Navigating Post-Pandemic Inflation: Central Bank Credibility and Evolving Asset Allocation Strategies

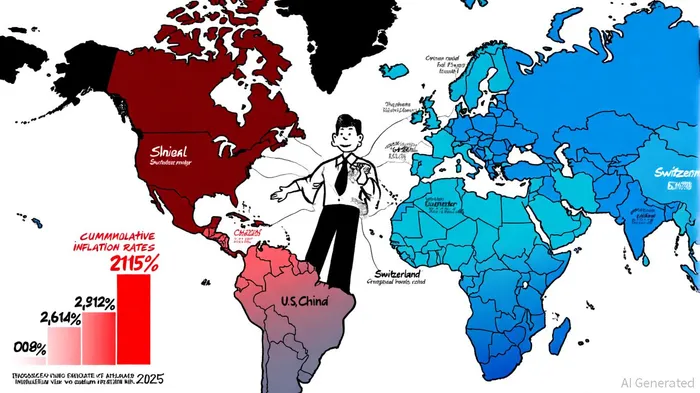

The post-pandemic era has been defined by a paradox: unprecedented fiscal and monetary stimulus collided with supply chain disruptions, geopolitical shocks, and shifting consumer behavior to create a volatile inflationary landscape. By June 2025, global inflation had diverged sharply, with Argentina's cumulative inflation hitting 2,614% while China's remained at 6%, according to the Visual Capitalist map. Central banks, once accused of underestimating inflation's persistence, have since recalibrated their strategies, balancing credibility with the need to avoid stifling growth. Meanwhile, investors have adapted their asset allocation tactics to navigate this new regime, prioritizing diversification and flexibility.

Central Bank Credibility: A Hard-Won Asset

Central banks faced a credibility crisis in the early stages of the post-pandemic recovery. The Federal Reserve and the European Central Bank (ECB) initially labeled inflation as "transitory," a misjudgment that eroded public trust, as noted in a Federal Reserve note. However, by 2024, policymakers began to pivot. The Fed removed the word "transitory" from its lexicon, while the ECB initiated eight rate cuts by mid-2025 to address moderating inflation and weak growth, according to the Global Macroeconomic Outlook. These adjustments were critical in re-anchoring inflation expectations.

Credibility, as academic research underscores, is not just a reputational asset-it directly enhances the effectiveness of monetary policy, as shown in a Wiley study. For instance, Switzerland's central bank cut rates to 0% in May 2025 after experiencing negative inflation, a move that signaled its commitment to price stability, as the Visual Capitalist map illustrates. Similarly, an ICIS insight notes that the IMF has warned that if inflation expectations become "de-anchored," central banks could face a far steeper path to normalization. The concept of "higher for longer" rates has emerged as a compromise, allowing banks to avoid premature easing that might reignite inflationary pressures, as discussed in How Central Banks Are Steering Inflation.

Asset Allocation in a Disinflationary Transition

Investors have responded to the evolving inflation narrative with a blend of caution and opportunism. Traditional fixed income's role as a diversifier has weakened due to persistent inflation and policy-driven yield volatility, according to a Farther post. Instead, asset allocators have favored:

- Equities with Inflation Hedges: U.S. mid- and small-cap stocks, which offer more attractive valuations than large-cap peers, have outperformed. International equities also gained traction as the U.S. dollar weakened, boosting returns in developed markets, per the J.P. Morgan report.

- Active Fixed Income Strategies: Short-dated Treasury Inflation-Protected Securities (TIPS) and active yield curve management-particularly in the 3- to 7-year segment-have become popular for their yield and duration risk balance, a point emphasized in a BlackRock note.

- Alternatives and Commodities: Digital assets and commodities are increasingly viewed as uncorrelated return drivers, with gold and energy sectors benefiting from inflationary tailwinds, according to a MetLife note.

J.P. Morgan's Q3 2025 asset allocation report recommends an overweight in Italian BTPs and UK Gilts, citing Europe's improving growth outlook and the ECB's dovish pivot. Meanwhile, BlackRockBLK-- emphasizes the need for "structural diversification," urging investors to rebalance portfolios toward global equities and macro hedge funds to mitigate concentration risks in AI-driven U.S. markets.

The Road Ahead: Challenges and Opportunities

While global inflation is projected to decline to 5.43% in 2025, challenges persist. Services inflation remains stubbornly elevated, and geopolitical risks-such as Middle East tensions and U.S. tariff policies-threaten to disrupt disinflationary trends, according to an IMF blog. Central banks must now navigate a "triple pivot" strategy, combining monetary easing with fiscal and structural reforms to sustain growth.

For investors, the key takeaway is adaptability. A pro-risk stance in equities is justified by strong fundamentals, but credit markets require caution due to tight spreads. Sovereign bonds, particularly in Europe, offer relative value, while alternatives provide a buffer against macroeconomic shocks, as highlighted in the MetLife analysis.

In this environment, central bank credibility remains the linchpin of stability. As history shows, when policymakers act decisively and transparently, they not only control inflation but also create the conditions for investors to thrive.

Comentarios

Aún no hay comentarios