Navigating Asia-Pacific Tariff Turbulence: Where to Invest Amid U.S. Trade Pressures

The Trump administration's aggressive tariff strategy in 2025 has turned Asia-Pacific markets into a high-stakes arena of geopolitical and economic maneuvering. While sectors like automotive and pharmaceuticals face punitive tariffs and shrinking profit margins, others—such as tech leaders in Singapore and Taiwan—are emerging as bastions of resilience. This article dissects the shifting landscape, identifying opportunities in supply chain diversification and cautioning against overexposure to vulnerable industries.

Automotive Sector: A Bull's-Eye for Tariffs—Avoid Overexposure

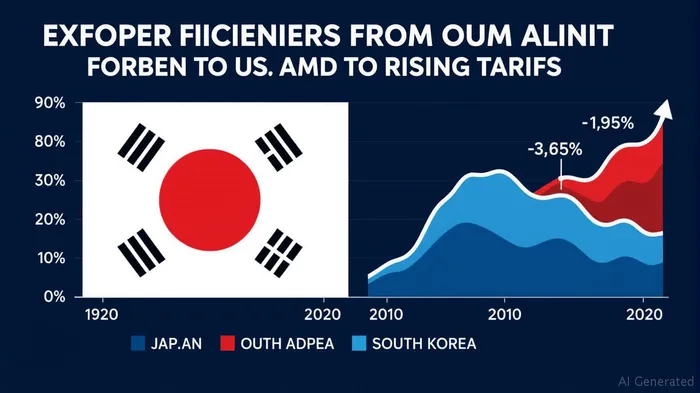

The automotive industry is ground zero for U.S. tariff pressures. Japan and South Korea, which exported a combined 2.9 million vehicles to the U.S. in 2024, now face tariffs of 25-40% by August 1, 2025.  . Companies like Nissan, ToyotaTM--, and Hyundai may struggle to absorb costs without passing them onto consumers—a risky move in a slowing global economy.

. Companies like Nissan, ToyotaTM--, and Hyundai may struggle to absorb costs without passing them onto consumers—a risky move in a slowing global economy.

.

Investors should tread carefully here. While some firms may pivot to reshoring or renegotiate trade terms, the sector's reliance on export-driven revenue makes it a high-risk bet.

Tech and Semiconductors: A Safe Haven for Growth

The semiconductor and technology sectors, particularly in Singapore and Taiwan, are positioned to thrive. The U.S. partnership with Japan and the EU to decouple from Chinese influence has spurred demand for non-Chinese suppliers. Companies like Taiwan Semiconductor Manufacturing (TSMC) and Singapore's STMicroelectronicsSTM-- are critical to this shift, benefiting from U.S. incentives for domestic production and regional supply chain diversification.

.

Taiwan's strategic neutrality and Singapore's status as a global trade hub make them ideal bases for tech firms. Meanwhile, Vietnam's role as a transshipment hub for Chinese goods—now subject to 40% tariffs—could incentivize companies to establish direct manufacturing ties with non-Chinese partners, further boosting regional tech ecosystems.

Pharmaceuticals: A Cautionary Tale of High Tariffs

The pharmaceutical sector faces a grim outlook. With a $139 billion U.S. trade deficit in 2024 and potential 200% tariffs looming, firms in Japan and South Korea (e.g., Takeda and Samsung Biologics) are vulnerable. These punitive rates could force companies to shift production closer to U.S. markets or accept razor-thin margins.

.

Investors should avoid overexposure here unless companies demonstrate rapid supply chain reconfiguration or diversification into untaxed markets.

Agriculture: A Bargaining Chip with Limited Upside

Japan's concessions on agricultural market access under the CPTPP framework offer a glimpse into how trade negotiations are being weaponized. While sectors like beef or dairy may see short-term gains, their reliance on bilateral deals with the U.S. exposes them to political whims.

.

This sector's narrow focus and vulnerability to renegotiation make it a speculative play at best.

Geopolitical Hedging: Diversify, Monitor Deadlines, and Stay Nimble

The August 1 deadline is a pivotal moment. While Trump's “firm but not 100% firm” stance suggests potential delays, investors should assume compliance. Key strategies include:

- Sector Rotation: Shift capital from tariff-hit industries (autos, pharma) to tech and supply chain diversification plays.

- Regional Focus: Prioritize Singapore, Taiwan, and Malaysia over Japan/South Korea for manufacturing exposure.

- Monitor Deadlines: Track negotiations closely—U.S. concessions on digital services taxes or sector exemptions could unlock value.

Final Analysis: Capitalize on Volatility with a Selective Lens

The Asia-Pacific market is a mosaic of risks and rewards. While automotive and pharmaceutical stocks face headwinds, tech leaders and supply chain innovators offer growth avenues. Geopolitical hedging requires avoiding overexposure to U.S.-exposed economies and embracing regions with strategic autonomy.

.

Investors should use dips to accumulate stakes in resilient tech firms while hedging against auto-sector declines. The path forward is volatile, but disciplined diversification will be the key to turning geopolitical turbulence into profit.

Stay informed, stay selective, and keep an eye on those August deadlines.

Comentarios

Aún no hay comentarios