Optimizing Social Security Claiming: Balancing Early Income Needs with Longevity Risks

The decision of when to claim Social Security benefits is one of the most critical financial choices retirees face. Claiming at age 62 offers immediate income but locks in permanently reduced benefits, while delaying until age 70 maximizes monthly payments but forgoes early cash flow. This analysis evaluates the trade-offs between these strategies using the latest life expectancy data, investment return assumptions, and actuarial break-even points to guide retirees toward a data-driven decision.

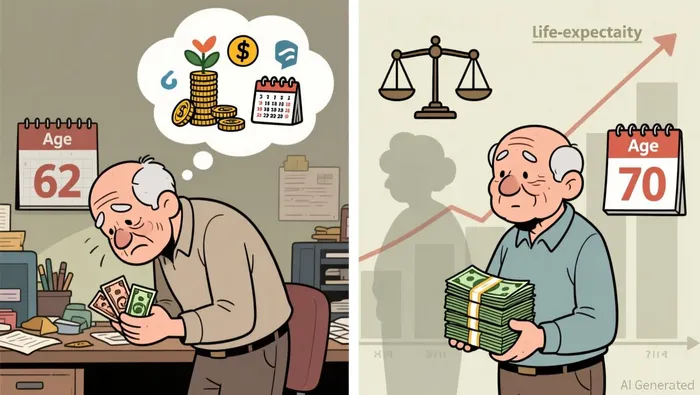

Life Expectancy: A Key Variable in the Decision

Life expectancy statistics are foundational to assessing the long-term value of delayed Social Security benefits. According to the 2025 Social Security Trustees Report, , . By age 67, , and at 70, , respectively according to the same report. These trends highlight the diminishing marginal value of delayed benefits as age increases, as the time horizon for recouping the "wait penalty" shortens.

For context, the CDC reports . This suggests that, on average, most retirees will live long enough to benefit from delayed claiming-provided they can manage early financial needs.

The Actuarial Trade-Off: 8% Annual Increases vs. Investment Returns

Social Security offers a . This effectively creates a "forced savings" mechanism, with the government acting as the insurer of longevity risk. However, this rate must be compared to alternative investment returns.

Over the past five years, . On the surface, this matches the 8% Social Security increase. However, according to , according to the same analysis. These figures suggest that, for retirees with access to equity-heavy portfolios, the actuarial gain from delayed claiming is marginally competitive. For those reliant on bonds or low-risk assets, the 8% Social Security increase becomes significantly more attractive.

Over the past five years, . On the surface, this matches the 8% Social Security increase. However, according to , according to the same analysis. These figures suggest that, for retirees with access to equity-heavy portfolios, the actuarial gain from delayed claiming is marginally competitive. For those reliant on bonds or low-risk assets, the 8% Social Security increase becomes significantly more attractive.

Break-Even Analysis: When Does Delayed Claiming Pay Off?

A critical tool for retirees is the break-even age calculation. For example, . This means living past 78 yields higher lifetime benefits by delaying. Given the CDC's life expectancy at 65, , most retirees are likely to surpass the break-even threshold.

However, this analysis assumes no investment growth on early benefits. , according to . This underscores the importance of asset allocation in the claiming decision.

Balancing Income Needs and Longevity Risk

The optimal claiming strategy depends on three factors:

1. Health and Family Longevity: Retirees with a family history of long life or access to quality healthcare may prioritize delaying benefits.

2. Financial Needs: Those requiring immediate income to cover expenses or pay off debt may need to claim early, though strategies like partial retirement or part-time work can mitigate this.

3. Investment Capacity: Retirees with high-risk tolerance and access to equity-heavy portfolios may outperform the 8% Social Security increase, making early claiming more viable.

For example, . Conversely, those with limited savings may face a liquidity crunch if they delay claiming.

Data-Driven Strategy: A Framework for Decision-Making

- Assess Life Expectancy: Use personalized health metrics and family history to estimate survival probabilities. If exceeding the break-even age is likely, delay claiming.

- Model Investment Scenarios: Calculate the real returns of your portfolio. If they exceed 8%, early claiming may be justified; otherwise, delay.

- Leverage COLA Adjustmentsaccording to financial data provide inflation protection, making delayed benefits more valuable in a high-inflation environment.

- Consider Spousal Needs: For married couples, coordinating claiming strategies (e.g., one spouse claiming early while the other delays) can optimize household income.

Conclusion

The Social Security claiming decision is a nuanced interplay of longevity, investment returns, and financial needs. While the 8% annual increase from delayed claiming is compelling, it is not universally optimal. Retirees must weigh their unique circumstances against actuarial data and investment capabilities. For most, delaying until at least 70 remains the statistically sound choice, but exceptions exist for those with strong investment returns or urgent liquidity needs. By grounding decisions in data, retirees can maximize their long-term financial security.

Comentarios

Aún no hay comentarios