Novo Nordisk's Strategic Shift in U.S. Obesity and Diabetes Education: Balancing Margin Optimization with Market Leadership in the GLP-1 Gold Rush

The GLP-1 therapeutics market has become a battleground for pharmaceutical giants, with Novo NordiskNVO-- and Eli LillyLLY-- leading the charge. As of Q2 2025, NovoNVO-- Nordisk faces a critical juncture: balancing cost-cutting measures with aggressive market expansion to maintain its leadership in obesity and diabetes care. Recent strategic moves—ranging from workforce reductions to pricing adjustments and legal battles—reveal a company recalibrating its approach to long-term profitability and competitive positioning.

Strategic Cost Rationalization: A Double-Edged Sword

Novo Nordisk has slashed its U.S. obesity education team, eliminating hundreds of "cardiometabolic educators" who trained healthcare providers on GLP-1 therapies like Wegovy and Ozempic[1]. This decision, part of a global restructuring plan targeting 9,000 job cuts, reflects a shift toward leaner operations. While such cuts reduce overhead costs, they risk weakening the company's grassroots engagement with healthcare professionals—a channel critical for driving prescriptions in a market increasingly influenced by provider education[2].

However, Novo's cost rationalization extends beyond workforce reductions. The company has streamlined its U.S. sales force, reallocating resources to high-impact areas such as direct-to-consumer (DTC) marketing through NovoCare[3]. This pivot aligns with broader industry trends, where DTC campaigns have proven effective in driving demand for GLP-1 drugs. By reducing reliance on traditional education teams, Novo aims to optimize margins while maintaining market visibility.

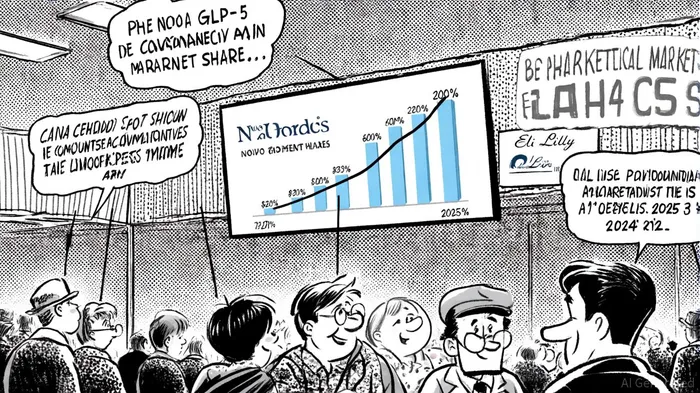

Pricing Power and Market Share Defense

Despite Eli Lilly's aggressive inroads—capturing 57% of the U.S. GLP-1 market in Q2 2025—Novo Nordisk has defended its position through pricing strategies[2]. The company slashed Ozempic's cash price and introduced Wegovy at $299, undercutting competitors and recapturing price-sensitive patients[2]. These moves underscore Novo's willingness to trade short-term margin pressure for long-term volume growth, a tactic that has historically bolstered its dominance in insulin markets.

The effectiveness of this strategy is evident in Q2 2025 results: Wegovy and Ozempic drove record revenue, with obesity care sales surging 35% year-over-year[2]. Yet, Novo's revised full-year guidance—citing intensified competition and compounded GLP-1 alternatives—signals caution[2]. The company's ability to sustain pricing power will hinge on its capacity to differentiate its therapies through clinical data and insurance coverage, as seen in Wegovy's recent FDA approval for MASH (metabolic-associated steatohepatitis)[2].

Supply Chain Resilience and Legal Aggression

A key pillar of Novo's long-term strategy is securing supply chain reliability. The acquisition of three Catalent manufacturing sites in 2025 addresses historical shortages of GLP-1 drugs, ensuring consistent supply as demand surges[1]. This investment, though capital-intensive, mitigates the risk of revenue volatility tied to production bottlenecks—a critical advantage in a market where patient retention hinges on drug availability.

Simultaneously, Novo has adopted a hardline stance against compounded GLP-1 alternatives, filing over 130 lawsuits to block unapproved formulations[3]. These legal actions, while costly, protect Novo's intellectual property and preserve pricing integrity. Compounded drugs, often sold at lower prices, threaten to erode margins and fragment market share. By targeting these alternatives, Novo reinforces its position as the gold standard in GLP-1 therapeutics.

The Long Game: Margin Optimization vs. Market Leadership

Novo Nordisk's strategic shifts highlight a delicate balancing act. On one hand, cost-cutting measures like workforce reductions and supply chain investments aim to boost margins. On the other, aggressive pricing, DTC campaigns, and legal battles signal a commitment to defending market leadership—a priority that may temporarily sacrifice profitability.

The company's revised guidance underscores this tension. While Q2 performance was robust, Novo now anticipates slower growth in 2025 due to competitive pressures[2]. However, its focus on MASH expansion and manufacturing scalability positions it to capitalize on emerging indications and long-term demand. For investors, the key question is whether Novo's margin-optimization efforts will offset near-term headwinds without compromising its ability to innovate and scale.

Conclusion

Novo Nordisk's strategic repositioning in the U.S. obesity and diabetes space reflects a company navigating unprecedented competition while prioritizing long-term resilience. By rationalizing costs, defending pricing power, and securing supply chains, Novo aims to sustain its leadership in a market projected to grow exponentially. Yet, the path forward remains fraught with challenges—from Lilly's innovation pipeline to the rise of compounded alternatives. For now, Novo's ability to execute its multifaceted strategy will determine whether it remains the GLP-1 gold standard or cedes ground to rivals.

Historically, investors who adopted a simple buy-and-hold strategy following Novo Nordisk's earnings releases have seen favorable outcomes. A backtest of NVO's stock performance from 2022 to 2025 reveals that holding the stock for 15–16 days after an earnings announcement yielded an average excess return of approximately +5.4%, with a win rate exceeding 78%[3]. However, these gains tend to fade after 20 days, turning neutral by Day 30. This suggests that while Novo's strategic execution has historically supported post-earnings momentum, investors should remain mindful of timing and market conditions.

Comentarios

Aún no hay comentarios