Navigating the Policy Divide: Dimon's Warnings on Europe and US Tariffs Shape Investment Horizons

The widening economic chasm between Europe and the United States, as highlighted by JPMorgan ChaseJPM-- CEO Jamie Dimon in recent public remarks, is reshaping investment landscapes. Dimon's stark warnings about Europe's declining competitiveness—driven by structural inefficiencies—and his caution about U.S. protectionist trade policies underscore a critical divergence in macroeconomic strategies. This divide creates both risks and opportunities for investors, demanding a nuanced approach to sectoral allocations and geographic exposure.

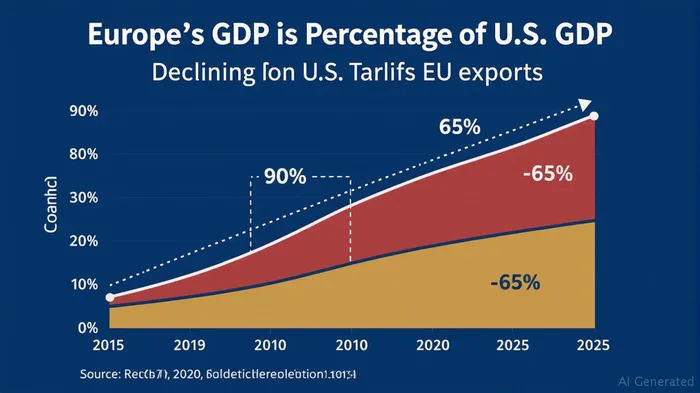

Europe's Stagnation: Structural Fault Lines and Investment Risks

Dimon's analysis paints a bleak picture of Europe's economic trajectory. Over the past decade, the EU's GDP has slipped from 90% of U.S. GDP to 65%, a decline he attributes to fragmented regulatory systems, lagging innovation, and insufficient integration. Key structural challenges include:

- Regulatory Fragmentation: The lack of a unified single market across banking, taxation, and climate policies stifles cross-border capital flows and hampers competitiveness.

- Innovation Lag: Europe's tech and energy sectors trail the U.S. and Asia, exacerbated by underinvestment in R&D and digital infrastructure.

- Trade Barriers: Ongoing disputes with the U.S. over tariffs—such as those on copper and pharmaceuticals—threaten export-dependent economies like Ireland, which relies on global supply chains.

Market Implications:

- Equity Exposure: European equities, particularly in industrials and financials, face headwinds. The Stoxx Europe 600 Industrials index has underperformed the S&P 500 Industrials by 22% over five years, reflecting weaker growth prospects.

- Currency Risks: The euro's decline—driven by inflation and policy uncertainty—adds pressure to euro-denominated assets.

- Sectoral Weakness: Energy and materials sectors, already strained by geopolitical tensions, face further drag from regulatory fragmentation and underinvestment.

U.S. Protectionism: Tariffs, Inflation, and Tactical Opportunities

Dimon's critique of U.S. trade policies centers on complacency toward the risks of escalating protectionism. While markets have historically bet on President Trump reversing tariff threats (the “TACO Trade”), Dimon warns that this time could be different. Recent tariff hikes on Brazil and Japan, coupled with fiscal deficits and migration-driven inflation, raise the likelihood of Fed rate hikes beyond market expectations.

Key Sectors and Risks:

- Inflation-Driven Sectors: U.S. manufacturers protected by tariffs—such as steel and automotive parts—could benefit from reduced foreign competition.

- Tech and Energy: U.S. tech firms, insulated by domestic demand and innovation, may outperform European peers. Energy stocks, particularly those with exposure to North American shale, could gain as geopolitical tensions boost oil prices.

- Inflation Hedging: Gold and real estate investment trusts (REITs) remain viable hedges against the “stickier inflation” Dimon anticipates.

Tactical Allocations: Capitalizing on Policy-Driven Shifts

Investors must navigate this divide by prioritizing resilience over growth in European markets while leveraging U.S. sectoral strengths:

- Underweight European Equities: Reduce exposure to Stoxx 600-heavy portfolios, particularly in industrials and banks.

- Overweight U.S. Manufacturing: Target companies like CaterpillarCAT-- or 3MMMM--, which benefit from tariffs shielding domestic production.

- Focus on Innovation Leadership: Invest in U.S. tech firms (e.g., NVIDIANVDA--, Microsoft) and biotech leaders (e.g., Moderna), which dominate global markets.

- Inflation-Hedged Portfolios: Allocate 5–10% to gold (GLD) or inflation-protected bonds (TIPS) to buffer against Fed rate surprises.

Conclusion: The Policy Divide as an Investment Compass

Dimon's warnings crystallize a stark reality: Europe's stagnation and U.S. protectionism are not transient issues but structural challenges defining the next decade. Investors ignoring this divide risk mispricing risks in sectors like European equities or underestimating the staying power of U.S. tariffs. By aligning allocations with policy outcomes—favoring U.S. innovation and inflation hedges while hedging against European stagnation—investors can navigate this geopolitical and economic divide with confidence.

As Dimon's words remind us: complacency is the greatest risk of all.

Comentarios

Aún no hay comentarios