OECD Hikes U.S. Growth Outlook, But Warns On 2026 Because of This Troubling Trend

The OECD's latest economic outlook for the United States presents a paradox: a modest upward revision to 2025 growth projections, yet a stark warning about the fragility of the 2026 outlook. While the organization now forecasts U.S. GDP growth at 1.8% for 2025—up from 1.6% in earlier estimates—the trajectory for 2026 remains troubling, with growth projected to dip to 1.5% [1]. This slowdown is driven by a confluence of macroeconomic imbalances, including a surge in trade barriers, policy uncertainty, and demographic headwinds. For investors, the OECD's analysis underscores a critical risk: the U.S. economy is teetering on the edge of a self-reinforcing cycle of inflation, reduced investment, and labor market strain.

The Tariff Tsunami: A Supply Chain Crisis in the Making

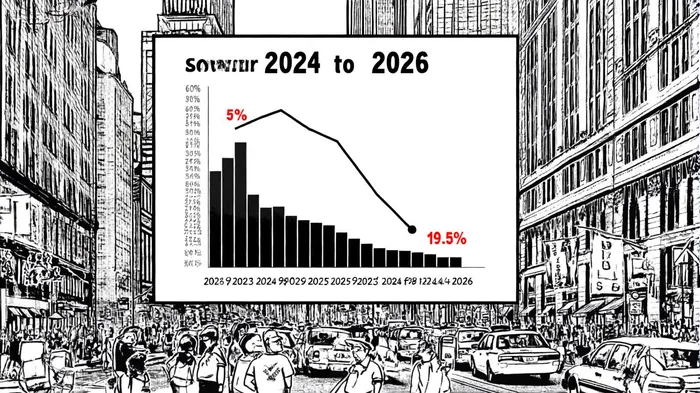

The most immediate threat to U.S. growth stems from the rapid escalation of trade barriers. By the end of August 2025, the effective tariff rate on imports had surged to 19.5%, the highest level since 1933 [2]. This spike, driven by “reciprocal” tariffs on Chinese goods and retaliatory measures from trade partners, is already disrupting global value chains. According to a report by the OECD, these tariffs are not merely distorting trade—they are eroding the foundations of U.S. economic resilience.

The impact is multifaceted. Higher tariffs have inflated import prices, squeezing consumer real incomes and forcing businesses to absorb costs through reduced workforce sizes [3]. For instance, the manufacturing sector, which relies heavily on cross-border supply chains, faces a 30% tariff hike on Chinese inputs, directly threatening profit margins. Meanwhile, the energy sector is grappling with volatile global markets, as trade tensions exacerbate geopolitical risks [4].

Policy Uncertainty: The Invisible Tax on Investment

Beyond tariffs, the OECD highlights a surge in economic policy uncertainty as a drag on growth. This uncertainty, fueled by shifting government priorities and the looming 2026 election cycle, has dampened business and consumer confidence. A recent Federal Reserve survey identified trade policy changes as the most frequently cited risk to financial stability, with 50% of respondents flagging policy uncertainty as a top concern [5].

The ripple effects are evident in capital markets. Sectors like financials, energy, and basic materials—identified in academic studies as particularly sensitive to geopolitical risk—are experiencing a 1–2% decline in aggregate investment [6]. For example, the financial sector's exposure to trade-dependent industries has led to a 15% drop in M&A activity year-to-date, as firms delay decisions amid regulatory ambiguity.

Immigration and Labor Market Strain: A Long-Term Headwind

The OECD also points to a sharp decline in net immigration as a structural drag on growth. With net immigration falling by 40% in 2025 compared to 2024, labor shortages are intensifying in sectors like healthcare, construction, and agriculture. This trend is compounding the effects of aging demographics, pushing up wage growth and inflation. The OECD warns that without policy adjustments, the U.S. labor market could contract by 0.5% in 2026, further stifling productivity [7].

Sector-Specific Risks: Where to Watch

For investors, the OECD's analysis highlights three key areas of vulnerability:

1. Manufacturing: Tariff-driven supply chain disruptions are expected to reduce sectoral output by 3–5% in 2026. Companies reliant on imported components, such as automotive and electronics firms, face margin compression.

2. Financials: Heightened policy uncertainty and trade tensions could trigger a 10–15% correction in banking stocks, as credit risk and regulatory costs rise.

3. Energy: Geopolitical volatility and inflationary pressures are likely to widen price swings, with oil and gas producers facing both opportunities and operational risks.

Conclusion: A Delicate Balancing Act

The OECD's revised growth forecast for the U.S. reflects a fragile equilibrium. While near-term resilience persists, the risks of a 2026 slowdown are acute and multifaceted. Investors must navigate a landscape where tariffs, policy uncertainty, and demographic shifts converge to create a perfect storm of macroeconomic imbalances. As the OECD emphasizes, resolving trade tensions and stabilizing immigration policy will be critical to restoring long-term growth. Until then, the U.S. economy remains a high-risk, high-reward proposition.

Comentarios

Aún no hay comentarios