Navient's Q3 2025 Net Charge-Offs: A Sign of Resilience or a Warning Signal?

Credit Risk in Context: Navient's Historical Benchmarks

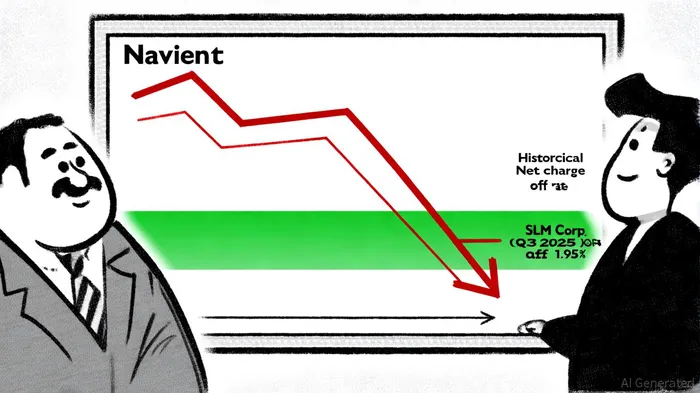

Navient's net charge-off rate-a critical metric for assessing credit risk-has historically ranged between 1.5% and 2%, according to the earnings call transcript. This range, while modest, reflects the company's exposure to student loan portfolios, which are inherently less cyclical than other credit products. However, the Q3 2025 earnings call transcript suggests that the company's charge-off rate for the quarter may remain within this historical band, even as revenue plummets. By comparison, SLM Corp (SLM) reported a net charge-off rate of 1.95% for private education loans in Q3 2025, as shown in SLM Q3 highlights. This near-alignment with industry benchmarks suggests that Navient's credit risk profile has not deteriorated sharply, at least on the surface.

Yet, this apparent stability masks deeper vulnerabilities. Navient's revenue decline-driven by divestitures of non-core businesses like Government Services and Healthcare Services, as outlined in Navient's earnings deck-reflects a strategic retreat rather than a sign of operational health. While these moves aim to reduce costs, they also signal a shrinking asset base, which could amplify sensitivity to future defaults.

Portfolio Sustainability: A Delicate Balance

Navient's Q3 2025 results underscore a paradox: improved earnings per share (EPS) of $0.29, surpassing analyst expectations of $0.18, per a GuruFocus report, contrasted with a 31.4% year-on-year revenue drop in the prior quarter (the IndexBox preview cited above). This discrepancy highlights the company's reliance on cost-cutting measures, such as outsourcing servicing operations and reducing operating expenses (described in the NavientNAVI-- earnings deck), to prop up profitability. While these steps may stabilize short-term results, they raise concerns about long-term portfolio sustainability.

For instance, Navient's servicing revenues-a key revenue stream-are projected to decline by 29.1% sequentially (per the Navient earnings deck), indicating reduced borrower activity or loan balances under management. This trend could exacerbate credit risk if borrowers face renewed financial stress, particularly as interest rates remain elevated and repayment terms tighten. Furthermore, the company's net interest income (NII) in the consumer lending segment is expected to fall by 4.6% (also noted in the Navient earnings deck), signaling weaker demand for new loans-a critical source of future earnings.

Industry-Wide Pressures and Strategic Implications

The student loan sector is not immune to macroeconomic shifts. SLM Corp's 1.95% charge-off rate (covered in the SLM Q3 highlights) reflects broader challenges, including rising defaults among borrowers grappling with stagnant wages and inflation. Navient's historical resilience-its charge-off rate remaining within 1.5%–2%-suggests disciplined underwriting and portfolio management. However, the company's repeated misses of revenue estimates (five times in two years, per the IndexBox preview) indicate structural weaknesses that could amplify credit risk in a downturn.

Investors must also consider regulatory and policy risks. The Biden administration's student debt relief programs and shifting repayment terms could alter default dynamics, potentially increasing charge-offs for servicers like Navient. While the company's cost-restructuring efforts aim to mitigate these risks, they do not address underlying vulnerabilities in its asset base.

Conclusion: A Tenuous Equilibrium

Navient's Q3 2025 net charge-off rate, if it remains within historical norms, may appear to signal resilience. However, this metric must be contextualized against the company's collapsing revenue and shrinking portfolio. The contrast with SLM Corp's 1.95% benchmark (noted in the SLM Q3 highlights) reveals that Navient is not outperforming peers on credit risk but merely keeping pace-a precarious position in a sector marked by volatility.

For Navient to achieve sustainable growth, it must demonstrate that its cost-cutting strategies can coexist with a robust, diversified portfolio. Until then, the net charge-off rate-while stable-remains a warning signal rather than a badge of resilience. Investors would be wise to monitor not just the rate itself, but the structural forces shaping Navient's ability to weather the next economic cycle.

Comentarios

Aún no hay comentarios