Navigating Czech Labor Market Crosscurrents: Opportunities and Risks for Equity and Bond Investors

The Czech Republic's labor market is a study in contrasts: persistent unemployment in industrial regions clashes with acute labor shortages in construction and logistics, while inflation nears 2.4% and real wage growth stalls. For investors, these dynamics present both pitfalls and opportunities. Sectoral imbalances and regional disparities could reshape equity and bond markets, while inflation risks demand careful navigation.

Sectoral Imbalances: A Tale of Two Economies

The Czech labor market is bifurcated between declining industries and booming sectors. Industrial regions like Ústí nad Labem (6.6% unemployment) and Moravian-Silesian (6%) face stagnation in manufacturing and energy sectors, while employers in construction, logistics, and healthcare scramble to fill vacancies. Over 264,000 job openings exist nationwide, particularly for roles like construction trades workers, forklift operators, and healthcare staff.

The mismatch stems from structural shifts. Automation and global supply chain adjustments have reduced demand for low-skilled manufacturing jobs, while digitalization and green energy projects drive demand for technical skills. Yet vocational training systems, as noted by the OECD, often over-specialize in outdated trades, leaving workers unprepared for emerging roles. This creates a skills gap that could benefit companies investing in reskilling or tech-driven efficiency.

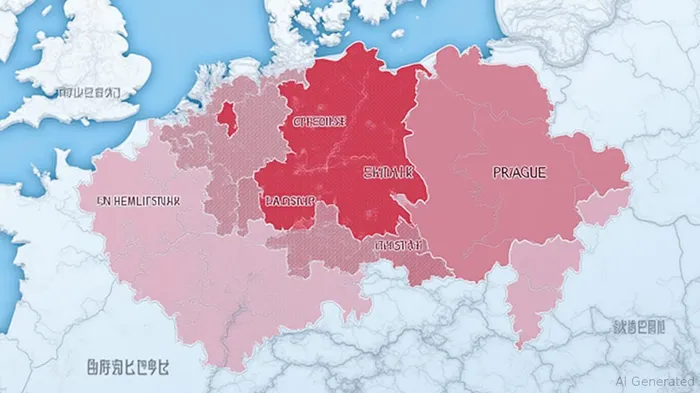

Regional Disparities: A Map of Contrasts

Regional unemployment rates highlight stark divides. Prague's 3.1% unemployment is half that of Most (9.4%) and Karviná (8.9%). These disparities reflect economic specialization:

- Northern and eastern regions: Heavily reliant on coal, steel, and traditional manufacturing, they face declining industries and lack job-creating innovation hubs.

- Central and western regions: Prague and its suburbs dominate services, tech, and finance, attracting talent and investment.

This geographic divide offers strategic opportunities. Investors might consider regional infrastructure projects or real estate in underserved areas, where low labor costs could attract businesses. However, political pressure to address inequality may lead to fiscal stimulus, boosting public-sector bonds temporarily.

Inflation Risks: A Fragile Equilibrium

The Czech National Bank (CNB) projects inflation to remain near 2.4% in 2025, just above its 2% target. While headline inflation is moderate, core inflation (excluding energy and food) has edged higher, reaching 2.7% in May 2025. This reflects persistent service-sector price pressures—e.g., healthcare, education, and public services—driven by labor shortages and regulatory fees.

Meanwhile, real wage growth has slowed to 0.8% year-on-year in 2025, insufficient to keep pace with even this muted inflation. This weakens consumer purchasing power, particularly in regions with high unemployment. The CNB's 3.75% key rate, aimed at curbing inflation, adds to the pressure, as borrowing costs remain elevated for households and businesses.

Investment Implications: Equity Opportunities, Bond Caution

Equities:

- Consumer Discretionary: If wage growth rebounds, sectors like retail, autos, and travel could thrive. Monitor companies with pricing power or exposure to resilient spending, such as Czech retail giants like Albert or Billa.

- Construction & Logistics: Firms addressing labor shortages via automation or workforce training (e.g., logistics companies using AI for route optimization) could outperform.

- Healthcare: Chronic staff shortages in healthcare create opportunities for private providers or telemedicine platforms.

Bonds:

- Government Bonds: Persistent core inflation risks could force the CNB to delay rate cuts, pressuring bond yields. The 10-year Czech bond yield (currently ~3.8%) may rise further if inflation stays elevated.

- Corporate Bonds: Companies in labor-starved sectors may face rising wage costs, squeezing margins. Avoid overleveraged firms without pricing power.

Conclusion: A Delicate Balancing Act

The Czech Republic's labor market is a microcosm of global economic challenges: aging industries, skills mismatches, and inflationary pressures. Equity investors can capitalize on sectoral winners—construction tech, healthcare, and reskilling initiatives—while bond investors should brace for volatility tied to inflation outcomes.

For now, the CNB's tight monetary policy keeps inflation in check, but the 2.4% rate is a precarious equilibrium. Equity portfolios should favor sectors with pricing power or labor solutions, while bonds require a defensive stance unless inflation trends downward.

In this environment, investors must remain nimble, ready to pivot as wage growth, regional policies, or global commodity prices shift the balance between opportunity and risk.

Comentarios

Aún no hay comentarios