Can Operational Efficiency Sustain Shake Shack's EBITDA Momentum?

Shake Shack Inc.’s SHAK recent performance highlights how operational efficiency is becoming a key driver of its profitability and EBITDA growth. In 2025, the company reported revenue growth of 15.4% to $1.45 billion, while adjusted EBITDA increased about 19.5% year over year to roughly $210 million. Management attributed this improvement largely to disciplined operational execution and margin-enhancing initiatives across the business.

A key factor behind the improvement has been the company’s revamped labor model. Rather than cutting staff, Shake ShackSHAK-- focused on optimizing workforce deployment to ensure the right staffing levels during peak hours. This strategy significantly improved productivity, with more than 90% of restaurants meeting labor targets in 2025 compared with about 50% in mid-2024. Better scheduling and reduced overtime helped lower labor costs as a percentage of sales while maintaining service quality.

Operational improvements have also enhanced restaurant productivity. Average wait times declined from roughly seven minutes in 2023 to under six minutes in 2025, while employee tenure increased nearly 40%, indicating stronger team stability and improved in-store execution.

Supply-chain optimization further supported profitability. Shake Shack expanded its supplier base, improved logistics networks and conducted extensive sourcing reviews to mitigate commodity inflation, including mid-teen beef price increases in the second half of 2025. These efforts helped protect margins despite industry cost pressures.

Looking ahead, management expects continued operational discipline to support earnings growth. For 2026, the company anticipates adjusted EBITDA growth in the low-to-high teens range, supported by modest pricing, supply-chain savings and improved restaurant operations. Over the longer term, Shake Shack reiterated its 2027 outlook for EBITDA growth in the low-to-high teens annually, alongside ongoing restaurant-level margin expansion.

If Shake Shack continues executing on labor optimization, supply-chain efficiencies and operational improvements, these initiatives could help sustain its EBITDA momentum through 2026 and into 2027.

How Do Competitors Compare in Driving Profitability?

Shake Shack’s operational efficiency push mirrors strategies used by key fast-casual peers such as Chipotle Mexican Grill CMG and Restaurant Brands International QSR.

Chipotle has built a strong margin profile by improving operational throughput and expanding digital capabilities. Initiatives such as streamlined kitchen workflows, mobile ordering and the Chipotlane drive-thru format allow the company to handle higher order volumes with improved labor productivity. These efforts have supported consistent restaurant-level margin expansion and strong EBITDA growth, demonstrating how operational discipline can translate into sustained profitability.

Restaurant Brands, the parent of Burger King and other global chains, has also prioritized operational improvements. Through its “Reclaim the Flame” turnaround strategy, the company is investing in restaurant modernization, technology upgrades and supply-chain efficiencies to enhance franchisee economics and systemwide profitability.

Against this competitive backdrop, Shake Shack is pursuing similar efficiency gains through labor optimization, supply-chain diversification and improved restaurant execution to sustain its EBITDA momentum.

SHAK’s Price Performance, Valuation and Estimates

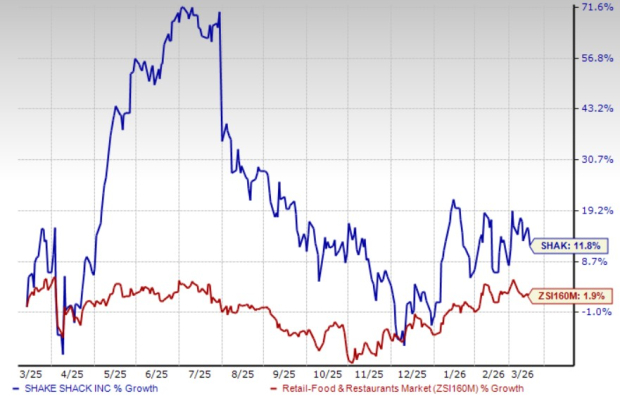

Shake Shack’s shares have gained 11.8% in the past year compared with the industry’s 1.9% increase.

Price Performance

Image Source: Zacks Investment Research

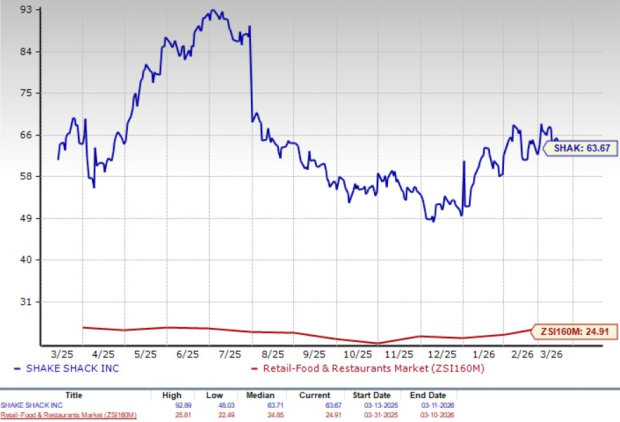

In terms of its forward 12-month price-to-earnings ratio, SHAKSHAK-- is trading at 63.67, up from the industry’s 24.91.

P/E (F12M)

Image Source: Zacks Investment Research

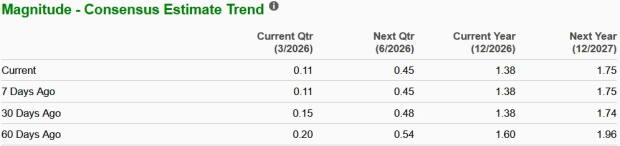

Over the past 60 days, the Zacks Consensus Estimate for SHAK’s 2026 earnings per share has decreased, as shown in the chart.

Image Source: Zacks Investment Research

SHAK currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chipotle Mexican Grill, Inc. (CMG): Free Stock Analysis Report

Restaurant Brands International Inc. (QSR): Free Stock Analysis Report

Shake Shack, Inc. (SHAK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios