Navigating Home Insurance After a Major Natural Disaster: What You Need to Know

Generado por agente de IATheodore Quinn

miércoles, 5 de febrero de 2025, 12:38 am ET2 min de lectura

HAIL--

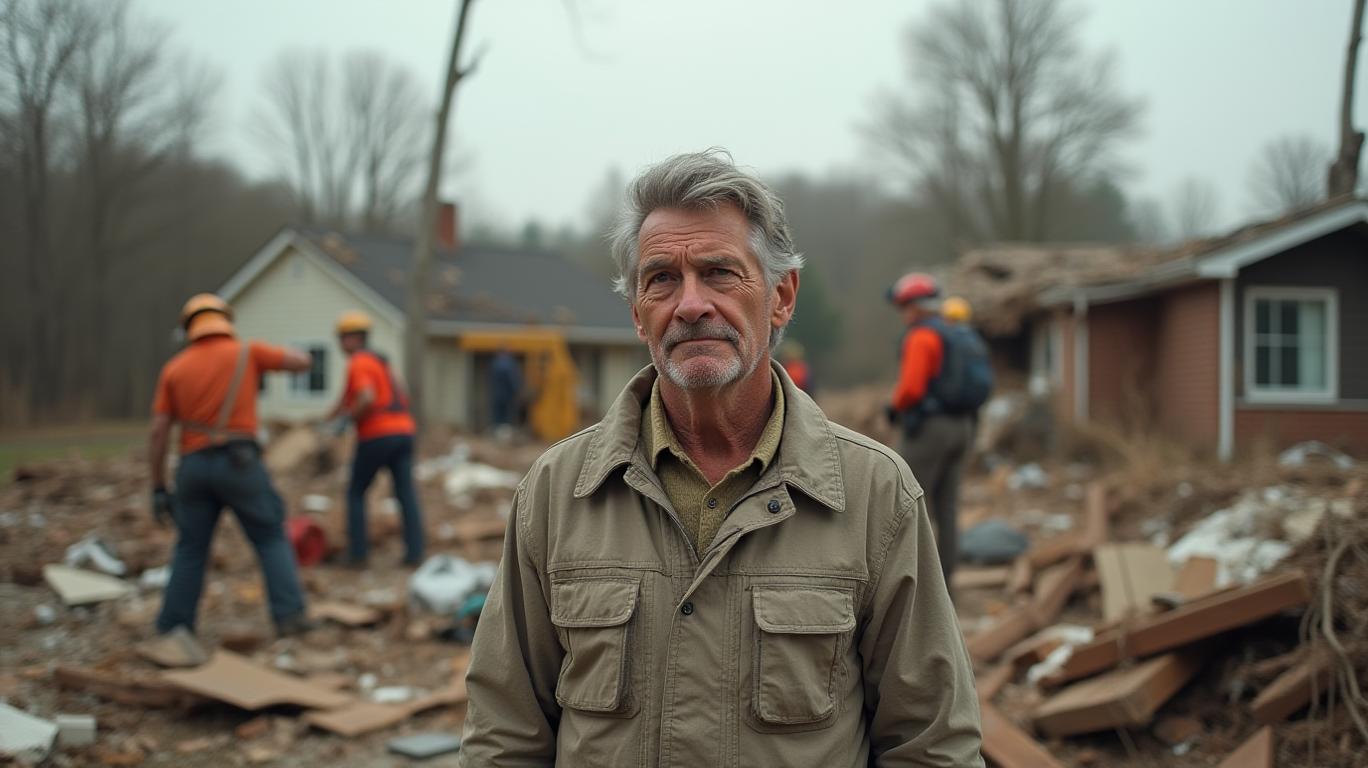

When a major natural disaster strikes, homeowners are often left with significant damage and a mountain of questions about their insurance coverage. Understanding your policy and the claims process is crucial to ensuring you receive the compensation you deserve. Here's what you need to know about home insurance coverage after a major natural disaster.

