PagerDuty’s Q2 Earnings: Navigating Profitability and Growth in a Maturing SaaS Sector

PagerDuty’s Q2 2025 earnings report delivered a mixed bag of signals for investors. Revenue grew 6.4% year-over-year to $123.4 million, aligning with Wall Street’s expectations, while billings rose 3.3% to $113.9 million [1]. The company also raised its full-year Adjusted EPS guidance to $1.02 at the midpoint and reported a non-GAAP profit of $0.30 per share, beating analyst estimates by 49.3% [1]. Yet, the stock plummeted 6.5% to $14.60 post-earnings, raising questions about whether the selloff reflects a mispricing or a justified correction in a slowing SaaS sector.

The Growth-Productivity Juggle

PagerDuty’s customer base grew to 15,322 in Q2, a modest sequential increase of 75 clients [1]. While this suggests resilience, it contrasts with the hypergrowth metrics that once defined the SaaS sector. The broader market is now prioritizing operational efficiency over aggressive expansion, a trend underscored by a 2025 report from RevenueGrid, which notes that SaaS companies are “shifting from hypergrowth to sustainable models” [5]. PagerDuty’s 106% dollar-based net retention rate (NRR) and $494 million in ARR indicate strong customer loyalty, but its 6.4% revenue growth lags behind the double-digit figures seen in earlier years.

The company’s pivot to AI-driven operations, however, offers a compelling differentiator. Its Agentic AI suite—featuring autonomous site reliability engineer agents and scheduling optimization tools—has reduced incident resolution times by 95% for clients like Anaplan [1]. A PagerDutyPD-- survey further highlights market confidence, with 62% of companies expecting over 100% ROI on agentic AI investments [4]. This positions PagerDuty as a leader in the AIOps space, a niche where competitors like DatadogDDOG-- and Splunk are still catching up.

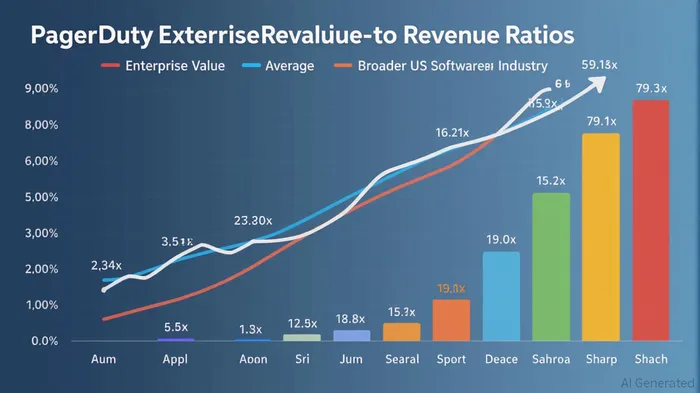

Valuation in a Maturing Sector

Valuation metrics tell a more nuanced story. PagerDuty’s enterprise value-to-revenue ratio of 2.84x is below the SaaS peer average of 4.6x and the US Software industry’s 5.0x [4]. Its forward P/E of 16.78 and price-to-book ratio of 10.20 also suggest undervaluation relative to its fundamentals [5]. However, the company’s EV/EBITDA ratio of -47.1x—a stark contrast to Datadog’s 58.0x and Splunk’s 79.1x—highlights its unprofitability [4][6]. This negative multiple reflects the challenges of scaling AI-driven operations while maintaining margins, a common pain point for SaaS firms in growth phases.

The broader SaaS sector’s valuation compression adds context. As FirstPageSage notes, private SaaS companies with EBITDA ranges of $1–3 million typically command 10.3x multiples, far above PagerDuty’s current level [3]. Yet, PagerDuty’s free cash flow generation and AI-driven differentiation make it an attractive candidate for private equity or strategic buyers, especially as the sector consolidates [1].

Risk-Reward Assessment

For long-term investors, the key question is whether PagerDuty’s valuation now reflects a compelling risk-reward proposition. On the risk side, the company’s 3.3% billings growth and downward guidance revision due to macroeconomic uncertainty signal near-term headwinds [1]. Its EV/EBITDA of -47.1x also raises concerns about path to profitability.

On the reward side, PagerDuty’s AI-driven operations strategy is gaining traction. The 171% expected ROI on agentic AI and strategic partnerships (e.g., MicrosoftMSFT-- Copilot integration) position it to capture market share in a $408.21 billion SaaS sector [1][6]. Its strong NRR and ARR growth above 10% further reinforce its ability to retain high-value clients [2].

The stock’s 6.5% post-earnings drop may thus represent a buying opportunity for investors who believe in the long-term value of AI-driven operations. At current levels, PagerDuty trades at a discount to its peers and the industry, offering exposure to a company that is both a beneficiary of SaaS maturation and a pioneer in AI adoption.

Conclusion

PagerDuty’s Q2 earnings underscore the tension between growth and profitability in a maturing SaaS sector. While its revenue growth has slowed, its AI-driven differentiation and strong customer retention metrics justify optimism. The stock’s near-term volatility, coupled with its undervaluation relative to peers, presents a compelling case for long-term investors willing to bet on its ability to scale profitability without sacrificing innovation.

Source:

[1] PagerDuty (NYSE:PD) Reports Q2 In Line With Expectations [https://finance.yahoo.com/news/pagerduty-nyse-pd-reports-q2-203247626.html]

[2] PagerDuty Announces Second Quarter Fiscal 2025 [https://www.pagerduty.com/newsroom/pagerduty-announces-second-quarter-fiscal-2025-financial-results/]

[3] SaaS Valuation Multiples: 2025 Report [https://firstpagesage.com/business/saas-valuation-multiples/]

[4] PagerDuty (NYSE:PD) Stock Valuation, Peer Comparison [https://simplywall.st/stocks/us/software/nyse-pd/pagerduty/valuation]

[5] SaaS Trends 2025: AI and Data Revolution Reshaping [https://revenuegrid.com/blog/saas-trends-2025-ai-data-future/]

[6] Top 7 SaaS Valuation Multiples to Know in 2025 [https://blog.acquire.com/saas-valuation-multiples/]

Comentarios

Aún no hay comentarios