The Payroll Shockwave: How a -911K Revision Supercharges Rate-Cut Bets and Fuels Risk-On Rallies

The U.S. labor market just got a reality check. According to a report by Reuters, the 12-month payrolls data through March 2025 was revised downward by a staggering 911,000 jobs—the largest benchmark adjustment in decades—revealing that monthly job gains averaged just 71,000 instead of the previously reported 147,000[1]. This isn't just a statistical hiccup; it's a seismic shift in the narrative. Key sectors like leisure and hospitality (-176,000), trade (-226,000), and professional services (-158,000) were hit hardest, underscoring a broad-based slowdown[1]. The implications? The Federal Reserve's dovish pivot is no longer a question of if but how aggressively.

The Fed's Dovish Domino Effect

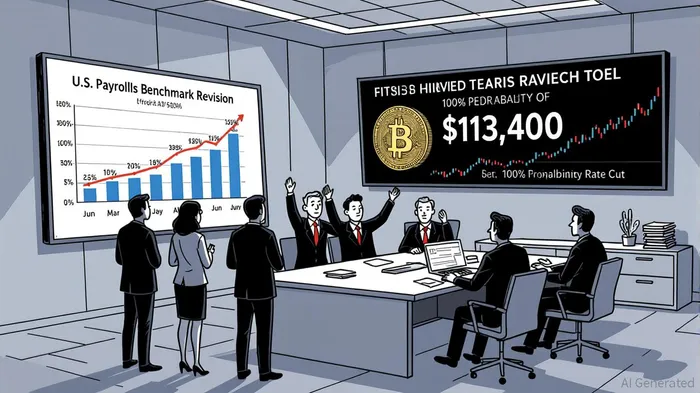

The downward revision has turbocharged expectations for rate cuts. As stated by Bloomberg, the CME FedWatch Tool now shows a 100% probability of a 25-basis-point cut in September, with over 75% odds of three or more cuts in 2025[2]. This isn't just market speculation—it's a policy inevitability. The data reinforces the Fed's shift from “higher for longer” to “lower for liquidity,” as weaker labor markets and a rising unemployment rate (4.3% in August) signal a fragile economy[2].

Christopher Waller and Samuel Tombs, two of the Fed's most hawkish voices, have already acknowledged the need for easing, citing the “overstated” nature of prior job gains due to flaws in the birth-death model[2]. With the final benchmark revision due in February 2026, investors can expect a prolonged period of accommodative policy, creating a tailwind for risk-on assets.

Equity Market: A Wait-and-See Game

While the S&P 500 posted a 1.91% gain in August 2025, the rally has been tepid compared to the euphoria of earlier years[2]. The market is pricing in the Fed's rate cuts but remains cautious about the broader economic backdrop. Rate-sensitive sectors like utilities and consumer discretionary are prime beneficiaries of lower borrowing costs, but institutional profit-taking and flat ETF flows are capping momentum[1].

Strategic entry points in equities are emerging for those with a medium-term horizon. As the Fed's easing cycle gains traction, sectors like financials (which benefit from rate cuts) and small-cap stocks (which thrive in liquidity-driven environments) could outperform. However, investors must remain wary of stagflation risks from Trump-era tariffs, which could force the Fed into a painful balancing act[2].

Crypto: A Short-Lived Rally and Long-Term Potential

The cryptocurrency market's reaction was even more volatile. After the August jobs report, BitcoinBTC-- briefly surged to $113,400 before retreating to $111,000, reflecting the sector's sensitivity to liquidity expectations[1]. While a rate cut could inject $1 trillion into global markets, crypto's near-term gains are being capped by institutional profit-taking and regulatory uncertainty[1].

Yet the medium-term outlook is bullish. As noted by Coinedition, the anticipated rate cuts could spark a crypto bull run by boosting liquidity and corporate borrowing[2]. However, long-term risks—such as inflationary pressures from tariffs and a potential jobs recession—remain on the table[2]. For crypto investors, the key is to treat Bitcoin as a speculative bet on the Fed's easing cycle rather than a long-term store of value.

The Bottom Line: Positioning for Policy-Driven Momentum

The -911,000 job revision isn't just a data point—it's a catalyst. The Fed's dovish pivot is now baked into asset prices, creating a fertile ground for risk-on flows. For equities, the fourth quarter offers a strategic window to capitalize on rate cuts, particularly in sectors that thrive on liquidity. For crypto, the path is clouded by short-term volatility but illuminated by long-term potential if the Fed's easing cycle outpaces inflationary headwinds.

As the final benchmark revision looms in February 2026, investors should stay nimble. The labor market's weakness may force the Fed into a more aggressive easing stance, but the real story lies in how markets adapt to a world where “lower for longer” isn't just a policy—it's a necessity.

Comentarios

Aún no hay comentarios