Navigating the Divergent Real Estate Landscape: Tactical Opportunities in a Correcting Market

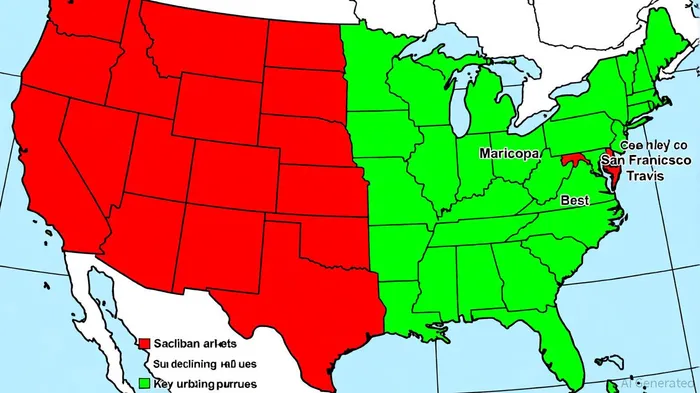

The U.S. housing market in 2025 is marked by stark regional divergence, with urban coastal hubs experiencing value declines while Sun Belt regions defy the trend. According to the Zillow Home Value Index for Q3 2025, national home values have fallen by approximately -1.9% year-over-year, driven by affordability challenges and elevated mortgage costs [1]. This correction is most pronounced in high-cost urban markets, where counties like San Francisco (-2.8%), King County (Washington), and Cook County (Illinois) face sharper declines [1]. Conversely, Sun Belt regions—particularly in Texas, Florida, Arizona, and North Carolina—continue to outperform, with Maricopa County (Arizona) and Travis County (Texas) posting gains of +3.9% and +3.4%, respectively [1]. This bifurcation underscores a structural shift in housing demand, driven by remote work flexibility, demographic trends, and supply constraints.

REITs: A Hedge Against Housing Market Volatility

While the housing market grapples with correction risks, real estate investment trusts (REITs) present a compelling tactical opportunity. Despite a prolonged underperformance relative to the S&P 500—returning just 2.6% annualized over five years as of early 2025—REITs are now poised for a rebound [2]. J.P. Morgan Research projects REIT earnings growth to remain stable at 3% in 2025, with fundamentals strengthening as capital markets liquidity improves [3]. By 2026, growth could accelerate to nearly 6%, supported by rate cuts and a return of pricing power in key sectors [3].

Sector-Specific Tactical Insights

- Office REITs: Vacancy rates are expected to peak by early 2026, with leasing activity rebounding as hybrid work norms stabilize [3]. Investors should prioritize markets with strong corporate demand, such as Austin and Raleigh, where Sun Belt job growth offsets urban declines.

- Residential REITs: Pricing power is anticipated to return in late 2025, particularly in Sun Belt markets where in-migration and limited supply drive demand [3]. However, caution is warranted in coastal markets, where affordability strains could dampen rental growth.

- Industrial REITs: While property-level cash flows remain resilient, sector headwinds from tariffs and economic slowdowns necessitate a cautious approach [3].

- Retail REITs: Strong consumer spending and limited supply in strip centers offer upside, but exposure to discretionary retailers remains a risk [3].

Strategic Positioning for 2025

The Federal Reserve's anticipated rate cuts and improving borrowing costs create a favorable environment for REITs, particularly those with access to capital for value-add acquisitions [2]. Small-cap and mid-cap REITs, which surged by +7.52% and +7.13% in August 2025, exemplify the sector's potential [4]. Investors should focus on REITs with exposure to Sun Belt growth corridors and diversified tenant bases to mitigate regional correction risks.

Zillow's dominance in the housing data ecosystem—boasting 227 million monthly users—further underscores the importance of data-driven decision-making in real estate [4]. As home values adjust, REITs with agile capital structures and sector-specific expertise will be best positioned to capitalize on dislocation.

Conclusion

The 2025 housing market correction is not uniform; it is a mosaic of regional resilience and vulnerability. While urban coastal markets face near-term headwinds, Sun Belt dynamics and REIT sector innovation offer a counterbalance. For tactical investors, the key lies in aligning exposure with structural trends—leveraging REITs to hedge against volatility while capturing growth in high-conviction markets.

Comentarios

Aún no hay comentarios