PayPal's Sustainable Edge: How Network Effects and Innovation Fuel Long-Term Shareholder Value

PayPal's Sustainable Edge: How Network Effects and Innovation Fuel Long-Term Shareholder Value

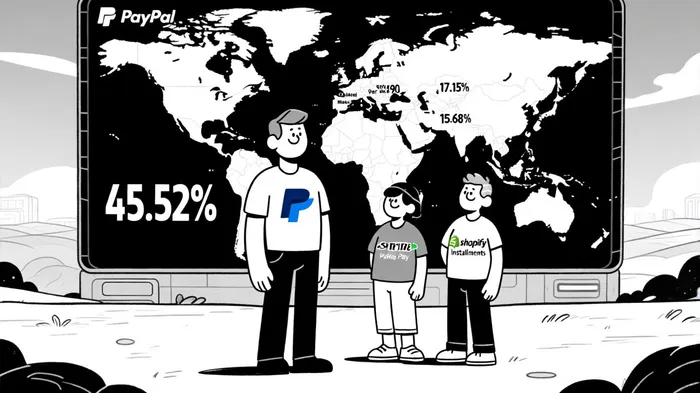

PayPal (PYPL) has long been a cornerstone of the digital payments ecosystem, but its 2025 performance suggests the company is evolving from a market leader to a fortress of sustainable competitive advantages. With 438 million active accounts and a 45.52% global market share in Q3 2025-well ahead of Stripe and Shopify Pay Installments-the fintech giant is leveraging network effects, proprietary technology, and regulatory moats to create long-term shareholder value, even as it faces intensifying competition from tech giants like Apple Pay and Google Pay, according to a Forbes analysis.

Network Effects: The Bedrock of PayPal's Dominance

PayPal's two-sided marketplace-connecting 432 million consumers with merchants-creates a self-reinforcing loop. As more users join, the platform becomes more attractive to merchants, who in turn attract more users. This dynamic is amplified by PayPal's cross-border capabilities, exemplified by its "PayPal World" initiative, which integrates with major digital wallets and payment systems to expand its addressable market, as noted by Forbes. According to a Monexa analysis, PayPal's active account base grew to 438 million in 2024, while Venmo's total payment volume surged 12% year-over-year, its fastest growth in three years. Such metrics underscore the company's ability to monetize its vast user base without relying solely on rapid customer acquisition-a strategic shift emphasized by CEO Alex Chriss in PayPal's 2024 Global Impact Report.

Proprietary Technology: AI-Driven Security and Personalization

PayPal's technological edge lies in its AI-powered fraud detection systems, which process billions of transactions in real time. These systems not only reduce losses but also enhance user trust-a critical differentiator in a sector where security concerns often deter adoption. The company's partnership with Google to integrate AI-driven payment solutions into the latter's ecosystem further cements its innovation moat, enabling personalized user experiences and advanced risk management, as reported by Forbes. Analysts note that PayPal's 46.1% gross margin in 2024 reflects the efficiency of these systems, as lower fraud rates directly boost profitability, according to Monexa.

Regulatory Moats: Trust in a Fragmented Landscape

Operating in 190+ countries, PayPalPYPL-- benefits from a regulatory moat that newer entrants struggle to replicate. Its compliance infrastructure, honed over decades, allows it to navigate complex cross-border regulations with ease. For instance, PayPal's 2024 Global Impact Report highlighted a 79% reduction in operational emissions compared to 2019 levels, aligning with global sustainability trends and reducing regulatory risks, as detailed in PayPal's 2024 Global Impact Report. This legitimacy is particularly valuable in emerging markets, where local compliance hurdles often stymie competitors.

Shareholder Value: Profitability, Buybacks, and a Discounted Valuation

Despite its dominance, PayPal trades at a notable discount to peers. As of September 2025, its forward P/E ratio of 11.89x is significantly lower than those of SoFi and Affirm, suggesting undervaluation relative to growth prospects, per Monexa. The company's capital allocation strategy reinforces this thesis: $6 billion in share repurchases in 2024 and $1.5 billion in Q1 2025 signal confidence in its cash-generating capabilities. With free cash flow surging 60.36% to $6.77 billion in 2024, PayPal has the financial flexibility to reward shareholders while investing in high-margin initiatives like crypto and buy-now-pay-later (BNPL) services, according to Monexa.

Challenges and the Path Forward

PayPal's growth isn't without headwinds. Transaction volume in Q3 2025 declined 7% year-over-year, and analysts project a 16.9% drop in earnings per share for the same period, according to a Nasdaq article. However, these figures mask a strategic pivot: PayPal is prioritizing value over volume. By refining its Braintree service to boost profit margins and focusing on engagement with existing users, the company is positioning itself for more sustainable growth. As stated by Reuters, this approach may mitigate the pressure from Apple Pay and Google Pay, which rely on mobile-first ecosystems to erode PayPal's market share.

Conclusion: A Compelling Long-Term Bet

PayPal's combination of network effects, AI-driven innovation, and regulatory expertise creates a durable competitive advantage. While near-term earnings volatility is a risk, the company's ability to generate robust free cash flow, execute aggressive buybacks, and expand into high-growth segments like BNPL positions it as a compelling long-term investment. For shareholders, the current valuation discount offers an opportunity to capitalize on a business that is not just surviving but redefining the digital payments landscape.

Comentarios

Aún no hay comentarios