Las prácticas de entrenamiento de Nighthawk continúan: un catalizador táctico para el papel especulativo de Bitterroot.

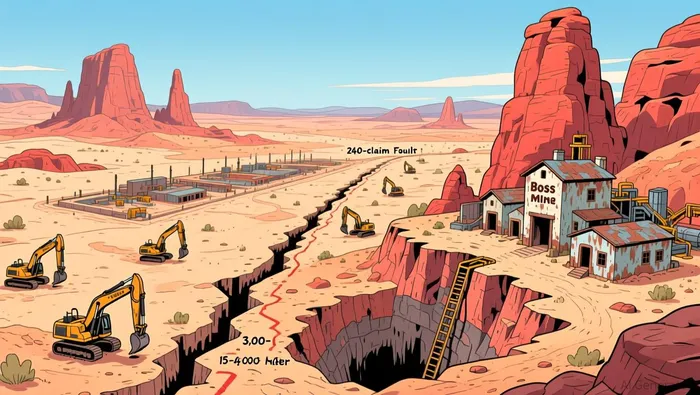

El catalizador inmediato ya está en marcha. La Oficina de Administración de Tierras de los EE. UU. ha aprobado la notificación de operaciones relacionada con el proyecto Nighthawk en Bitterroot. Esto elimina una de las principales barreras regulatorias. Esta autorización permite la construcción de hasta 15 sitios de perforación y el transporte terrestre correspondiente en el área de 240 acres que se encuentra en el distrito de Walker Lane, en Nevada. La aprobación abre el camino para que las operaciones de perforación puedan reanudarse, después de una breve pausa debido a problemas con los contratistas. Se espera que un nuevo equipo basado en Nevada reanude las operaciones a finales de enero.

El plan de gestión es un test preciso y de alto impacto del potencial del proyecto. Se pretende que se realicen 3.000 a 4.000 metros de perforación de círculos verticales en 15 a 20 agujeros inclinados. El foco se centra en siete objetivos estructurales de hasta un kilómetro de longitud identificados por medio de magnetoformación de drones, y se están analizando específicamente depósitos de oro y plata en oxidados epitermales en la superficie del suelo. El contexto del proyecto es un gran plus: se trata de un 100% de propiedad, sin comisión, y se sitúa contiguo a la antigua y productora mina Boss. Esto facilita la exploración de zonas nuevas tanto en cuanto al entorno geológico conocido.

Para un negocio de tipo especulativo con riesgo bajo, esto representa un evento claro en el corto plazo. La reanudación de las perforaciones es el primer paso concreto para probar estos objetivos de alto potencial. Resultados positivos podrían generar valor rápidamente, al reducir el riesgo asociado al potencial de recursos del proyecto. Dada la magnitud de la acción y la naturaleza binaria de los resultados de la exploración, es probable que la reacción del mercado ante los datos iniciales de perforación sea rápida e inmediata.

La tendencia de la Walker Lane: geología y riesgos

La lógica geológica en este caso es una clásica estrategia de exploración en terrenos nuevos, basada en tendencias conocidas. La empresa tiene como objetivo explorar siete zonas estructurales de varios kilómetros de extensión, a lo largo de una línea de 15 kilómetros. Estas zonas son estructuras falleras que no habían sido investigadas antes; fueron identificadas mediante técnicas de medición magnética con drones. Estas zonas se encuentran dentro del distrito minero de Walker Lane, donde existen importantes yacimientos minerales, como la mina Boss. El enfoque principal es la exploración de yacimientos de oro y plata en superficies cercanas al suelo. Este tipo de yacimientos suele ser adecuado para la perforación por métodos de baja costo.

Una de las principales ventajas es la presencia de un manto superficial reducido. La zona de proyecto se encuentra a nivel medio con una superficie del pedimento ligeramente inclinada, y se espera que las profundidades del manto superficial varíen entre0-30 metrosEste cubrimiento superficial reduce significativamente el riesgo de perforación y sus costos, lo que hace que el programa de pruebas iniciales sean más eficientes y reduzca la barrera para desconocer el riesgo de estos objetivos.