Understanding Your Policy

Before a disaster occurs, it's essential to review your home insurance policy to understand what is covered and what is not. Standard homeowners insurance policies typically cover damage caused by fires, hail, hurricanes, lightning, snow storms, wildfires, explosions, and volcanic eruptions. However, earthquakes and floods are usually excluded from standard policies.

To protect your home from these excluded events, you may need to purchase additional coverage:

* Earthquake Insurance: Earthquake insurance can be purchased as a separate policy or as an endorsement to an existing homeowners policy. This coverage helps protect your home and belongings from damage caused by earthquakes. However, it's important to note that earthquake insurance often comes with high deductibles, which can range from 5% to 15% of the policy limit.

* Flood Insurance: Flood insurance is available through the National Flood Insurance Program (NFIP), administered by FEMA, or through private insurance companies. This coverage helps protect your home and belongings from damage caused by flooding. Keep in mind that there is typically a 30-day waiting period before flood insurance coverage takes effect, so it's essential to purchase a policy well in advance of any potential flooding events.

Assessing the Damage

After a natural disaster, it's crucial to document the damage to your property. Take detailed photos and videos of all affected areas, including both exterior and interior damage. Make a list of damaged items, including descriptions, purchase dates, and estimated values. If you have receipts or proof of purchase, attach those to your list as well.

Contact your insurance company as soon as possible to initiate the claim process. Most insurers require homeowners to report damage within a specific time frame, so don't delay. Have your policy number ready and provide a clear description of the damage.

The Claims Process

Once your claim is initiated, your insurance company will likely send an adjuster to inspect your home and assess the damage. To prepare for the visit, have all your documentation—such as photos, videos, and an inventory of damaged items—ready for the adjuster to review. Be sure to accompany the adjuster during the inspection to ensure that all damage is accurately documented.

After the inspection, the adjuster will provide you with an estimate of the damage and the expected settlement amount. If you disagree with the adjuster's assessment, you have the right to request a second opinion or consult with a public adjuster.

Additional Living Expenses

If your home is uninhabitable due to the disaster, your insurance policy may cover additional living expenses, such as hotel bills and restaurant meals while you wait for your home to be repaired or rebuilt. Keep receipts for these expenses and submit them to your insurance company for reimbursement.

Filing a Home Insurance Claim After a Natural Disaster

Filing a home insurance claim after a natural disaster can be a complex and overwhelming process. However, understanding your policy and the claims process can help ensure that you receive the compensation you deserve. By following the steps outlined above and seeking the assistance of a professional public adjuster if needed, you can navigate the claims process more effectively and secure the settlement you deserve.

In conclusion, homeowners should be aware of the specific natural disasters that are typically excluded from standard home insurance policies and consider purchasing additional coverage to protect their property. After a natural disaster, it's crucial to document the damage, understand your policy, and follow the claims process to ensure you receive the compensation you deserve. By taking these steps, homeowners can better protect their property and minimize the risk of underinsurance or insufficient coverage.

WTRG--

When a major natural disaster strikes, homeowners are often left with significant damage and a mountain of questions about their insurance coverage. Understanding your policy and the claims process is crucial to ensuring you receive the compensation you deserve. Here's what you need to know about home insurance coverage after a major natural disaster.

Understanding Your Policy

Before a disaster occurs, it's essential to review your home insurance policy to understand what is covered and what is not. Standard homeowners insurance policies typically cover damage caused by fires, hail, hurricanes, lightning, snow storms, wildfires, explosions, and volcanic eruptions. However, earthquakes and floods are usually excluded from standard policies.

To protect your home from these excluded events, you may need to purchase additional coverage:

* Earthquake Insurance: Earthquake insurance can be purchased as a separate policy or as an endorsement to an existing homeowners policy. This coverage helps protect your home and belongings from damage caused by earthquakes. However, it's important to note that earthquake insurance often comes with high deductibles, which can range from 5% to 15% of the policy limit.

