OPEC+'s Limited Supply Risk in 2025: Why Oil Investors Should Stay Bullish

The oil market's fixation on OPEC+'s production plans often overlooks the real-world constraints that limit the cartel's ability to flood global markets. While the alliance has signaled a modest output increase of 137,000 barrels per day (b/d) in October 2025, a closer examination of its spare capacity, compliance challenges, and geopolitical hurdles reveals a far more nuanced—and bullish—picture for oil investors.

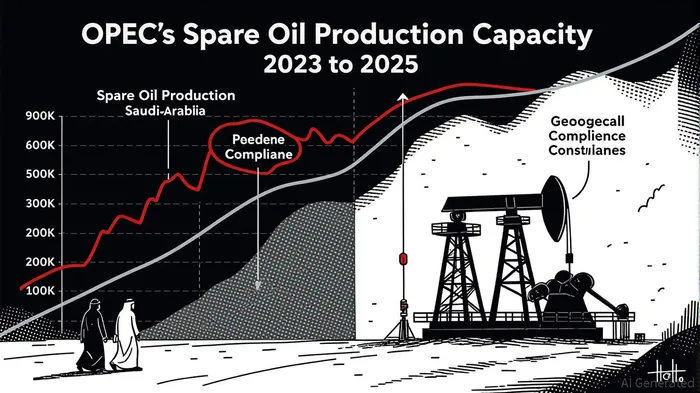

Spare Capacity: A Double-Edged Sword

OPEC+'s spare production capacity remains a critical buffer, but its distribution and sustainability are far from uniform. As of July 2025, the group held 4.61 million bpd of spare capacity, with Saudi Arabia accounting for 2.59 million bpd—nearly 56% of the total. This dominance allows Riyadh to act as a swing producer, but it also exposes the alliance's fragility. For instance, Saudi Arabia's own capacity is expected to shrink as it fulfills its share of the 1.66 million bpd production increase planned for the next year. Analysts warn that continued output hikes could push spare capacity below historical averages by late 2025, reducing OPEC+'s ability to respond to sudden demand shocks.

Meanwhile, other members face structural limitations. Russia, for example, is constrained by Western sanctions and aging infrastructure, leaving it unable to contribute meaningfully to the production increase. Iraq and Nigeria, meanwhile, grapple with internal instability and technical bottlenecks. These constraints mean that OPEC+'s headline spare capacity is less of a guarantee than a theoretical maximum.

Compliance: A Persistent Achilles' Heel

OPEC+'s ability to enforce production quotas has been a persistent weakness. In Q1 2025, the group's compliance rate averaged 67%, with Iraq, Kazakhstan, and Russia lagging at 54%, 61%, and 65%, respectively. This underperformance is compounded by a flawed compensation mechanism: only 37% of pledged cuts materialized in Q1 2025, undermining the group's credibility.

The situation is further complicated by the fact that many members are now producing above their quotas. For example, Iraq and Russia have consistently exceeded their targets, while Saudi Arabia and the UAE have maintained high output levels to secure market share. This overproduction, coupled with the difficulty of enforcing compensatory cuts, suggests that OPEC+'s ability to rapidly scale up supply is limited by internal discord and operational inertia.

Geopolitical Hurdles: Unpredictable but Pivotal

Geopolitical risks remain a wildcard for OPEC+'s supply strategy. Russia's production is already below its targets due to export constraints and sanctions, while U.S.-Russia tensions and potential new sanctions on Russian oil exports add further uncertainty. Meanwhile, U.S. President Donald Trump's rhetoric on additional sanctions has fueled market speculation about tighter global oil balances.

These dynamics are not one-sided. The Russia-Ukraine conflict and U.S. trade policies have kept oil prices supported despite OPEC+'s output increases. For investors, this means that geopolitical frictions—rather than OPEC+'s production decisions—may ultimately dictate market outcomes.

A Bullish Case for Oil Investors

For oil investors, the combination of eroding spare capacity, weak compliance, and geopolitical volatility creates a compelling bullish case. OPEC+'s production increases, while headline-grabbing, are unlikely to translate into a meaningful oversupply. The group's ability to unwind its cuts is hampered by technical, political, and financial constraints, ensuring that global oil markets remain in a state of delicate balance.

Moreover, the looming 2026 oil glut—projected to materialize as non-OPEC+ supply rises—will likely force OPEC+ to prioritize market share over price stability, further limiting its ability to flood the market. This strategic shift, coupled with the IEA's forecast of slowing demand growth (1.2 million bpd in 2025 vs. 1.8 million in 2024), suggests that oil prices will remain resilient.

In short, the market's fear of an OPEC+-driven oversupply is overblown. For investors, this mispricing presents an opportunity to capitalize on a sector where supply-side constraints and geopolitical risks continue to outweigh the headline production numbers.

Comentarios

Aún no hay comentarios