Payoneer (PAYO): A Mispriced Fintech Gem in a High-Growth Sector

In the ever-evolving fintech landscape, valuation mispricing often creates opportunities for discerning investors. PayoneerPAYO-- (PAYO), a global leader in cross-border payments, appears to be one such opportunity. Despite robust revenue growth, strong profitability metrics, and strategic expansion into high-margin markets, Payoneer trades at a significant discount to its high-growth fintech peers. This mispricing, rooted in short-term macroeconomic concerns and GAAP accounting quirks, overlooks the company's long-term value proposition.

Revenue Growth and Profitability: A Tale of Two Metrics

Payoneer's Q2 2025 results underscore its ability to scale profitably. Core transaction revenue, excluding interest income, surged 16% year-over-year to $188.6 million, driven by a 7% volume increase and take rate expansion among small and medium-sized businesses (SMBs), according to CompaniesMarketCap. Notably, Average Revenue Per User (ARPU) grew 22% YoY, reflecting a strategic shift toward higher-value customers and products like B2B services, Checkout, and Card. Revenue from B2B SMBs alone jumped 37%, while Merchant Services revenue nearly doubled, per CompaniesMarketCap.

Adjusted EBITDA of $65.2 million in Q1 2025 (implying a ~28.6% margin) further highlights Payoneer's operational efficiency, per MarketBeat. However, GAAP net income declined 29% YoY to $20.6 million, primarily due to cost pressures and swings in financial expenses, a discrepancy visible in CompaniesMarketCap's figures. This discrepancy between adjusted and GAAP metrics has likely contributed to a temporary undervaluation, as investors fixate on short-term volatility rather than sustainable cash flow generation.

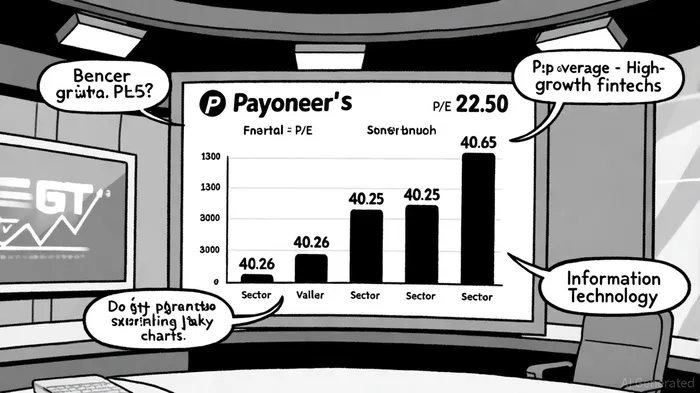

Valuation: A Discount to Industry Averages

Payoneer's current P/E ratio of 22.50, per Fortune Business Insights, stands in stark contrast to the Q2 2025 average P/E of 40.65 for the Information Technology sector (reported by CompaniesMarketCap) and 40.26 for the Software - Application industry (per Fortune Business Insights). Even within the fintech space, where public companies now average 16% EBITDA margins and 69% profitability (CompaniesMarketCap data), Payoneer's valuation appears unloved.

This gap is particularly striking given Payoneer's market fundamentals. At a $2.22 billion market cap (reported by MarketBeat), the company trades at a 44% discount to its historical P/E average, according to FullRatio. For context, high-growth fintechs-often valued on future potential rather than current earnings-are trading at multiples that assume aggressive revenue scaling and margin expansion. Payoneer, meanwhile, is already delivering both.

Strategic Positioning in a Booming Sector

The global fintech industry is on a tear, with revenues growing 21% YoY in 2024 and projected to expand at a 16.2% CAGR through 2032, according to Fortune Business Insights. Payoneer is uniquely positioned to capitalize on this trend. Its recent acquisition of a licensed payment service provider in China, for instance, bolsters its regulatory footprint in a $1.5 trillion market (per CompaniesMarketCap). Meanwhile, AI-driven monetization tools and a focus on B2B cross-border solutions align with macro trends like digital transformation and global e-commerce growth.

Yet, despite these strengths, Payoneer's valuation remains anchored by macroeconomic headwinds. The company suspended full-year 2025 guidance due to uncertainty, a move noted by MarketBeat, a development that has likely dampened investor sentiment. This overreaction, however, ignores the fact that Payoneer's core business is thriving.

Conclusion: A Case for Rebalancing

Payoneer's current valuation reflects a myopic focus on near-term volatility and macroeconomic noise, rather than its long-term growth trajectory. With a P/E ratio that is 44% below its historical average and a revenue growth profile that outpaces many high-growth fintechs, Payoneer offers a compelling risk-rebalance. Investors who look beyond GAAP accounting distortions and recognize the company's strategic momentum may find a rare opportunity in a sector where multiples are typically sky-high.

As the fintech industry continues to mature, companies like Payoneer-those that combine disciplined growth with profitability-will likely outperform. The question is not whether Payoneer can grow, but whether the market will eventually correct its mispricing.

Comentarios

Aún no hay comentarios