Sin embargo, el principal riesgo operativo radica en los aspectos mecánicos y humanos. La reciente pausa en las actividades de perforación fue causada directamente por un contratista.problemas mecánicos recurrentesEsto destaca una vulnerabilidad crítica: el éxito del catalizador a corto plazo depende de la fiabilidad del nuevo equipo ubicado en Nevada. Cualquier retraso adicional en el reinicio de las operaciones, o cualquier problema durante el proceso, podría hacer que los resultados sean menos favorables durante esa etapa de transacciones. Esto, a su vez, aumentaría los costos y agotaría la paciencia de los inversores.

El método de riesgo/compensación es, por lo tanto, binario y basado en eventos. La superficie destruida superficial y la proximidad a un importante trend son factores geológicos ventajosos que podrían generar una rápida y positiva conclusión. Pero el reciente retraso del contratista es un señal tangible que podría retrasar el resultado. Para una jugada especulativa con bajo nivel, el mercado se verá esta fase de ejecución estudiando a fondo.

Valoración y reacción del mercado: Una operación especulativa de bajo riesgo

La actual posición de la compañía es un juego de especulación de bajo flujo, tal como los ejemplos de libros de texto. Bitterroot tiene una valoración de mercado de $1.472 billones, con el precio a la baja en $22.77. Esta valoración implica poco o ningún valor para el proyecto Nighthawk más allá de la reciente aprobación regulatoria. El mercado está poniendo en valores el riesgo de fracaso de la ejecución, tal como lo demuestra el 0.17% de la rotación de la bolsa durante los 20 días y la mínima volatilidad. Este déficit de liquidez e interés es típico de estos nombres, donde la mayoría de acciones son tomadas por un grupo concentrado de inversionistas, dejando a la bolsa vulnerable a cambios bruscos por noticia.

El catalizador aquí es binario. Un resultado de inyección positivo podría desencadenar una rápida revalorización, dada la cercanía convincente del proyecto a depósitos conocidos. Las afirmaciones de Nighthawk sonContiguo a la mina Boss, que produce mineral en el pasado.y los objetivos identificados se encuentran a lo largo de unaLongitud de 15 kilómetros de estructuras de fallas modificadas, que hasta ahora eran desconocidas y no habían sido sometidas a ningún tipo de prueba.dentro del trend de la Walker Lane. Si las perforaciones iniciales de RC confirman la mineralización epitermales en proximidad a la superficie, ello reduciría el riesgo de una oportunidad significativa de campo y probablemente impuse una nueva evaluación sobre el potencial de recursos del proyecto. En un entorno con bajo liquidez, incluso un volumen modesto de compra podría impulsar el precio de forma drástica.

El punto clave es el momento y la calidad de los primeros resultados obtenidos durante la práctica. El programa se reanudará a finales de enero, y la empresa tiene como objetivo…De 3.000 a 4.000 metros de perforación.El mercado buscará una confirmación temprana del modelo geológico, especialmente en los siete objetivos estructurales de varios kilómetros de extensión. Cualquier resultado positivo validaría a los objetivos de alto potencial y podría cambiar rápidamente la situación, pasando de una situación de aprobación regulatoria a una situación de descubrimiento real. Por el contrario, cualquier retraso adicional o resultados insuficientes probablemente consolidarían el descuento que se aplica actualmente a dichos objetivos.

La conclusión es que el precio actual refleja una alta probabilidad de fracaso. Para un inversor táctico, la configuración es clara: la acción se está negociando cerca del máximo de 52 semanas de $22,92 con un mínimo de momentum reciente, lo que sugiere que el mercado tuvo en cuenta el aprobado de la BLM pero no el riesgo de ejecución. Las próximas semanas son cruciales. La reanudación del perforado es el primer paso tangible, pero los primeros resultados de la prueba determinarán si la valoración actual es un error o una reflexión justa de la incierta trayectoria del proyecto.

