NEO Battery's Strategic Expansion and Capital Raise: A Catalyst for the EV Battery Supply Chain

The electric vehicle (EV) battery industry is undergoing a seismic shift, driven by the urgent need for higher energy density and sustainable materials. At the forefront of this transformation is NEO Battery Materials, a Canadian firm leveraging silicon anode technology to disrupt the lithium-ion battery supply chain. Recent developments—including a $2.1 million CAD capital raise and a $120-million silicon anode plant in Windsor, Ontario—underscore the company's strategic ambition to secure a pivotal role in North America's EV ecosystem. This analysis evaluates NEO's positioning, the implications of its capital infusion, and the broader investment landscape for silicon anode materials.

Capital Raise: Fueling R&D and Production Scaling

In July 2025, NEO Battery completed the final tranche of a private placement, raising $1.4 million CAD, bringing total proceeds to $2.1 million CAD [1]. The offering issued 1.4 million units at $0.50 CAD each, with each unit comprising one common share and one-half warrant. The funds will accelerate research and development, expand production capacity, and fortify the company's balance sheet [1]. This capital infusion is critical for addressing the technical and financial challenges inherent in scaling silicon anode technology, which, despite its promise, remains costly and complex to manufacture.

The strategic use of these funds aligns with a broader industry trend: investors are increasingly prioritizing firms that can bridge the gap between cutting-edge materials science and commercial viability. For NEO, the capital raise not only stabilizes its financial position but also signals confidence in its ability to deliver on its roadmap. As stated by Markets Gone Wild, stakeholders stand to benefit from “potential capital appreciation” as the company advances its silicon anode commercialization and strengthens its supply chain partnerships [1].

Strategic Partnerships and Manufacturing Plans

NEO's recent $120-million plant in Windsor, Ontario, represents a bold bet on the future of North American batteryABAT-- production. The facility, secured via a 49-year lease, aims to produce 5,000 tonnes of silicon anode material annually, directly supporting the region's goal to scale EV battery cell production to 1.2 terawatt-hours (TWh) by 2030 [2]. This infrastructure investment is complemented by a joint development agreement (JDA) with a North American battery cell manufacturer, focusing on optimizing silicon anode performance for automotive and mobility applications [2].

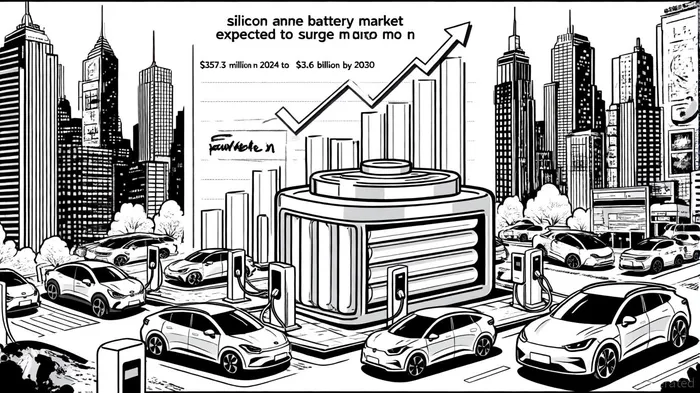

Such partnerships are vital for overcoming the technical hurdles of silicon anodes, which, while offering up to 3,600 mAh/g energy density (compared to graphite's 372 mAh/g), face challenges like structural degradation during charge cycles [3]. By collaborating with industry leaders, NEO can integrate advanced material science—such as silicon-carbon composites—to enhance durability and reduce costs. These efforts position the company to capitalize on the projected $3.6 billion silicon anode market by 2030, growing at a 50.1% CAGR [4].

Market Dynamics and Investment Implications

The global demand for silicon anode materials is surging, driven by EVs' need for longer ranges and faster charging. The market, valued at $357.3 million in 2024, is expected to reach $3.6 billion by 2030 [4]. Meanwhile, the silicon-based anode material market is projected to balloon from $967.38 million in 2024 to $48.4 billion by 2033, at a 54.47% CAGR [5]. This growth is fueled by EVs, consumer electronics, and energy storage systems, with companies like TeslaTSLA-- and Sila Nanotechnologies already integrating silicon-dominant anodes into their products [5].

However, the market is not without risks. High production costs and technical complexities remain barriers to widespread adoption. For instance, silicon anodes' tendency to expand and contract during charge cycles increases manufacturing costs and reduces battery lifespan [5]. NEO's focus on low-cost production and strategic R&D partnerships could mitigate these challenges, but execution risks persist.

From an investment perspective, NEO's positioning in the North American supply chain offers a unique advantage. Unlike lithium iron phosphate (LFP) batteries, which are heavily concentrated in China, silicon anode materials can diversify supply chains and reduce geopolitical risks. This aligns with global efforts to localize EV battery production, a trend that could amplify demand for NEO's offerings.

Conclusion: A High-Stakes Bet on the Future of Batteries

NEO Battery's capital raise and manufacturing plans reflect a calculated strategy to capture a significant share of the silicon anode market. While the company's technological and geographic positioning are compelling, investors must weigh the risks of scaling a nascent technology against the potential rewards of a market growing at over 50% annually. Success hinges on its ability to reduce production costs, secure long-term partnerships, and navigate the technical complexities of silicon anodes. For those willing to tolerate the volatility of an emerging sector, NEO represents a high-conviction opportunity in the EV battery revolution.

Comentarios

Aún no hay comentarios