Navigating High-Cost Housing: 15-Year Mortgages vs. Alternatives in a Post-Pandemic Market

The post-pandemic housing market has become a minefield of trade-offs for buyers. With home prices stubbornly high and mortgage rates elevated, the age-old debate between 15-year and 30-year mortgages has taken on new urgency. Let’s cut through the noise and dissect the numbers, liquidity risks, and real-world wisdom to determine whether the 15-year mortgage is still a viable path—or if alternatives like 30-year mortgages with extra payments or renting might better serve today’s financially cautious households.

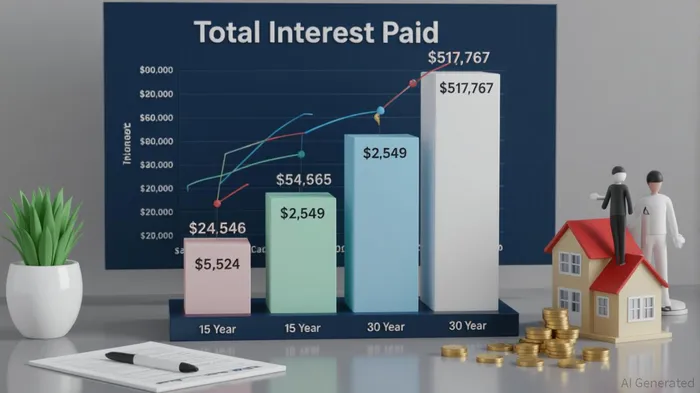

The Cost Conundrum: 15-Year vs. 30-Year Mortgages

The math is stark. For a $400,000 loan, a 15-year mortgage at 5.76% results in a monthly payment of $3,324 and total interest of $124,546 over the loan’s life. By contrast, a 30-year mortgage at 6.58% would cost $2,549 monthly but incur $517,767 in interest—a 410% increase [1]. This isn’t just a numbers game; it’s a generational wealth decision. The 15-year term locks in lower rates and builds equity faster, but the higher monthly payments can strain households already grappling with inflation-driven expenses [2].

Consider a $500,000 mortgage: the 15-year payment ($4,337) is a staggering $1,010 more than the 30-year option ($3,327). That’s a significant chunk of change that could otherwise fund emergency savings, retirement accounts, or investments [3]. Financial planners increasingly warn that the 15-year mortgage’s appeal hinges on stable, high incomes—a luxury many lack in today’s volatile economy [4].

Liquidity and Flexibility: The 30-Year Mortgage’s Hidden Edge

The 30-year mortgage’s lower payments aren’t just easier on the wallet—they’re a lifeline for liquidity. Critics argue that the 15-year term creates a “one-sided bet” where borrowers bear the risk of income shocks or emergencies, while lenders profit from fixed rates [5]. Real-world investors echo this, noting that “paying a little extra each month on a 30-year mortgage at a payment you can afford” offers a safer, more adaptable strategy [6].

Here’s the kicker: If you invest the $1,010 monthly savings from a 30-year mortgage at an 8% annual return, you’d accumulate over $1.5 million in 30 years—enough to offset the extra interest paid and then some [3]. This flexibility is invaluable in a market where home prices and rents are rising faster than incomes [7].

The Renting Dilemma: Liquid but Leaky

Renting is often dismissed as a “no-equity” option, but it’s not without merit. Monthly costs are typically lower than mortgage payments, and renters avoid property taxes, insurance, and maintenance expenses. However, in high-cost markets like San Francisco or New York, long-term rent hikes can erode savings. A 2025 study found that in markets with 5% annual rent growth, renters could end up paying more than homeowners in 15 years [8].

Expert Critiques and the “Lock-In Effect”

Financial experts have sounded alarms about the 30-year mortgage’s structural flaws. The “lock-in effect” keeps homeowners with low-rate mortgages from selling, reducing inventory and inflating prices [2]. Meanwhile, the 15-year mortgage’s popularity remains low due to its liquidity demands. As one analyst put it, “The 15-year mortgage is a great deal for those who can afford it—but it’s not for everyone” [4].

The Verdict: A Nuanced Approach

The 15-year mortgage is a winner for those with stable, high incomes and a long-term commitment to a home. But for most, the 30-year mortgage with extra principal payments strikes a better balance. By allocating $500–$1,000 monthly toward principal, borrowers can shorten their loan term and reduce interest costs without sacrificing liquidity [3]. Renters, meanwhile, should focus on investing the difference—provided they’re in markets where home appreciation outpaces rent growth.

Source:

[1] Current 15-year mortgage rates compared to other loan types [https://www.bankrate.com/mortgages/15-year-mortgage-rates/]

[2] Data Spotlight: The Impact of Changing Mortgage Interest Rates [https://www.consumerfinance.gov/data-research/research-reports/data-spotlight-the-impact-of-changing-mortgage-interest-rates/]

[3] Should You Choose a 15 or 30 Year Mortgage in 2025? [https://www.millswealthadvisors.com/should-you-choose-a-15-or-30-year-mortgage-in-2025/]

[4] A 30-Year Trap: The Problem With America's Weird [https://www.nytimes.com/2023/11/19/business/economy/30-year-mortgage.html]

[5] 15-Year vs. 30-Year Mortgage: What's the Difference? [https://www.investopedia.com/articles/personal-finance/042015/comparison-30year-vs-15year-mortgage.asp]

[6], [15yr vs 30yr mortgage rate] [https://www.redditRDDT--.com/r/BayAreaRealEstate/comments/1j467uw/15yr_vs_30yr_mortgage_rate/]

[7] Impact of Today's Changing Interest Rates on the Housing Market [https://www.usbank.com/investing/financial-perspectives/investing-insights/interest-rates-impact-on-housing-market.html]

[8] Data Spotlight: The Impact of Changing Mortgage Interest Rates [https://www.consumerfinance.gov/data-research/research-reports/data-spotlight-the-impact-of-changing-mortgage-interest-rates/]

Comentarios

Aún no hay comentarios