* Flood Insurance: Flood insurance is available through the National Flood Insurance Program (NFIP), administered by FEMA, or through private insurance companies. This coverage helps protect your home and belongings from damage caused by flooding. Keep in mind that there is typically a 30-day waiting period before flood insurance coverage takes effect, so it's essential to purchase a policy well in advance of any potential flooding events.

Assessing the Damage

After a natural disaster, it's crucial to document the damage to your property. Take detailed photos and videos of all affected areas, including both exterior and interior damage. Make a list of damaged items, including descriptions, purchase dates, and estimated values. If you have receipts or proof of purchase, attach those to your list as well.

Contact your insurance company as soon as possible to initiate the claim process. Most insurers require homeowners to report damage within a specific time frame, so don't delay. Have your policy number ready and provide a clear description of the damage.

The Claims Process

Once your claim is initiated, your insurance company will likely send an adjuster to inspect your home and assess the damage. To prepare for the visit, have all your documentation—such as photos, videos, and an inventory of damaged items—ready for the adjuster to review. Be sure to accompany the adjuster during the inspection to ensure that all damage is accurately documented.

After the inspection, the adjuster will provide you with an estimate of the damage and the expected settlement amount. If you disagree with the adjuster's assessment, you have the right to request a second opinion or consult with a public adjuster.

Additional Living Expenses

If your home is uninhabitable due to the disaster, your insurance policy may cover additional living expenses, such as hotel bills and restaurant meals while you wait for your home to be repaired or rebuilt. Keep receipts for these expenses and submit them to your insurance company for reimbursement.

Filing a Home Insurance Claim After a Natural Disaster

Filing a home insurance claim after a natural disaster can be a complex and overwhelming process. However, understanding your policy and the claims process can help ensure that you receive the compensation you deserve. By following the steps outlined above and seeking the assistance of a professional public adjuster if needed, you can navigate the claims process more effectively and secure the settlement you deserve.

In conclusion, homeowners should be aware of the specific natural disasters that are typically excluded from standard home insurance policies and consider purchasing additional coverage to protect their property. After a natural disaster, it's crucial to document the damage, understand your policy, and follow the claims process to ensure you receive the compensation you deserve. By taking these steps, homeowners can better protect their property and minimize the risk of underinsurance or insufficient coverage.

Divulgación editorial y transparencia de la IA: Ainvest News utiliza tecnología avanzada de Modelos de Lenguaje Largo (LLM) para sintetizar y analizar datos de mercado en tiempo real. Para garantizar los más altos estándares de integridad, cada artículo se somete a un riguroso proceso de verificación con participación humana.

Mientras la IA asiste en el procesamiento de datos y la redacción inicial, un miembro editorial profesional de Ainvest revisa, verifica y aprueba de forma independiente todo el contenido para garantizar su precisión y cumplimiento con los estándares editoriales de Ainvest Fintech Inc. Esta supervisión humana está diseñada para mitigar las alucinaciones de la IA y garantizar el contexto financiero.

Advertencia sobre inversiones: Este contenido se proporciona únicamente con fines informativos y no constituye asesoramiento profesional de inversión, legal o financiero. Los mercados conllevan riesgos inherentes. Se recomienda a los usuarios que realicen una investigación independiente o consulten a un asesor financiero certificado antes de tomar cualquier decisión. Ainvest Fintech Inc. se exime de toda responsabilidad por las acciones tomadas con base en esta información. ¿Encontró un error? Reportar un problema

SOBRE NOSOTROS

Nuestra historiaAutores de noticiasBase de conocimientosPolítica de privacidadTérmino de usoDescargo de responsabilidad de corretaje de tercerosTérminos de uso de AIMEDivulgaciones de riesgos de AInvest AICarrerasCONTÁCTENOS

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.

Comentarios

Aún no hay comentarios