Navigating the 2025 Fed Rate-Cut Cycle: Tactical Asset Allocation Strategies for Fixed Income and Equities

The Federal Reserve's September 2025 rate cut—marking the first reduction in a nine-month pause—has reignited debates about the trajectory of monetary policy and its implications for asset allocation. With the federal funds rate now at 4.00%-4.25%, the central bank has signaled two additional 25-basis-point cuts by year-end, followed by a slower easing pace in 2026 and 2027[1]. This shift, driven by a weakening labor market and persistent inflation above 2%, has prompted investors to recalibrate their portfolios.

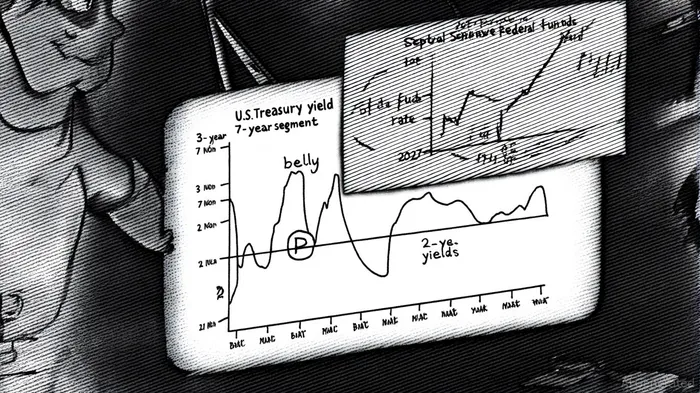

Fixed Income: Targeting the "Belly" of the Yield Curve

As the Fed embarks on its easing cycle, fixed-income strategies are pivoting toward the "belly" of the U.S. Treasury yield curve—the 3- to 7-year segment—where a steeper slope offers a balanced mix of income and duration risk[1]. This approach reflects the expectation that long-term rates may not decline in lockstep with policy cuts, particularly in the absence of a recession. According to a report by InvescoIVZ--, this segment provides a sweet spot for investors seeking to capitalize on higher yields without overexposing themselves to long-duration volatility[1].

Meanwhile, cash-heavy allocations are losing favor. With the Fed's rate cuts projected to reduce cash yields, investors are advised to extend duration modestly and explore high-yield bonds, which offer compelling returns relative to Treasuries[2]. BlackRockBLK-- highlights that credit spreads have tightened, making high-yield bonds an attractive option for income generation, while active income-oriented ETFs and market-neutral funds can further diversify risk[2].

However, caution remains warranted. The Fed's dissenting vote by Stephen Miran—a Trump appointee—advocating for a 50-basis-point cut underscores internal policy divergences[4]. This uncertainty reinforces the case for shorter-duration instruments, as rapid policy shifts could disrupt long-end yields.

Equities: Defensive Positioning Amid Policy Uncertainty

Equity strategies are also adapting to the evolving rate environment. The September rate cut, coupled with softening labor market data—including a weaker-than-expected non-farm payroll report—has prompted asset managers to adopt a more defensive stance[2]. Firms like Pathstone have reduced tactical exposures in growth allocations, reflecting concerns over valuation pressures on large-cap U.S. equities and the potential inflationary impact of U.S. trade policies[3].

The focus has shifted toward regional equity markets with neutral exposures, as investors hedge against currency volatility and global growth risks[1]. This aligns with broader macroeconomic trends, including the Fed's revised projections for a 4.5% unemployment rate in 2025 and a gradual decline in core PCE inflation to 2.6% by 2026[4].

Importantly, the Fed's signaling of further cuts has priced in a high probability of easing, reducing the likelihood of abrupt market corrections. As noted by BlackRock, this environment favors a "barbell" approach: underweighting the U.S. dollar while maintaining selective exposure to sectors insulated from rate volatility[2].

Looking Ahead: Balancing Opportunity and Risk

The Fed's 2025 rate-cut path presents both opportunities and challenges. For fixed income, the belly of the yield curve and high-yield bonds offer a compelling risk-reward profile, while equities require a nuanced approach to navigate policy-driven uncertainties. As the central bank navigates the delicate balance between inflation control and economic growth, tactical reallocation will remain critical.

Comentarios

Aún no hay comentarios