transparencia de la IA: Ainvest News utiliza tecnología avanzada de Modelos de Lenguaje Largo (LLM) para sintetizar y analizar datos de mercado en tiempo real. Para garantizar los más altos estándares de integridad, cada artículo se somete a un riguroso proceso de verificación con participación humana.

Mientras la IA asiste en el procesamiento de datos y la redacción inicial, un miembro editorial profesional de Ainvest revisa, verifica y aprueba de forma independiente todo el contenido para garantizar su precisión y cumplimiento con los estándares editoriales de Ainvest Fintech Inc. Esta supervisión humana está diseñada para mitigar las alucinaciones de la IA y garantizar el contexto financiero.

Advertencia sobre inversiones: Este contenido se proporciona únicamente con fines informativos y no constituye asesoramiento profesional de inversión, legal o financiero. Los mercados conllevan riesgos inherentes. Se recomienda a los usuarios que realicen una investigación independiente o consulten a un asesor financiero certificado antes de tomar cualquier decisión. Ainvest Fintech Inc. se exime de toda responsabilidad por las acciones tomadas con base en esta información. ¿Encontró un error? Reportar un problema

Comentarios

Aún no hay comentarios