Nvidia's $4 Trillion Milestone: A Catalyst for AI Supremacy and Geopolitical Realignment in Tech

Nvidia's historic $4 trillion market cap milestone, achieved in July 2025, marks a turning point in the tech landscape. The company's dominance in AI chips has not only redefined valuation metrics for the sector but also ignited a geopolitical scramble for control over the strategic materials powering this revolution. For investors, this milestone is both an opportunity and a warning: the AI era is irreversible, but its trajectory hinges on supply chain resilience, trade policies, and monetary conditions. Let's dissect the implications.

AI's Ascendancy: Nvidia's Chip Superiority

Nvidia's valuation surge is rooted in its AI chip leadership. Its Blackwell chips, 40 times more powerful than the prior Hopper architecture, are the gold standard for training large language models (LLMs) and generative AI systems. These chips, paired with its CUDA software platform, have become indispensable for data centers and enterprises racing to adopt AI.

The company's fiscal 2026 first-quarter revenue jumped 69% year-over-year, underscoring the insatiable demand for its hardware. Yet this growth comes with risks: U.S. export restrictions on advanced chips like the H20 have cost NvidiaNVDA-- $8 billion in lost sales to China.

This chart illustrates how AI's ascendance has created a clear divide between chipmakers. Nvidia's lead is widening, but geopolitical headwinds loom.

Geopolitical Realignment: The Rare Earths War

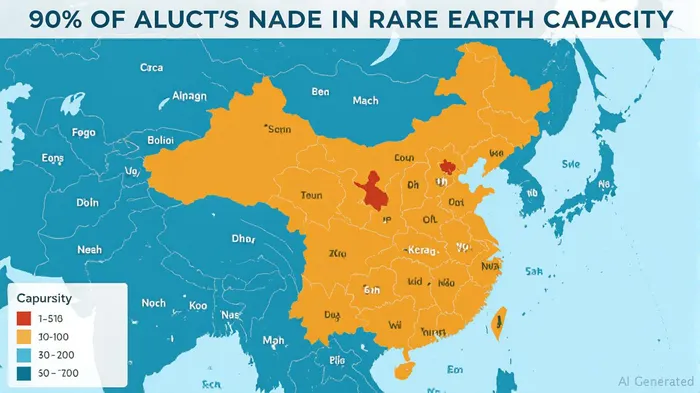

Nvidia's success highlights a broader struggle: the global competition for rare earth elements (REEs) and critical minerals. China's December 2024 export ban on gallium, germanium, and other materials has exposed the U.S.'s reliance on Chinese supply chains. These elements are not just “rare”—they're existential for AI chips.

- Gallium: Vital for gallium arsenide semiconductors in high-speed AI processors.

- Germanium: Used in photonics for advanced chip interconnects.

- Neodymium: Powers magnets in cooling systems for data centers.

The U.S. response has been aggressive. MP Materials' Texas magnet plant and General Motors' rare earth partnerships aim to reduce dependency. Yet progress is slow: the U.S. still sources 72% of its rare earths from China. The Defense Department's $439 million investment to secure supply chains underscores the urgency—F-35 fighters and submarines rely on these materials.

Supply Chain Vulnerabilities: The Hidden Risks

The rare earth bottleneck is not just an economic issue—it's a national security crisis. A complete gallium/germanium shortage could cost the U.S. $3.4 billion in GDP losses annually. Meanwhile, the EV industry faces its own crunch: each electric vehicle requires 136 pounds of graphite, and the U.S.'s only nickel mine is set to deplete by 2028.

Investors should note two critical data points:

1. China controls 60% of global rare earth mining and 90% of refining capacity (as of 2025).

2. The U.S. rare earth processing capacity is just 10% of China's, with projects like Victory Metals' North Stanmore mine in Australia still years from full production.

This gap presents both a risk and an opportunity. Companies like MP MaterialsMP-- (MP) and Talon Metals (TAL) are positioned to profit if supply diversification accelerates.

Federal Reserve Rates: A Double-Edged Sword

The Fed's July 2025 decision to hold rates at 4.25-4.50% is a mixed blessing for tech investors. While no immediate cuts were announced, markets anticipate two rate reductions by year-end and two more in 2026. Lower rates will:

- Boost valuations: Tech's high-growth, low-cash-flow models benefit from discounted cash flow (DCF) tailwinds.

- Encourage capital allocation: Cheaper debt will fuel M&A and IPO activity in AI and semiconductor sectors.

However, risks remain. A prolonged rate plateau could dampen investor enthusiasm, while geopolitical inflationary pressures (e.g., Middle East conflicts) might force the Fed to pivot.

This correlation highlights how tech's fate is now intertwined with monetary policy.

Investment Strategy: Position for AI Supremacy and Strategic Materials

- Buy AI Leaders:

- Nvidia (NVDA): The undisputed leader, but monitor trade risks.

AMD (AMD): A key beneficiary of the AI boom, with its MI300A chip rivaling Blackwell.

Hedge with Strategic Materials:

- MP Materials (MP): The U.S.'s top rare earth miner, critical for magnets and semiconductors.

Talon Metals (TAL): Nickel is essential for batteries and AI infrastructure.

Diversify Geopolitical Risk:

- Invest in companies with diversified supply chains (e.g., Apple's TSMCTSM-- Arizona chips).

Track the U.S.-China trade talks—any easing of rare earth restrictions could unlock upside.

Avoid Overexposure to China:

- While companies like SMIC (semi-conductor manufacturer) may see near-term gains, long-term risks from U.S. sanctions persist.

Conclusion: The AI Era is Here—But the Fight for Dominance Has Just Begun

Nvidia's $4 trillion milestone is not just a valuation triumph—it's a geopolitical wake-up call. The AI revolution will fuel growth for decades, but its success depends on resolving supply chain fragility and navigating trade wars. Investors who pair exposure to AI leaders with strategic materials plays will thrive. Those who ignore the rare earth war and Fed dynamics may find themselves on the wrong side of this seismic shift.

The AI era is irreversible. Position accordingly.

Comentarios

Aún no hay comentarios