Navigating Democratic Fiscal Uncertainty: Strategic Asset Allocation in a Polarized Era

Political instability in U.S. fiscal policy, particularly under Democratic-led frameworks, has emerged as a critical driver of asset allocation strategies. The Democratic Party's emphasis on expansive fiscal measures—such as infrastructure spending, progressive taxation, and social welfare programs—has been accompanied by growing concerns over long-term debt sustainability. According to the U.S. Government Accountability Office (GAO), federal debt is projected to more than double as a share of GDP over the next 30 years under current fiscal policies, raising alarms about economic resilience and investor confidence [1]. This trajectory, coupled with partisan gridlock, has created a volatile environment where market participants must navigate conflicting signals between short-term stimulus and long-term fiscal caution.

Fiscal Uncertainty and Market Mechanisms

Democratic fiscal policy uncertainty (FPU) manifests through delayed legislative action, abrupt shifts in spending priorities, and prolonged debates over deficit reduction. Research underscores that such uncertainty dampens industrial production and investment, with effects persisting for months [5]. For instance, government shutdowns and fiscal brinkmanship—common during Democratic-Republican negotiations—have historically tightened credit conditions and eroded consumer confidence. The Federal Reserve has noted that these events disproportionately impact sectors reliant on government contracts, such as aerospace and defense, which face operational disruptions and cash flow constraints [1].

Moreover, FPU amplifies borrowing costs for the U.S. government, indirectly raising market volatility. A study by the IMF highlights that fiscal uncertainty correlates with synchronized global financial movements, including risk aversion and dollar strength, as investors seek safe-haven assets [3]. This dynamic has forced institutional investors to recalibrate portfolios, favoring shorter-duration bonds and defensive equities to mitigate liquidity risks.

Investor Adaptation: Historical Patterns and Modern Strategies

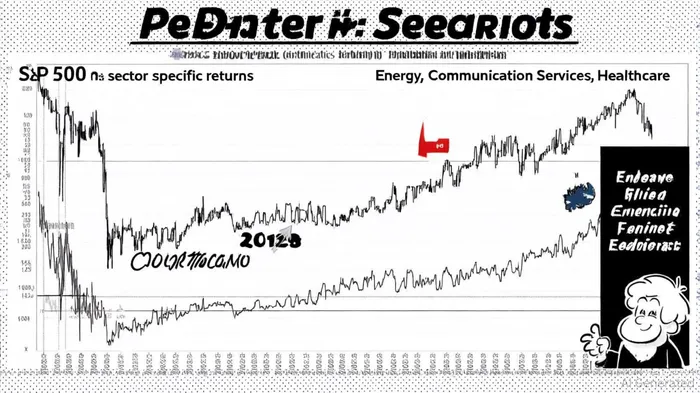

Historical data reveals distinct sectoral responses to Democratic fiscal cycles. During Democratic administrations, Energy and Communication Services sectors have historically outperformed the S&P 500, while Healthcare has lagged [2]. This divergence reflects policy-driven tailwinds for infrastructure and tech innovation, contrasted with regulatory headwinds in healthcare. For example, J.P. Morgan's 3Q 2025 asset allocation report recommends overweights in U.S. tech and communication services, citing their resilience amid trade tensions and fiscal uncertainty [5].

Modern investors are adopting nuanced strategies to hedge against Democratic fiscal risks. CFRA advocates a 60% equities, 35% bonds, and 5% cash allocation to balance growth and stability [1]. Meanwhile, J.P. Morgan emphasizes strategic overweights in bonds, particularly international duration (e.g., Italian BTPs and UK Gilts), to diversify against U.S. fiscal volatility [5]. These approaches reflect a shift toward “fiscal dominance” themes, where investors bet on long-term U.S. economic resilience despite short-term turbulence.

Sector-Specific Impacts and Policy Contingencies

Beyond macroeconomic trends, sector-specific vulnerabilities are emerging. The Congressional Budget Office (CBO) has outlined deficit-reduction scenarios, including spending cuts and tax reforms, which could reshape corporate earnings trajectories [4]. For instance, energy firms face regulatory uncertainty under potential climate policies, while financial institutions may benefit from increased public investment. Additionally, firms are adopting conservative financial policies during high FPU periods, including reduced capital expenditures and cautious payout ratios [6].

Investors must also consider the implications of fiscal policy on accounting practices. Grant Thornton advises companies to proactively disclose risks from policy shifts—such as tariff impositions or spending freezes—to align investor expectations [4]. This transparency is critical in an era where policy-driven earnings volatility is becoming the norm.

Conclusion: Balancing Risk and Resilience

The Democratic Party's fiscal vulnerabilities present both challenges and opportunities for investors. While rising debt and political polarization heighten uncertainty, strategic asset allocation can capitalize on sectoral asymmetries and long-term economic themes. As the GAO warns of an unsustainable fiscal path, investors must remain agile, leveraging tools like TIPS, international bonds, and sector rotation to navigate a landscape where fiscal policy and market stability are inextricably linked.

Comentarios

Aún no hay comentarios