Navigating Retirement Savings in 2025: Strategic Asset Allocation and Inflation Resilience Strategies

The Retirement Savings Dilemma in a High-Inflation Era

Retirees in 2025 face a dual challenge: preserving capital in a low-growth, high-inflation environment while ensuring sufficient liquidity to cover extended lifespans. According to a report by LPL Research, strategic asset allocation must now prioritize income generation and inflation resilience[2]. With core PCE inflation projected at 3.1% for 2025[3] and the Federal Reserve signaling a "higher-for-longer" interest rate environment[1], traditional fixed-income investments alone cannot safeguard purchasing power. This necessitates a rebalanced portfolio structure that integrates growth-oriented equities, inflation-protected bonds, and alternative assets.

Strategic Asset Allocation: A Modernized Framework

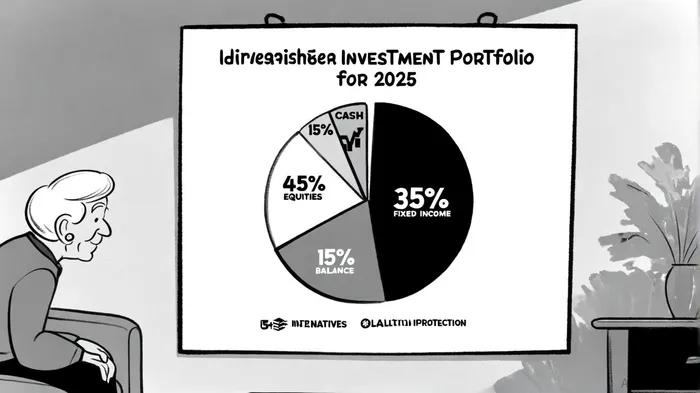

A 2025 roadmap for retirement savings emphasizes a 40–50% equity allocation, focusing on dividend-paying blue-chip stocks, low-volatility ETFs, and international exposure[1]. These instruments not only offer growth potential but also provide consistent cash flows to counteract inflation. For example, global infrastructure and emerging markets are gaining traction as they align with long-term economic expansion and diversification[2].

Fixed income remains critical but must be restructured. Short- to intermediate-term bonds and Treasury Inflation-Protected Securities (TIPS) now constitute 30–40% of the portfolio, with TIPS offering a direct hedge against inflation by adjusting principal values with the Consumer Price Index (CPI)[6]. Meanwhile, cash and cash equivalents (10–20%) ensure liquidity for immediate expenses, reducing the need to sell assets during market downturns[1].

Alternative investments, such as multi-strategy funds and managed futures, are increasingly recommended to hedge volatility[2]. These tools, combined with real assets like commodities and real estate investment trusts (REITs), diversify risk and provide non-correlated returns[4].

Inflation Resilience: Beyond Traditional Safeguards

Inflation resilience requires a multi-pronged approach. TIPS remain foundational, with their yields outpacing current inflation rates[6]. For instance, the 2-year Treasury yield of 3.72% offers modest protection, but TIPS' inflation-adjusted principal ensures long-term stability[1].

Equities, particularly those with pricing power, historically outperform inflation. Companies in sectors like healthcare and technology can pass rising costs to consumers, maintaining profitability[1]. Dividend stocks, such as those in the S&P 500, have demonstrated a 5–7% annualized return above inflation over the past decade[5].

Real estate, whether through direct ownership or REITs, also serves as a robust inflation hedge. Property values and rental income typically rise with inflation, preserving real returns[2]. For retirees without physical assets, REITs offer liquidity and diversification without management burdens[1].

Economic Tailwinds and Policy Implications

The Federal Reserve's September 2025 rate cut to 4.00–4.25% reflects a shift toward risk management amid a cooling labor market and persistent inflation[3]. While this provides temporary relief, retirees must anticipate continued volatility. J.P. Morgan's Global Asset Allocation report highlights a pro-risk stance, favoring U.S. tech equities and sovereign bonds to capitalize on yield differentials[4].

However, the "higher-for-longer" rate environment complicates bond strategies. Short-duration bonds are preferable to mitigate interest rate risk, while high-yield corporate bonds offer higher returns for those with moderate risk tolerance[2].

Tax Efficiency and Systematic Withdrawals

Tax drag remains a critical concern. A diversified portfolio across taxable, tax-deferred, and tax-free accounts (e.g., Roth IRAs) minimizes liabilities[1]. Systematic withdrawal strategies, such as the 4% rule adjusted for inflation, ensure longevity while avoiding over-withdrawal during market downturns[5].

Conclusion: A Balanced Path Forward

Retirement savings adequacy in 2025 hinges on a dynamic, adaptive strategy. By blending equities for growth, TIPS for inflation protection, and alternatives for diversification, retirees can navigate economic uncertainties. As the Federal Reserve navigates its delicate balancing act, a proactive approach to asset allocation and tax efficiency will remain paramount.

Comentarios

Aún no hay comentarios