Nvidia's Dominance in AI and Data Center Markets: A Deep Dive into Sustainable Margins, Market Share, and Valuation Rationale

Nvidia's ascent in the AI and data center markets has redefined the semiconductor industry, driven by a combination of technological innovation, strategic ecosystem development, and financial discipline. As of Q3 2025, the company reported $35.1 billion in revenue, a 94% year-over-year increase, with the Data Center segment alone contributing $30.8 billion-a 112% year-over-year surge, according to NVIDIA's Q3 2025 earnings report. This performance underscores a structural shift in global demand for AI infrastructure, where Nvidia's dominance is both a product of and a catalyst for industry trends.

Sustainable Margins: A Testament to Operational Excellence

Nvidia's financial metrics reveal a company scaling efficiently while maintaining exceptional profitability. In Q3 2025, gross profit margins reached 74.6%, operating margins hit 62.4%, and net margins stood at 55.0%, figures that are reported in NVIDIA's Q3 2025 earnings report. These figures represent a dramatic improvement from FY2023, when gross margins were 56.93% and net margins at 16.19%, according to Stock Analysis On's profitability page. The company's ability to sustain these margins, even as it scales rapidly, is attributed to its vertically integrated approach-combining cutting-edge hardware (e.g., Hopper and Blackwell GPUs) with proprietary software (CUDA) and enterprise AI solutions, as detailed in a Mordor Intelligence report.

Analysts project slight margin moderation in Q4 2025, with gross margins expected to dip to 73%–73.5%, per the same NVIDIANVDA-- Q3 2025 filing. However, this remains well above the semiconductor industry average of 64.9% in 2022 and 75.0% in 2025, a gap highlighted by Invrix, suggesting Nvidia's pricing power and ecosystem lock-in are robust.

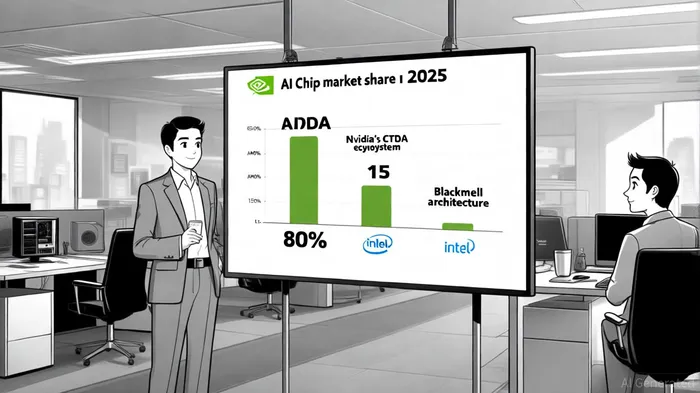

Expanding Market Share: A Moat Built on AI and Ecosystem Leadership

Nvidia commands approximately 80% of the AI chip market in 2025, a position fortified by its CUDA software ecosystem and the Blackwell architecture, which delivers unparalleled performance-per-watt for AI training and inference (Mordor Intelligence). Competitors like AMD and Intel are closing the gap but face structural challenges. AMD's MI300X GPU, with 192GB of memory, targets cost-sensitive data centers, while Intel's Gaudi processors and Intel Foundry Services aim to diversify its AI offerings. However, Nvidia's end-to-end solutions-spanning hardware, networking (e.g., BlueField DPU), and AI software stacks-create a competitive moat that rivals struggle to replicate (Mordor Intelligence).

Industry trends further cement Nvidia's leadership. Hyperscale data centers, which accounted for 34.4% of the AI data center market in 2024, are increasingly adopting Nvidia's GPUs to power generative AI models, according to a Grand View Research report. Meanwhile, edge computing and energy-efficient infrastructure (e.g., liquid cooling) are expanding, aligning with Nvidia's roadmap for Blackwell and future architectures (Mordor Intelligence). North America, particularly the U.S., remains the epicenter of this growth, contributing 36.6% of global AI data center demand in 2024 (Grand View Research report).

Valuation Rationale: Justifying the Premium

Nvidia's valuation metrics reflect high expectations for future growth. As of Q3 2025, the company trades at a trailing P/E of 50x and a forward P/E of 33x, with an enterprise value to sales ratio of 27.5x, data summarized on the StockAnalysis statistics. While these multiples appear elevated, they are supported by its $12.9 billion annualized R&D investment-a nearly 2x edge over AMD's $6.37 billion, a gap highlighted by Invrix. This spending fuels innovation in AI-specific chips (e.g., GB200, B100) and ensures Nvidia stays ahead of rivals in performance and efficiency (StockAnalysis).

Comparisons with peers highlight Nvidia's premium. AMD, with a forward P/E of 33.14x and EV/Revenue of 9.24x, is valued more favorably on sales but lags in AI-focused R&D and ecosystem integration (Stock Analysis On). Intel, despite $16 billion in 2023 R&D spending, remains a distant third in market capitalization and AI innovation (Invrix). Analysts project continued outperformance for Nvidia, with consensus EPS of $3.51 for FY2025 and a forward P/E of 33x (StockAnalysis), reflecting confidence in its ability to monetize AI's secular growth.

Conclusion: A Compelling Case for Long-Term Investment

Nvidia's dominance in AI and data centers is underpinned by sustainable margins, a widening market share, and a valuation that balances premium pricing with growth potential. While AMD and Intel pose credible threats, Nvidia's ecosystem, R&D scale, and alignment with industry trends (e.g., hyperscale computing, edge AI) position it as the de facto infrastructure provider for the AI era. For investors, the company's financial discipline and innovation pipeline justify its current valuation, making it a cornerstone holding in portfolios targeting the next decade of technological disruption.

However, historical data from 2022 to the present reveals that NVDANVDA-- shares have underperformed the market in the 30 days following earnings releases, with an average excess return of -0.79% compared to the benchmark's +8.44%. This pattern, which becomes statistically significant from day 3 onward, suggests a potential "buy-the-rumor, sell-the-news" dynamic that investors may want to consider when timing their positions, as shown by an internal event-study analysis of NVDA earnings releases (2022–2025).

Comentarios

Aún no hay comentarios