NVIDIA's Ecosystem-Driven Dominance: A Strategic Investor's Guide to AI and Semiconductor Supremacy

In 2025, NVIDIANVDA-- has cemented its position as the uncontested leader in the AI and semiconductor industries, driven by an ecosystem-driven business model that combines cutting-edge hardware, proprietary software, and strategic partnerships. For investors, the company's recurring revenue streams, network effects, and defensible moats present a compelling case for long-term value creation, even amid geopolitical headwinds and competitive pressures.

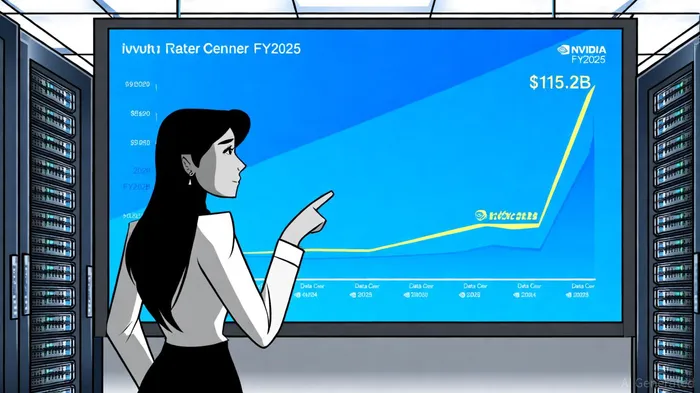

Financial Performance: A Data Center-Driven Powerhouse

NVIDIA's Q2 2025 results underscore its meteoric rise. The company reported $46.7 billion in revenue, surpassing Wall Street's $46.05 billion estimate and marking a 6% sequential increase and 56% year-over-year surge[1]. The Data Center segment alone accounted for $41.1 billion (88% of total revenue), fueled by demand for AI training and inference workloads[1]. This segment's dominance is not a short-term anomaly: in fiscal year 2025 (FY2025), NVIDIA's Data Center revenue reached $115.2 billion, representing 88% of total revenue and a 142% YoY growth[2].

The Blackwell GPU architecture, with its 17% sequential revenue growth, has become a linchpin for hyperscalers like Amazon, Google, and Meta, while strategic partnerships with European nations (France, Germany, etc.) are expanding its industrial AI cloud footprint[2]. Despite zero H20 chip shipments to China due to U.S. export controls, NVIDIA's ability to clear $180 million in reserved inventory to non-Chinese clients and maintain 72.7% non-GAAP gross margins highlights its pricing power and operational resilience[1].

Ecosystem Lock-In: CUDA, Software, and Developer Network Effects

NVIDIA's competitive advantage lies in its CUDA platform, which has become the de facto standard for AI development. Over 90% of AI developers rely on CUDA, creating a formidable switching cost that locks in both individual developers and enterprises[2]. This ecosystem is further reinforced by tools like NVIDIA AI Enterprise (adopted by 75% of Fortune 500 companies) and Omniverse, which streamline AI deployment and industrial design[2].

The company's recurring revenue model is amplified by enterprise contracts and subscription-based software. For instance, NVIDIA AI Enterprise improves developer productivity by 30% on average, incentivizing long-term client retention[2]. Meanwhile, strategic investments in AI startups (e.g., OpenAI, Mistral AI) and partnerships with drug discovery firms like Novo Nordisk diversify revenue streams beyond traditional chip sales[2].

Competitive Landscape: AMD and Intel in the Rearview Mirror

While AMD and Intel remain relevant, NVIDIA's 80–85% projected AI chip market share in 2025–2026 dwarfs their efforts[3]. AMD's MI300X chips, though competitive in inference tasks, lack the full-stack integration and software ecosystem that define NVIDIA's offerings. Analysts note that NVIDIA's 74.2% gross margin in 2025 far exceeds AMD's 51%, underscoring its premium positioning in high-margin training workloads[3].

Intel's recent $5 billion partnership with NVIDIA to develop x86 CPUs with NVLink connectivity illustrates the latter's gravitational pull in the industry[3]. By embedding its technology into Intel's CPU roadmap, NVIDIA is extending its influence into hybrid computing architectures, further entrenching its ecosystem.

Investor Positioning: Shareholder Returns and Long-Term Confidence

NVIDIA's financial strength has enabled aggressive shareholder returns. In H1 2026 alone, the company returned $24.3 billion to shareholders and approved an additional $60 billion in share repurchases[2]. This capital allocation strategy, combined with a $8.68 billion R&D investment in FY2024, signals a balance between rewarding investors and fueling innovation[2].

Institutional investors remain bullish, with Bank of America analyst Vivek Arya highlighting NVIDIA's Blackwell AI chip, CUDA dominance, and global partnerships as “key differentiators”[3]. Despite risks like U.S.-China tensions, NVIDIA's pivot to lower-performance variants (e.g., H20) and expansion into robotics and automotive markets mitigate exposure[4].

Conclusion: A Defensible Moat in the AI Era

NVIDIA's ecosystem-driven growth model—combining hardware innovation, software lock-in, and strategic partnerships—positions it as a must-own asset for investors. With $54 billion in guided Q3 2025 revenue and a $130.5 billion FY2025 revenue milestone, the company is not just capitalizing on AI's rise but actively shaping its trajectory[1]. For those seeking exposure to the AI revolution, NVIDIA's recurring revenue streams and 85% market share projection make it the cornerstone of a forward-looking portfolio.

Comentarios

Aún no hay comentarios