Oracle's Valuation Risks: A Cautionary Tale Amid Enterprise Software Speculation

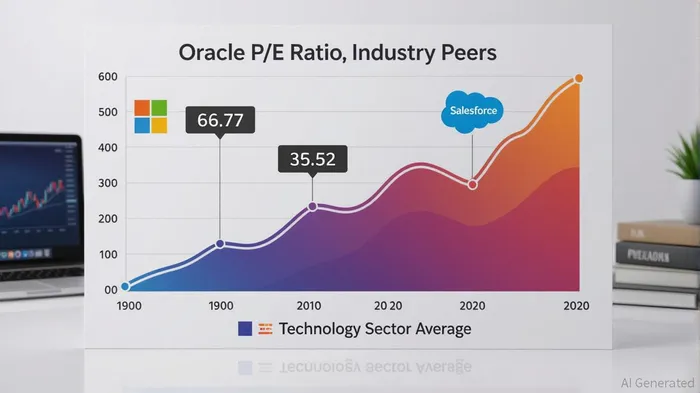

Oracle's recent financial performance has ignited both optimism and caution among investors. The company's Q2 2025 results revealed a 49% year-over-year surge in Remaining Performance Obligations (RPO) to $97 billion, reflecting robust customer commitments[6]. Coupled with earnings per share (EPS) of $1.47—exceeding guidance—Oracle appears to be thriving[1]. However, its valuation metrics tell a more complex story. The trailing twelve months (TTM) P/E ratio now stands at 66.77, far outpacing its 5-year quarterly average of 29.0 and the Technology sector average of 32.17[2]. This disconnect raises a critical question: Is Oracle's stock being driven by fundamentals, or is the market pricing in speculative growth akin to the dot-com bubble?

The Fundamentals: Strength and Contradictions

Oracle's financials are undeniably strong. Fiscal 2025 revenue reached $57.4 billion, with net income of $12.44 billion, reflecting an 8% year-over-year revenue increase and a 19% rise in profitability[5]. Its RPO growth—driven by AI, healthcare, and cloud contracts—signals durable demand for enterprise software. CEO Safra Catz highlighted $48 billion in new sales contracts in Q3 2024, underscoring the company's ability to secure long-term revenue streams[3].

Yet, these fundamentals clash with valuation metrics. Oracle's price-to-book (P/B) ratio of 33.15 as of May 2025 dwarfs the Software industry median of 3, indicating investors are paying a premium for intangible assets like data and AI capabilities[2]. Meanwhile, its intrinsic value is estimated at $203.59, versus a current market price of $293.73—a 31% overvaluation[4]. This gap suggests the market is pricing OracleORCL-- not for its current earnings but for speculative future potential.

Historical Parallels: Dot-Com Lessons

The dot-com bubble (1995–2001) offers a cautionary framework. During that period, the NASDAQ's P/E ratio ballooned to 200, fueled by hype for unprofitable internet startups[1]. Companies like Pets.com and Webvan collapsed when growth expectations failed to materialize. Today's enterprise software sector shares some parallels: high valuations, focus on transformative technologies (e.g., AI), and a concentration of value in a few dominant players. However, there are key differences. Unlike dot-com-era firms, Oracle generates consistent profits and has a 135% year-over-year increase in equity, bolstering its book value[3].

Still, Oracle's P/E ratio of 66.77 rivals the speculative excesses of 2000. For context, Microsoft's P/E is 36.53, and Salesforce's is 35.2[2]. Even during the 2008 financial crisis, when tech stocks faced headwinds, Oracle's peers maintained more grounded valuations due to stronger fundamentals[5]. The current disconnect between Oracle's multiples and its peers suggests systemic overvaluation risks, particularly if AI-driven growth slows or regulatory scrutiny intensifies.

Strategic Exit Points: Mitigating Bubble Risks

For investors, the challenge lies in balancing Oracle's long-term potential with near-term risks. Historical data indicates that overvalued stocks often correct when growth expectations fail to meet reality. Given Oracle's 31% overvaluation relative to intrinsic value[4], a strategic exit could be triggered if:

1. P/E Compression: The TTM P/E drops below 50—a 23% correction from current levels—aligning with its 5-year average[2].

2. RPO Growth Slows: A decline in RPO growth below 30% YoY could signal weakening demand for enterprise software[6].

3. Sector-Wide Correction: A 20% pullback in the Technology sector average P/E would likely pressure Oracle's valuation[5].

Investors should also monitor macroeconomic factors, such as interest rate hikes, which historically dampen speculative valuations. Oracle's exposure to data privacy lawsuits (e.g., its BlueKai platform[1]) adds another layer of risk, potentially impacting revenue streams if regulatory actions escalate.

Conclusion: Proceed with Caution

Oracle's backlog growth and profitability are impressive, but its valuation metrics—particularly the P/E and P/B ratios—suggest a dangerous disconnect from fundamentals. While the company's dominance in enterprise software provides a moat, the current premium reflects speculative optimism rather than proven AI-driven growth. Investors should treat Oracle as a high-conviction holding, with clear exit triggers to mitigate bubble-like risks. As the market grapples with AI hype and regulatory uncertainty, Oracle's stock may yet serve as a bellwether for broader enterprise software valuations.

Comentarios

Aún no hay comentarios