Paysign's Q3 2025 Earnings Call: Assessing Market Momentum and Strategic Positioning in Fintech

Paysign, Inc. (NASDAQ: PAYS) is set to host its Q3 2025 earnings call on November 12, 2025, at 5:00 p.m. Eastern Time, offering investors a critical window into its financial performance and strategic direction. With the fintech sector evolving rapidly, Paysign's ability to leverage its niche in healthcare payments will determine its long-term competitiveness. This analysis evaluates the company's market momentum, guided by its Q2 2025 results and Q3 2025 projections, alongside its strategic initiatives to solidify its position in the fintech ecosystem.

Financial Momentum: Strong Revenue Growth, Margin Expansion

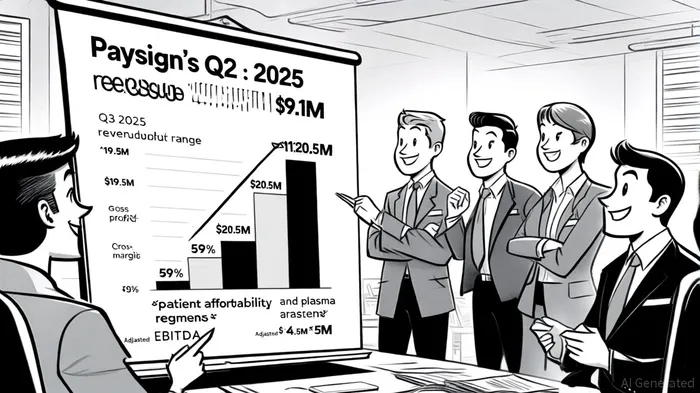

Paysign's Q2 2025 results underscored its resilience, with revenue surging to $19.1 million, a 33% year-over-year increase[2]. The patient affordability segment, a key growth driver, saw a staggering 190% YoY revenue jump to $7.75 million, fueled by new program launches and increased claims processing[4]. For Q3 2025, the company forecasts revenue between $19.5 million and $20.5 million, with plasmaXPL-- compensation accounting for 60% of total revenue and pharma patient affordability contributing 37%[3].

Gross profit margins are expected to remain robust at ~59%, supported by higher plasma revenue and cost efficiencies from its new contact center[3]. Adjusted EBITDA is projected to range between $4.5 million and $5.0 million, representing 23.1% to 24.4% of revenue[3]. These figures reflect Paysign's ability to scale operations while maintaining profitability, a critical factor in a sector where margins often compress under competitive pressure.

Strategic Positioning: Diversification and Technological Innovation

Paysign's strategic initiatives for 2025 are centered on diversifying revenue streams and modernizing its digital infrastructure. The company aims to increase non-plasma revenue to 20% of total revenue by year-end, up from 10% in 2024[1]. This includes launching three major enterprise pharma co-pay assistance programs and securing partnerships with healthcare IT firms to expand market reach[1]. Such moves address the plasma segment's volatility, as evidenced by a 4.7% YoY revenue decline in Q2 2025 due to industry oversupply[4].

Technologically, PaysignPAYS-- is migrating 50% of transaction volume to a cloud-native platform, reducing client onboarding time from 60 to 30 days[1]. A public API for embedded finance is also in the pipeline, enabling third-party integration and unlocking new revenue opportunities. These innovations align with broader fintech trends, where agility and scalability are paramount.

Market Positioning: Leadership in Niche Segments

Paysign's dominance in the plasma donor compensation market-where it holds a 40% market share-provides a stable revenue base[1]. Its 98% gross revenue retention rate and plans to expand digital wallet adoption among plasma donors to 25% within 12 months further reinforce this position[1]. Meanwhile, the patient affordability segment, projected to grow by at least 135% YoY, is becoming a strategic differentiator as pharmaceutical companies prioritize cost-saving solutions for patients[3].

However, challenges persist. The plasma segment's Q2 2025 performance was hampered by $300,000 in one-time onboarding costs for new centers[4], and industry headwinds like oversupply and efficiency gains in plasma collection remain. Paysign's ability to mitigate these risks through diversification will be a key focus during the Q3 2025 call.

Investor Outlook: Strong Buy Consensus and Guidance

Analysts maintain a "Strong Buy" rating for PAYSPAYS--, with a 12-month price target of $8.06[3]. This optimism is underpinned by Paysign's raised 2025 revenue guidance to $76.5 million–$78.5 million, reflecting a 32.7% growth at the midpoint[4]. The company's balance sheet also appears resilient, with $42.2 million in shareholder equity, $0 debt, and $11.8 million in cash and short-term investments[1].

Conclusion: A Fintech Story Built on Healthcare Synergy

Paysign's Q3 2025 earnings call will be pivotal in assessing whether its strategic bets-on diversification, technology, and market expansion-translate into sustained momentum. While the plasma segment remains a cornerstone, the company's pivot toward pharmaceutical patient affordability and digital innovation positions it to capitalize on broader fintech trends. Investors should watch for clarity on Q3 results, particularly in the pharma segment, and how management addresses plasma market challenges.

As the healthcare fintech landscape evolves, Paysign's ability to balance growth with margin preservation will define its trajectory. With a robust balance sheet and a clear roadmap, the company is well-positioned to navigate headwinds and emerge as a leader in its niche.

Comentarios

Aún no hay comentarios