Pattern Group's (PTRN) Sudden Share Price Surge and Underlying Valuation Realities

Pattern Group (PTRN), the e-commerce acceleration platform, has captured investor attention with a dramatic share price surge following its September 19, 2025, Nasdaq debut. The stock opened at $14.00 per share and closed its first day up 11%, only to retreat 3.6% in subsequent sessions, valuing the company at $2.38 billion [1]. This volatility raises a critical question: Is the price spike a speculative anomaly, or does it reflect a justified re-rating based on fundamentals?

Fundamental Strength: A Case for Justified Growth

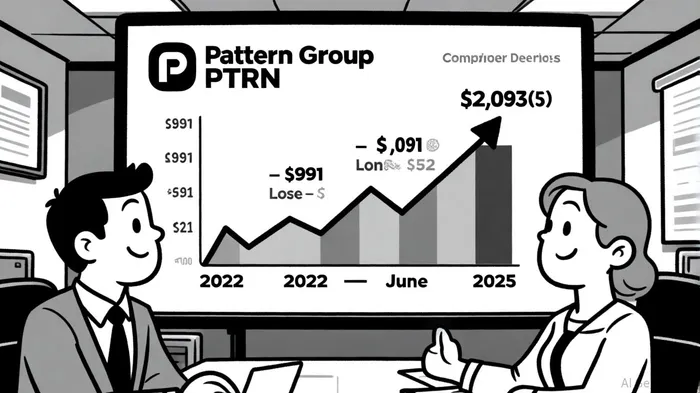

Pattern's financials reveal a company in rapid ascent. From December 2022 to June 2025, revenue surged from $991 million to $2,093 million, while earnings transitioned from a $21 million loss to a $52 million profit [2]. Earnings growth of 67.2% annually far outpaces the 7.8% average for the Specialty Retail industry [3]. The company's net profit margin improved to 2.5% in 2025 from 2.0% in 2024, and its return on equity (ROE) of 18.6% underscores efficient capital utilization [4].

Pattern's business model further strengthens its case. By leveraging AI and machine learning to automate pricing, advertising, and logistics for global brands on marketplaces like AmazonAMZN-- and WalmartWMT--, the company addresses a critical pain point in e-commerce scaling. Its platform, which processes 46 trillion data points, enables brands to grow without large in-house teams—a value proposition that aligns with the sector's shift toward automation [5].

Valuation Realities: A Mixed Picture

The company's valuation multiples suggest a blend of optimism and caution. As of September 2025, Pattern trades at a trailing P/E of 27.43 and an EV/EBITDA of 22.03 [6]. These metrics are in line with the broader Information Technology sector's EV/EBITDA of 27.25 but lower than the 8.1x multiples seen in B2B SaaS companies with recurring revenue [7]. The discrepancy may reflect investor skepticism about Pattern's 2.5% net margin, which, while improved, lags behind the margins of mature SaaS firms.

However, Pattern's growth trajectory justifies a premium. Its 32.5% annual revenue growth and 67.2% earnings growth outpace industry benchmarks, suggesting the market is pricing in future margin expansion. The company's debt-to-equity ratio of 0.6734 and quick ratio of 1.2598 also indicate robust liquidity and solvency, reducing downside risk [8].

Speculation or Re-Rating?

The IPO's mixed performance—strong debut followed by a pullback—hints at both enthusiasm and caution. The 11% opening gain reflects investor confidence in Pattern's disruptive potential, while the 3.6% post-IPO drop may signal profit-taking or concerns about valuation.

Critically, the stock's valuation is not disconnected from fundamentals. Pattern's EV/EBITDA of 22.03 is lower than the IT sector average, suggesting it is undervalued relative to peers. Moreover, its revenue growth and margin improvement indicate a trajectory toward higher profitability, which could justify a re-rating over time.

Risks and Considerations

Investors must weigh several risks. First, Pattern's net margin of 2.5% remains low, and any slowdown in revenue growth could pressure margins. Second, competition in the e-commerce tech space is intensifying, with rivals like ShopifySHOP-- and Amazon's own tools posing threats. Finally, the stock's short-term volatility—exacerbated by its IPO liquidity event—may attract speculative trading, creating noise in the price action.

Conclusion: A Re-Rating Anchored in Fundamentals

Pattern Group's share price surge is not a speculative anomaly but a re-rating driven by its exceptional growth and strategic positioning in the e-commerce sector. While valuation multiples appear elevated relative to some SaaS benchmarks, they are justified by the company's outperformance in revenue and earnings. The recent IPO volatility reflects market dynamics rather than a misalignment with fundamentals. For long-term investors, Pattern's ability to scale its platform and improve margins offers a compelling case for continued growth.

Comentarios

Aún no hay comentarios