Navigating Fixed-Income Income Generation in a Low-Yield Environment: The Case for High-Quality ETFs

In the current fixed-income landscape, investors face a paradox: historically low yields coexist with a resilient economy and a Federal Reserve poised to ease policy further. This environment demands a nuanced approach to income generation, one that prioritizes quality, duration management, and sector-specific opportunities. High-quality ETFs like the SPDR Portfolio Intermediate Term Treasury ETF (SPTI) have emerged as compelling tools for navigating these challenges, offering a blend of stability, liquidity, and competitive returns.

The Fed's Tightrope and Its Impact on Yields

The Federal Reserve's 25-basis-point rate cut in September 2025, bringing the fed funds rate to 4.0%–4.25%, underscores its balancing act between inflation control and economic risk management, according to Treasury rates. While short-term rates have declined, long-term yields have remained stubbornly elevated. The 10-year Treasury yield now stands at 4.20%, and the 30-year yield at 4.77%, reflecting market expectations of sustained inflation and a steepening yield curve (Treasury rates). This divergence-short-term easing versus long-term resilience-has created a complex backdrop for bond investors.

High-Quality ETFs Outperform in a Fragmented Market

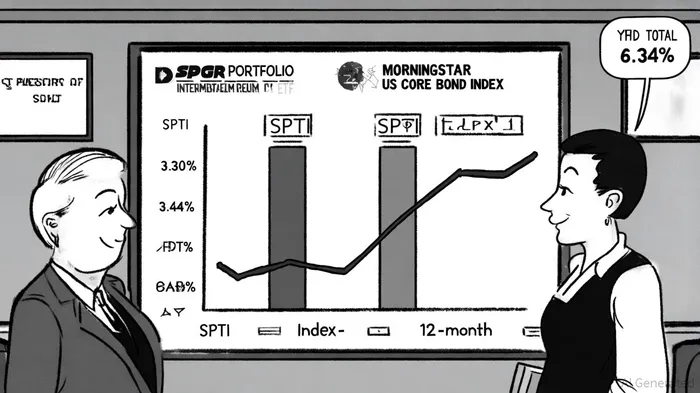

Amid this volatility, high-quality fixed-income ETFs have outperformed broader benchmarks. For instance, the SPDR Portfolio High Yield Bond ETF (SPHY) has delivered an 11.37% return over the past 12 months, far outpacing the Morningstar US Core Bond Index's 3.44%, as shown on a Morningstar list. Similarly, the SPDR Portfolio Intermediate Term Treasury ETF (SPTI) has returned 3.30% over the same period, with a stronger YTD total return of 6.34% (FinanceCharts). These results highlight the advantages of focusing on high-credit-quality instruments and intermediate-duration strategies, which mitigate interest rate risk while capturing yield.

The outperformance is not accidental. Investment-grade corporates and municipal bonds have benefited from tight credit spreads and strong demand, with the 10-year investment-grade spread tightening to 72 basis points, according to the Nuveen commentary. High-yield corporates and preferred securities have also seen gains, driven by a flight to relative safety amid geopolitical uncertainties (Nuveen commentary). In contrast, Treasury bonds and emerging market debt have lagged, underscoring the importance of sector selection.

Duration Management: The Key to Balancing Risk and Return

SPTI's focus on intermediate-term Treasuries (1–10 years) positions it to benefit from both income generation and moderate price stability. While the fund faced a -10.64% decline in 2022, its 10-year total return of 15.39% demonstrates its resilience over full cycles (FinanceCharts). This aligns with a broader trend: investors are increasingly favoring intermediate-duration bonds to hedge against the volatility of long-term Treasuries, which have struggled in a rising rate environment.

The steepening yield curve-2-year yields at 3.63% versus 10-year yields at 4.20%-further supports this strategy. A 57-basis-point spread between these maturities offers a buffer against rate hikes while preserving capital (Treasury rates). For income-focused investors, this dynamic makes intermediate-term ETFs like SPTISPTI-- a more attractive option than long-dated bonds, which face greater price sensitivity to rate changes.

Looking Ahead: Policy, Inflation, and Strategic Allocation

The Fed's forward guidance suggests two additional 25-basis-point cuts in 2025, which could further support bond prices and narrow credit spreads (Nuveen commentary). However, investors must remain cautious. While inflation expectations have moderated, they remain above pre-pandemic levels, with 35 basis points of the 10-year yield increase since mid-2024 attributed to inflation concerns, according to a Morningstar analysis. This means that even in a low-yield environment, real returns remain under pressure.

For investors seeking to optimize income generation, the solution lies in a diversified approach. High-quality ETFs like SPTI offer a foundation of stability, while allocations to high-yield corporates and preferred securities can enhance returns without excessive risk (Morningstar list). Meanwhile, avoiding overexposure to Treasuries and emerging markets-sectors that have underperformed in 2025-can help preserve capital.

Conclusion

The low-yield environment of 2025 is not a dead end for income generation-it is a call to refine strategies. High-quality fixed-income ETFs, particularly those with intermediate durations and strong credit profiles, offer a path forward. By leveraging these tools, investors can navigate the Fed's tightening cycle, capitalize on sector-specific opportunities, and build portfolios that balance yield with resilience.

Comentarios

Aún no hay comentarios