Olin Corporation's Operational Transformation: Navigating Challenges to Drive Shareholder Value

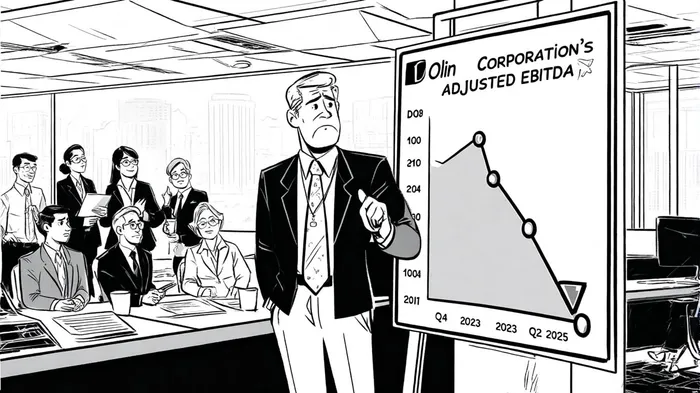

Olin Corporation's operational transformation, initiated in late 2023, has been a focal point for investors seeking to understand how the industrial conglomerate balances strategic reinvention with financial stability. While the company's efforts to restructure its Chlor Alkali Products and Vinyls segment under the "value accelerator initiative" showed early promise—evidenced by a $52.9 million net income and $210.1 million adjusted EBITDA in Q4 2023—its financial performance has since deteriorated, raising questions about the long-term viability of its strategy[3]. By Q1 2025, net income had plummeted to $1.4 million, or $0.01 per diluted share, with adjusted EBITDA declining to $185.6 million, a 23% drop year-over-year[2]. This volatility underscores the challenges of executing a complex operational overhaul in a sector marked by fluctuating commodity prices and rising input costs.

Strategic Shifts and Operational Realignment

A pivotal element of Olin's transformation has been its repositioning in the vinyls value chain. In late 2025, the company announced its exit from the Blue WaterBLUW-- Alliance joint venture with Mitsui & Co., Ltd., opting instead to focus on Ethylene Dichloride (EDC) production to reduce exposure to volatile spot markets[1]. This move, while aimed at enhancing long-term profitability, has coincided with a decline in segment earnings. For instance, the Chlor Alkali Products and Vinyls segment reported earnings of $64.9 million in Q2 2025, down from $99.3 million in the prior year, due to lower pricing and higher operating costs[2]. Such outcomes highlight the trade-offs inherent in strategic realignment: short-term pain for potential long-term gains.

Simultaneously, OlinOLN-- has invested in digital transformation to bolster operational efficiency. Acquisitions of tools like the Bubble Platform for app development and OracleORCL-- PeopleSoft HCM for HR functions[3] align with broader goals to streamline workflows and reduce costs. These initiatives, however, remain unproven in their ability to offset rising expenses. For example, the Epoxy segment incurred a $23.7 million loss in Q2 2025, driven by elevated operating costs and maintenance expenses[2], suggesting that digital tools alone may not be sufficient to counter external pressures.

Shareholder Value and Capital Allocation

Olin's capital allocation strategyMSTR-- has been a mixed bag for shareholders. The company has aggressively repurchased shares, spending $10.1 million to buy back 0.5 million shares in Q2 2025[2], and maintaining a $1.978 billion repurchase program. This contrasts with its liquidity position, which includes a robust $1.4 billion in available liquidity and a $223.8 million cash balance as of Q2 2025[2]. Yet, concerns persist over its $3.035 billion long-term debt load[2], which could constrain flexibility during periods of economic uncertainty.

The company's focus on cash generation—$212.3 million in operational cash flow in Q2 2025[2]—has enabled debt reduction and strategic acquisitions, but investors must weigh these against declining margins. For instance, the Winchester segment's earnings fell to $25.0 million in Q2 2025 from $70.3 million in the prior year, attributed to weaker commercial ammunition sales and raw material costs[2]. Such trends suggest that Olin's capital allocation may need to prioritize segments with higher growth potential.

Sustainability and Long-Term Resilience

Olin's sustainability initiatives, including carbon emission reductions and water conservation efforts[2], align with global ESG trends and could enhance its competitive positioning. However, these programs often require upfront investment, which may exacerbate short-term financial pressures. The company's ability to balance sustainability goals with profitability will be critical in maintaining stakeholder confidence.

Outlook and Risks

Looking ahead, Olin's leadership projects adjusted EBITDA between $170 million and $210 million for Q3 2025[2], a range that reflects ongoing uncertainty. While the company's strong liquidity and disciplined capital allocation provide a buffer, risks such as commodity price volatility, inflationary pressures, and execution risks in its vinyls strategy could hinder progress. Investors should monitor key metrics, including segment profitability trends and debt-to-EBITDA ratios, to assess whether the transformation is delivering on its promises.

In conclusion, Olin's operational transformation represents a bold but precarious attempt to future-proof its business. While early initiatives showed promise, the mixed financial results and segment-specific challenges underscore the need for continued strategic agility. For shareholders, the path to value creation will depend on Olin's ability to execute its vinyls strategy, optimize digital tools, and navigate macroeconomic headwinds without compromising long-term resilience.

Comentarios

Aún no hay comentarios