Línea de tiempo y hitos clave

El catalizador más inmediato es el estallido de los primeros resultados de perforación. Cuando se espera que la perforación reanude su actividad a finales de enero, la compañía comprobará hasta cinco objetivos para encontrar la epitermial de oro/plata. Los primeros resultados de las analíticas, probablemente dentro de pocas semanas de la reanudación del programa, serán el primer punto de referencia de los datos de la zona de alta potencial. Interceptaciones positivas confirman el modelo geológico y podrían impulsar una reevaluación rápida, mientras que resultados débiles confirmarían, probablemente, el descuento especulativo actual de la bolsa.

Un riesgo financiero importante es que los retrasos puedan prolongar el programa más allá de los 15-20 hoyos previstos. La pausa reciente se debió directamente a problemas con un contratista.problemas mecánicos recurrentesSe trata de una vulnerabilidad crítica. Cualquier problema adicional que surja con el equipo nuevo, basado en Nevada, podría retrasar el cronograma de ejecución, aumentar los costos y poner a prueba la paciencia de los inversores. La empresa ha logrado mejorar los objetivos de su planificación mediante estudios sísmicos, pero el riesgo de error en la ejecución sigue siendo alto.

El punto operativo principal a corto plazo es el rendimiento del contratista. El éxito del catalizador depende de la fiabilidad de este nuevo equipo. Los inversores deben vigilar cualquier actualización sobre el avance del perforado o problemas mecánicos, ya que estos serán el primer indicio de si el programa sigue el camino. Lo importante es que el cronograma es estrecho y la margen de error es pequeña. Los primeros resultados determinarán si la valoración actual es un valor incorrecto o una reflexión justa del camino incierto del proyecto.

Niveles de precios y configuración de riesgo/recompensa

La cotización se encuentra en un punto de inflexión. Con un precio actual de $22.80, se sitúa justo por debajo de su máximo de 52 semanas de $22.92. Esta posición ofrece una reducción limitada, con un mínimo de 52 semanas de $20.20 que representa una reducción potencial de cerca de 10%. Sin embargo, también limita el incremento a corto plazo a menos que un catalizador impulse un rompimiento.

El riesgo principal es que el resultado del entrenamiento sea negativo o que ocurran más retrasos en las operaciones. La pausa reciente se debió a problemas relacionados con un contratista.problemas mecánicos que se repitenEs una señal de alerta evidente, y es muy probable que se repita. Un resultado débil o otro retraso en los resultados podrían llevar a que la acción vuelva a su nivel más bajo, consolidando así el descuento actual en el precio de la acción. El bajo número de acciones en circulación y la baja actividad del mercado indican que el mercado no está asignando ningún valor real a este riesgo. Por lo tanto, la acción es vulnerable a una caída brusca debido a malas noticias.

Sin embargo, el potencial de ganancia es importante y está determinado directamente por el catalizador. Un resultado positivo de la perforación que confirma la mineralización epítectica a nivel de superficie desactivará el riesgo de una oportunidad de exploración de gran escala. Dada la proximidad del proyecto aLa mina que produce productos del pasadoY, en los títulos de alto potencial, como la noticia podría provocar una rápida reclasificación. El precio podría moverse rápidamente hacia niveles vistos durante los éxitos de exploración pasados, potencialmente rompiendo los $25. Esto representaría un aumento significativo del precio actual.

Por lo tanto, la estructura de riesgo/retorno es binaria y está determinada por los acontecimientos futuros. El precio del activo se encuentra cerca de sus límites altos, pero el camino hacia un aumento significativo es estrecho y depende completamente de la ejecución del programa de perforación y de la calidad de los primeros resultados obtenidos. Para un inversor táctico, el punto de entrada no es barato, pero la posible recompensa que se puede obtener con un catalizador positivo justifica el riesgo. Las próximas semanas determinarán si el precio actual representa una subestimación o si es una reflección justa de la trayectoria incierta del proyecto.

Comentarios

Aún no hay comentarios