Navigating the New Normal: Defensive Investment Strategies in Emerging Markets Amid China's Economic Transition

China's economic trajectory has sparked intense debate in 2025, with critics labeling it "stagnant" and optimists pointing to resilience amid headwinds. The International Monetary Fund (IMF) and World Bank have revised their forecasts upward for 2025, projecting 4.8% growth for China, driven by fiscal expansion and front-loaded trade activity despite U.S. trade tensions, according to the World Bank forecast. Yet, structural challenges-aging demographics, a property sector crisis, and subdued exports-loom large, as noted by the World Economic Forum. This duality creates a pivotal moment for global investors, particularly in emerging markets (EMs), where defensive strategies are reshaping portfolios.

The Myth of Stagnation: A Nuanced View of China's Growth

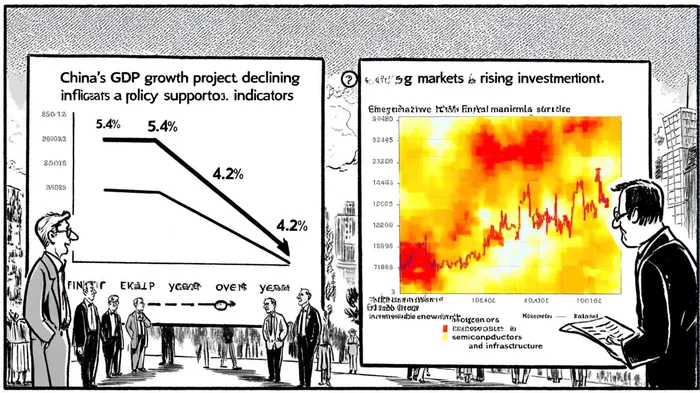

China's growth, while decelerating, remains robust compared to advanced economies. The World Bank's October 2025 update raised its 2025 forecast to 4.8%, citing "policy-driven stimulus and resilient domestic consumption." The IMF similarly upgraded its 2023–2024 forecasts to 5.4% and 4.6%, respectively, noting stronger-than-expected third-quarter performance, as reported in a SCMP article. However, these gains mask vulnerabilities. The property sector, which accounts for 30% of GDP, remains in turmoil, and external demand is softening as global trade tensions escalate, according to an Atlas Institute analysis.

For investors, the key takeaway is that China's slowdown is structural, not terminal. Policy interventions-such as consumer trade-in programs and green energy subsidies-are designed to pivot growth toward high-quality, sustainable models, according to an AMRO report. Yet, external risks, including potential U.S. tariff hikes, remain a wildcard.

Defensive Strategies in EMs: Diversification and Policy-Driven Opportunities

As China's growth model evolves, investors are recalibrating their EM allocations. The bifurcation between China and EM ex-China markets has deepened, with the latter outperforming on fundamentals and valuations, per MSCI research. Active strategies now prioritize regional diversification, favoring markets like India, Vietnam, and Mexico, which benefit from supply chain reshaping and domestic demand resilience, as highlighted in a Goldman Sachs note.

Sectoral Resilience in EM ex-China Markets

Defensive sectors in non-China EMs are gaining traction. India's IT and infrastructure sectors, for instance, have attracted capital due to favorable demographics and structural reforms, according to the Duke Fuqua outlook. In the Middle East, financial services and telecommunications are expanding under government-led economic transformations, per an OECD report. Meanwhile, Latin America's agricultural and energy sectors are seeing renewed interest as global demand for commodities stabilizes, according to a McKinsey update.

Policy-Driven Sectors in China

Within China, defensive bets are shifting toward government-backed industries. Renewable energy and biotechnology are prime examples, with state support ensuring growth despite weak domestic demand (see prior Atlas Institute analysis). The solar energy sector, in particular, has seen a 15% year-on-year increase in investment, driven by carbon neutrality goals (see prior AMRO report).

Geopolitical Risks and the Case for Active Management

Geopolitical tensions, particularly U.S.-China trade disputes, have amplified volatility. Rising tariffs and supply chain realignments are pushing companies to "friend-shore" production, with Mexico, Vietnam, and India emerging as key beneficiaries, according to Deloitte insights. However, this shift is uneven: while Mexico's semiconductor industry thrives, its agricultural exports face U.S. import barriers, as outlined in a Brookings analysis.

Active management is now critical. Investors are separating China from broader EM allocations to capture alpha in markets with stronger fundamentals. For example, Newton's strategy notes that the MSCIMSCI-- Emerging Markets ex-China Index has outperformed its China-inclusive counterpart by 3.2% year-to-date, reflecting divergent growth trajectories.

Conclusion: Balancing Caution and Opportunity

China's economic transition is neither a collapse nor a boom-it is a recalibration. For investors, the path forward lies in balancing defensive strategies with selective exposure to policy-driven sectors. While China's structural challenges persist, EM ex-China markets offer compelling opportunities in resilient sectors and diversified geographies. As the OECD notes, "Policy harmonization and sound investment frameworks will be critical to unlocking EM potential in a post-China slowdown world."

In this new normal, the winners will be those who adapt-leveraging regional diversification, sectoral specialization, and active management to navigate the ripple effects of China's evolving economy.

Comentarios

Aún no hay comentarios