NiSource's Undervaluation Amid Regulatory Tailwinds: A Strategic Investment Opportunity in the U.S. Energy Transition

The U.S. energy sector is undergoing a seismic shift driven by regulatory mandates and environmental imperatives. For investors, this transition presents both challenges and opportunities. NiSource Inc.NI-- (NI), a mid-sized natural gas utility, stands at the intersection of these dynamics. While its current valuation appears undervalued relative to its strategic positioning, political noise and market skepticism have obscured its long-term potential. This analysis argues that NiSource's proactive alignment with regulatory trends—particularly in methane reduction, renewable natural gas (RNG), and infrastructure modernization—positions it as a compelling investment amid the energy transition.

Regulatory Tailwinds: Compliance as a Catalyst for Growth

The Environmental Protection Agency's (EPA) 2023 methane emission rules[1] and the Federal Energy Regulatory Commission's (FERC) updated pricing transparency policies[2] are reshaping the natural gas landscape. These regulations impose higher compliance costs but also incentivize innovation. NiSourceNI-- has embraced this duality. As a former Methane Challenge Partner, it reduced emissions by 3,658 metric tons through infrastructure upgrades, saving $762,150 in gas costs[3]. Such initiatives not only align with EPA mandates but also enhance operational efficiency—a critical factor for utilities navigating rising compliance expenses.

FERC's approval of NiSource's $19.9% equity stake sale in its Northern Indiana Public ServicePEG-- Company (NIPSCO) subsidiary to BlackstoneBX-- Infrastructure Partners[4] further underscores its strategic agility. This transaction, expected to close by late 2023, strengthens NiSource's balance sheet, enabling capital expenditures for infrastructure modernization and RNG integration. By leveraging private equity partnerships, the company mitigates regulatory risks while accelerating its transition to cleaner energy.

Renewable Natural Gas: A Goldmine in the Energy Transition

Renewable natural gas (RNG), a carbon-neutral alternative derived from organic waste, is central to NiSource's long-term strategy. The company's Green Path℠ program already offers RNG to customers without infrastructure overhauls[5], and its advocacy for policies like Virginia's Energy Innovation Act[6] signals a commitment to scaling RNG adoption.

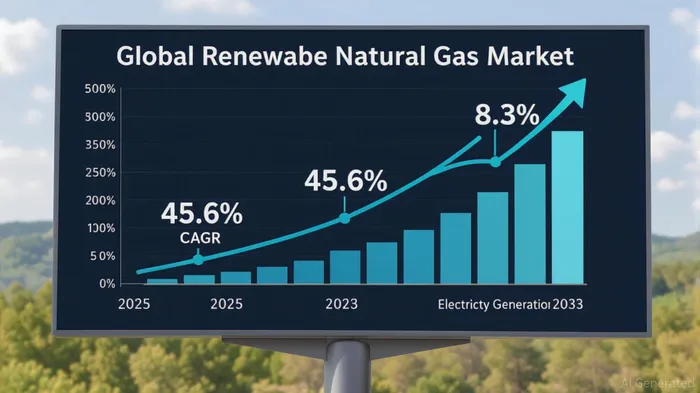

The RNG market's projected growth reinforces this strategy. By 2033, the global RNG market is forecasted to reach $216.51 billion at a 45.6% CAGR[7], with North America leading at a 44.8% CAGR[8]. Even the more conservative 8.3% CAGR estimate[9] highlights a $26.57 billion market by 2032. For NiSource, which operates in key RNG growth regions like Indiana and Ohio, these trends represent a direct revenue stream. Its ability to integrate RNG without costly infrastructure modifications[10] gives it a competitive edge over peers reliant on traditional gas pipelines.

Financial Metrics: A Discounted Yet Resilient Valuation

NiSource's 2025 trailing P/E ratio of 20.83 and forward P/E of 20.35[11] suggest a discount relative to its projected 10.38% annual earnings growth[12]. Analysts have assigned a “Buy” consensus rating with a $43.88 average price target[13], implying a 10–15% upside from its current price. Meanwhile, its 2.81% dividend yield and 58.2% payout ratio indicate a sustainable and attractive income stream for investors.

The company's P/B ratio, though fluctuating between 1.74 and 2.10 in 2025, remains well below the industry average for utilities (typically 2.5–3.0). This discrepancy suggests the market is underappreciating NiSource's asset base and growth potential, particularly in RNG and hydrogen injection projects.

Political Noise vs. Structural Resilience

Critics may argue that NiSource's reliance on natural gas exposes it to regulatory and environmental risks. However, its “balanced” approach—combining infrastructure upgrades with RNG and hydrogen investments—mitigates this concern. Unlike peers fully pivoting away from gas, NiSource leverages its existing network to deliver cleaner alternatives, reducing stranded asset risks.

Moreover, the political noise surrounding fossil fuels often overlooks the role of natural gas as a transitional fuel. With RNG and hydrogen blending, NiSource is positioning itself as a bridge to decarbonization rather than a relic of the past.

Conclusion: A Strategic Buy for the Energy Transition

NiSource's undervaluation is a function of short-term regulatory headwinds and market skepticism, not a reflection of its long-term potential. Its proactive engagement with methane reduction, RNG adoption, and strategic partnerships like the NIPSCO sale align it with the energy transition's core drivers. With a compelling dividend yield, favorable analyst ratings, and a valuation discount to its asset base, NiSource offers a rare combination of defensive resilience and growth potential. For investors seeking exposure to the U.S. energy transition, this is a strategic opportunity worth seizing.

Comentarios

Aún no hay comentarios