Navigating Post-Recession Recovery: Tactical Sectors for 2025 Equity Gains

The global economy is navigating a fragile post-recession recovery, with growth projections of 3.0% for 2025 and 3.1% for 2026, according to the IMF's July 2025 update [1]. While improved financial conditions and fiscal expansion in major economies have bolstered optimism, risks such as rising tariffs, geopolitical tensions, and uneven inflationary pressures persist [1]. For investors, this environment demands a tactical approach to equity market rotation, prioritizing sectors poised to capitalize on structural trends while mitigating exposure to cyclical vulnerabilities.

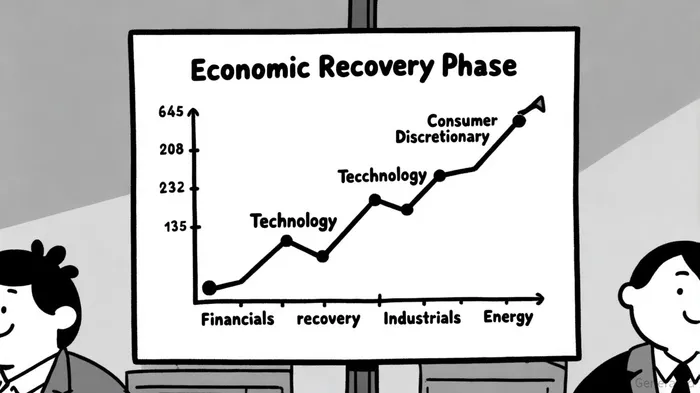

Historical Rotation Patterns and 2025's Economic Cycle

Post-recession recoveries typically follow a predictable sector rotation pattern. Financials861076-- often lead early recoveries, benefiting from favorable interest rates and credit demand [2]. This is followed by Technology, as innovation drives productivity gains, and Consumer Discretionary, as spending rebounds. Later stages see strength in Industrials and Energy, reflecting demand for goods and infrastructure [2].

In 2025, the economic cycle appears to be in the early-to-mid recovery phase. The U.S. Federal Reserve's unchanged policy rate and the ECB's recent 25-basis-point cut to 2.15% signal a cautious stance, while global trade growth—revised upward to 0.9%—suggests tentative normalization [1]. However, U.S. effective tariff rates have surged to 18%, complicating trade dynamics and dampening business and consumer sentiment [1].

Undervalued Sectors: Financials, Healthcare, and Energy

Amid this backdrop, three sectors stand out for their valuation appeal and alignment with macroeconomic trends:

Financials: Trading at a forward P/E of 18.09 and a P/B of 2.33, regional banks and insurers remain attractively priced [3]. Despite a modest earnings recovery since 2023, the sector benefits from rising interest rates and a resilient economic backdrop. BarclaysBCS-- notes that financial markets are increasingly focused on AI-driven earnings potential, further enhancing long-term value [4].

Healthcare: A P/E of 21.37 and a P/B of 4.86 reflect moderate valuations, with biotech and medical device firms trading at discounts to intrinsic value [3]. MorningstarMORN-- highlights that demographic-driven demand for healthcare services861198-- and private-sector innovation could stabilize earnings growth, even as regulatory pressures persist [5].

Energy: While oil prices have declined, energy stocks trade at a 14% discount to fair value estimates, offering a hedge against inflation and geopolitical risks [5]. The sector's transformation toward renewables and energy transition technologies adds a layer of growth potential, though demand uncertainties remain.

Tactical Reallocation: Balancing Risk and Growth

The case for immediate capital reallocation hinges on three factors:

- Valuation Gaps: Financials and Healthcare trade at significant discounts to historical averages, offering margin of safety.

- Macro Tailwinds: Fiscal expansion and AI-driven productivity gains could accelerate demand for technology and financial services.

- Defensive Positioning: Energy and Healthcare provide resilience against inflation and trade policy shocks.

However, investors must remain vigilant. The U.S. inflation outlook remains above target at 2.9%, and global GDP growth is projected to decelerate to 2.9% in 2025–2026 [4]. Tariff-driven price pressures on autos and consumer goods also pose near-term risks [1].

Conclusion

The post-recession landscape demands a disciplined, sector-specific approach. By leveraging historical rotation patterns and current valuation metrics, investors can position portfolios to capitalize on undervalued growth assets while hedging against macroeconomic headwinds. Financials, Healthcare, and Energy emerge as compelling candidates, offering a blend of affordability, earnings resilience, and long-term structural potential.

Comentarios

Aún no hay comentarios