PB Financial's Q3 Earnings Signal Resilience, But Can It Sustain Growth in a Shifting Fintech Landscape?

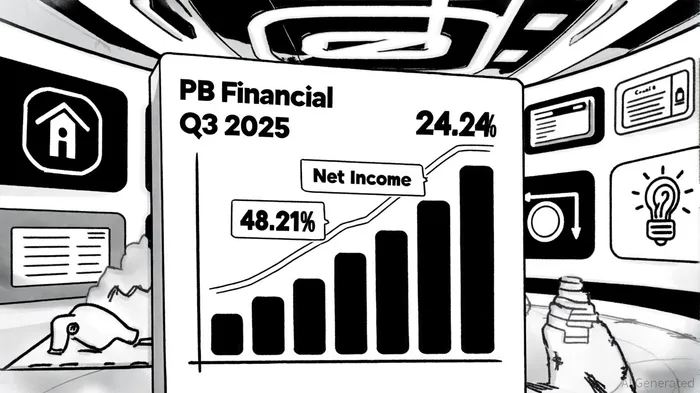

PB Financial Corporation's Q3 2025 earnings, per the company press release, have ignited optimism among investors, with net income surging 24.21% year-on-year to $5.71 million and total assets expanding to $1.391 billion, reflecting an 8.23% increase. This performance underscores the company's ability to capitalize on its core strengths, particularly in insurance broking, where revenue grew 62.4% to ₹1,132 crore, driven by a 47% rise in new health and life insurance premiums, as noted in a Reuters report. However, the broader fintech landscape remains fraught with challenges, including regulatory headwinds and intensifying competition, which could test PB Financial's long-term growth trajectory.

A Dual-Engine Growth Model: Insurance Dominance and Credit Rebalancing

PB Financial's insurance segment has become a flywheel of recurring revenue, with its annualized run rate reaching ₹817 crore in FY25, according to a YourStory feature. This momentum is fueled by strategic shifts, such as prioritizing high-quality insurance agents over sheer volume, which has improved policy renewal rates and customer retention, Market Insiders reported. Meanwhile, the credit segment, while facing a 20% year-on-year decline in unsecured lending due to RBI regulations, has pivoted to secured credit products. This shift has already yielded results: Paisabazaar's secured credit disbursements grew 52% in Q3 2025, mitigating some of the sector's volatility, according to an Economic Times article.

The company's operational efficiency further bolsters its growth story. By optimizing cost allocations and leveraging AI-driven claims processing, PB Financial has reduced overheads while maintaining a 14.69% ROE, per StockAnalysis data. Yet, the aggressive 18% commission cut-three times the industry's expected reduction-signals a defensive strategy to retain market share amid rising customer acquisition costs, according to a ScanX report.

Navigating a Crowded Fintech Arena: Threats and Opportunities

The fintech sector's projected 16.2% CAGR through 2025, per a Fortune Business Insights forecast, masks a fragmented and increasingly competitive environment. PB Financial's dominance in insurance broking (87.6% of total revenue) is being challenged by government-backed platforms like Bima Sugam, which aims to democratize insurance access and could erode PB's take rate, as noted in a Moneycontrol piece. Macquarie analysts warn that Bima Sugam's interoperable model may replicate UPI's disruptive impact on payments, potentially reducing PB Financial's margins by 25% over the long term, according to a Mordor Intelligence report.

Yet, PB Financial's strategic agility offers a counterbalance. Its pivot to fixed-income products in the savings segment and expansion into Tier 2–3 cities-where insurance penetration remains low-position it to capture underserved markets, per a Fintegriti analysis. Additionally, the company's 448% YoY profit surge in FY25, highlighted in a Lapaas report, demonstrates its ability to scale profitability even as it invests heavily in digital marketing (₹15,000 crore in FY25).

Long-Term Viability: Innovation vs. Regulatory Risk

While PB Financial's Q3 results are impressive, its valuation-trading at 50x EV/EBITDA as of September 2027 per StockAnalysis-raises questions about sustainability. Macquarie's "underperform" rating highlights regulatory risks, including stricter digital-lending norms and the zero-MDR policy, which have compressed margins across the fintech sector (Moneycontrol has covered these concerns). However, the company's focus on AI and blockchain adoption aligns with industry trends, offering potential for cost savings and fraud prevention, as outlined in a KPMG briefing.

The global fintech market's resilience, with 69% of publicly listed firms turning profitable in 2024, per DigitalSilk data, suggests that innovation-driven players like PB Financial can thrive. Yet, its reliance on India's under-penetrated insurance and credit markets means macroeconomic shifts-such as rising interest rates or inflation-could disproportionately impact its growth.

Conclusion: A High-Conviction Play with Caveats

PB Financial's Q3 performance validates its position as a fintech leader, but investors must weigh its short-term success against structural risks. The company's insurance renewal flywheel and secured credit pivot are compelling, yet Bima Sugam's emergence and regulatory volatility could temper long-term gains. For those willing to navigate these uncertainties, PB Financial's strategic reinvention and operational discipline present a compelling case for sustained growth-if it can maintain its agility in an increasingly crowded and regulated ecosystem."""

Comentarios

Aún no hay comentarios