Nova's (NVMI) Valuation Reassessment Amid Convertible and Senior Note Financing Shifts

Nova Ltd. (NASDAQ: NVMI) has embarked on a strategic financing maneuver that underscores both its ambition and the complexities of capital structuring in a volatile market. On September 2, 2025, the company announced a $500 million private offering of 0.00% convertible senior notes due 2030, with an option for underwriters to purchase an additional $75 million, later upsized to $650 million and ultimately finalized at $750 million after full exercise of the over-allotment option [1][2]. This move, while securing critical capital, has sparked a reassessment of Nova’s valuation dynamics, revealing a nuanced interplay between financial flexibility, shareholder dilution risks, and market sentiment.

Strategic Financing: Balancing Flexibility and Dilution

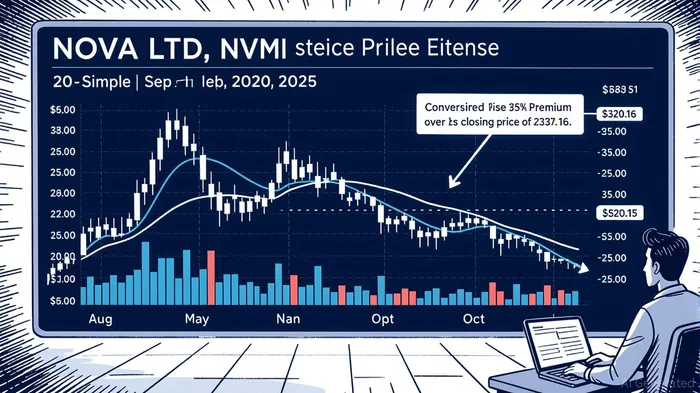

The zero-coupon structure of the notes—bearing no regular interest payments—reflects Nova’s intent to minimize immediate financial obligations while extending its cash runway until 2030 [1]. The conversion price of $320.16 per share, a 35% premium to the stock’s closing price of $237.16 on the announcement date, suggests management’s confidence in long-term growth prospects [3]. However, this premium also embeds a significant dilution risk for existing shareholders, particularly if the stock price surges above 130% of the conversion price ($416.21) in the coming years [2]. To mitigate this, NovaNVMI-- entered into capped call transactions, capping potential share price increases at $415.03, a 75% premium to the September 2 closing price [3].

This strategy aligns with broader trends in private markets, where middle- and late-stage venture capital saw a 41.8% year-over-year increase in Series C/D funding in 2024 [4]. By securing capital at a premium, Nova positions itself to pursue aggressive M&A and R&D initiatives, a tactic common among tech firms navigating macroeconomic uncertainty. Yet, the absence of traditional interest payments and the reliance on equity-linked instruments signal a shift toward shareholder value redistribution rather than debt servicing—a double-edged sword in a sector prone to rapid valuation swings.

Market Reaction: Mixed Signals and Bearish Sentiment

The market’s response to the offering has been mixed. While the 35% conversion premium initially suggested optimism, the stock price declined sharply in the days following the announcement, breaking below its 20-day simple moving average—a technical indicator often interpreted as bearish [5]. Analysts have split on the implications: some upgraded their price targets, citing Nova’s leadership in leading-edge wafer fabrication equipment (WFE) and Materials Metrology adoption [5], while others downgraded, citing conservative guidance amid global economic headwinds [5].

This divergence highlights the tension between strategic capital allocation and short-term investor psychology. The zero-coupon structure, while beneficial for cash flow, may have raised concerns about the company’s ability to meet long-term obligations without generating sufficient revenue. Additionally, the capped call transactions, while designed to limit dilution, could be perceived as a signal of management’s belief that the stock is overvalued at current levels—a perception that may have exacerbated selling pressure.

Valuation Reassessment: A Calculated Gamble

Nova’s valuation now hinges on its ability to deploy the $750 million effectively. The proceeds, earmarked for M&A, business development, and technology R&D [2], must catalyze growth sufficient to justify the embedded dilution risks. Historical data from the private markets suggests that firms leveraging convertible debt for strategic expansion often outperform peers in bull markets but face sharper corrections during downturns [4]. For Nova, the key variables will be the pace of adoption in its core markets and the macroeconomic environment’s stability.

Critically, the offering’s terms reflect a bet on sustained growth in the semiconductor and metrology sectors. With the conversion price effectively setting a floor for long-term shareholder value, Nova’s success will depend on whether its R&D investments translate into market-leading products capable of driving the stock above $415.03—a threshold that would trigger the capped calls and limit further dilution.

Conclusion: Navigating the Crossroads of Capital and Confidence

Nova’s convertible note offering exemplifies the delicate balance between securing growth capital and preserving shareholder value. While the zero-coupon structure and capped calls offer flexibility and dilution control, the immediate market reaction underscores the challenges of aligning investor expectations with long-term strategic goals. As the company moves forward, its ability to execute on M&A and R&D initiatives will be pivotal. In a sector where innovation cycles are rapid and margins are razor-thin, Nova’s valuation will ultimately be a function of its capacity to turn this capital into tangible, scalable value.

Source:

[1] Nova Ltd. Announces $500 Million Convertible Senior Notes Offering [https://www.gurufocus.com/news/3090412/nova-ltd-nvmi-announces-500-million-convertible-senior-notes-offering-nvmi-stock-news]

[2] Nova Announces Pricing of Upsized Private Offering of $650 Million 0.00% Convertible Senior Notes Due 2030 [https://www.nasdaq.com/press-release/nova-announces-pricing-upsized-private-offering-650-million-000-convertible-senior]

[3] Nova Ltd. Shares Decline as Stock Breaks Below 20-Day SMA Amid Convertible Notes Offering [https://intellectia.ai/news/monitor/nova-ltd-shares-decline-as-stock-breaks-below-20day-sma-amid-convertible-notes-offering]

[4] State of Private Markets: Q4 and 2024 in Review [https://carta.com/data/state-of-private-markets-q4-2024/]

[5] Nova at Citi's 2025 Global TMT Conference, Strategic Growth Insights [https://www.investing.com/news/transcripts/nova-at-citis-2025-global-tmt-conference-strategic-growth-insights-93CH-4225784]

Comentarios

Aún no hay comentarios